Turning Probability into an Asset: A Forward-Looking Perspective on Prediction Market Agents

TechFlow Selected TechFlow Selected

Turning Probability into an Asset: A Forward-Looking Perspective on Prediction Market Agents

Prediction market agents will take early shape by early 2026 and are expected to emerge as a new product category in the agent space over the coming year.

Author: 0xjacobzhao

In our prior Crypto AI research reports, we have consistently emphasized that the most practically valuable applications in crypto today lie primarily in stablecoin payments and DeFi. Meanwhile, Agents represent the critical user-facing interface of the AI industry. Therefore, within the convergence trend of crypto and AI, the two most valuable pathways are: (1) AgentFi in the short term—built atop mature, existing DeFi protocols (e.g., lending, liquidity mining for basic strategies; swaps, Pendle PT, funding rate arbitrage for advanced strategies); and (2) Agent Payment in the medium to long term—centered on stablecoin settlement and leveraging protocols such as ACP/AP2/x402/ERC-8004.

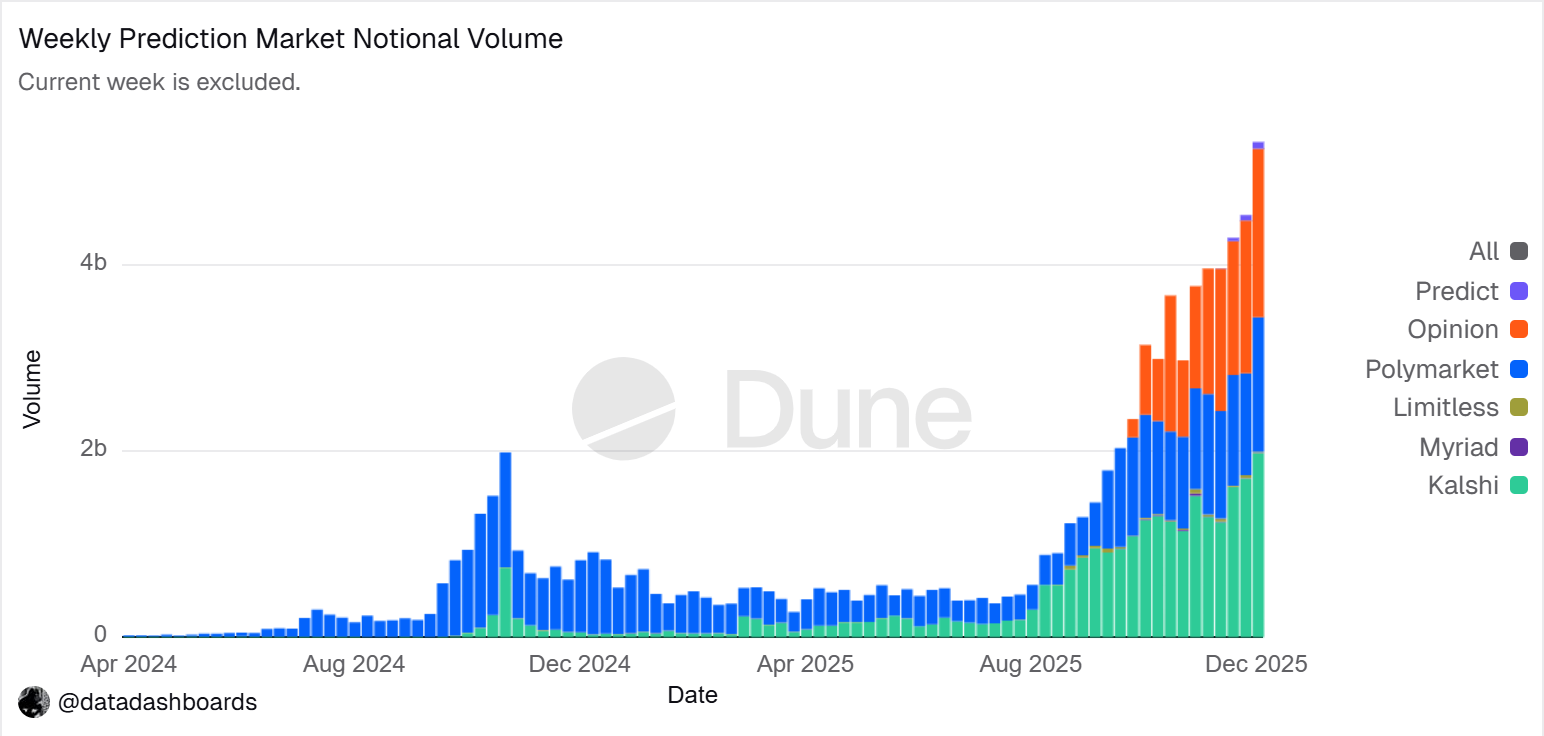

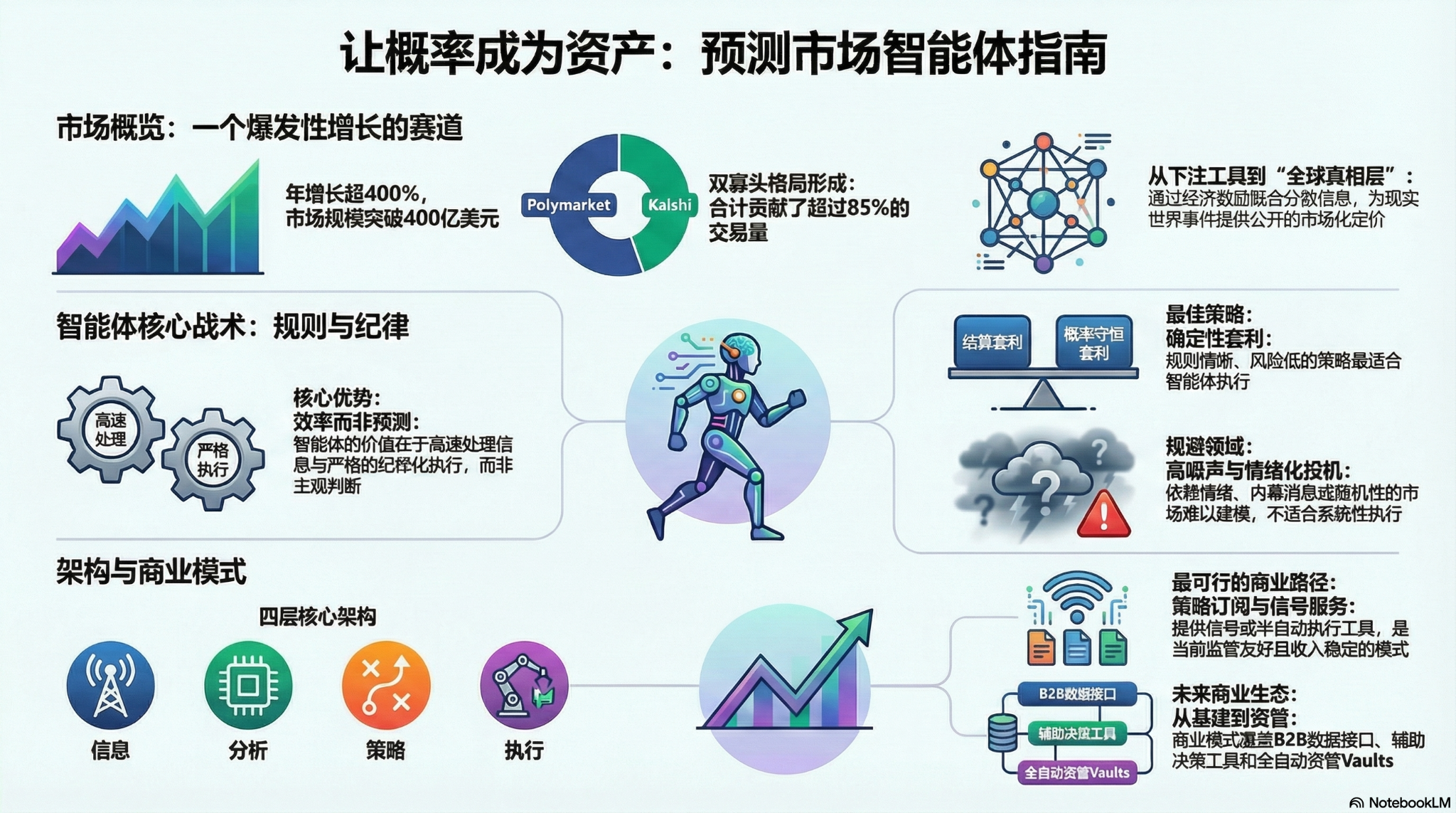

Prediction markets have emerged as an undeniable new industry trend in 2025, with annual total trading volume surging from approximately $9 billion in 2024 to over $40 billion in 2025—a year-on-year growth exceeding 400%. This dramatic expansion has been driven by multiple factors: heightened uncertainty stemming from macro-political events; maturation of infrastructure and trading models; and regulatory breakthroughs (e.g., Kalshi’s legal victory and Polymarket’s return to the U.S.). The Prediction Market Agent has taken early shape at the beginning of 2026 and is poised to become an emerging product category in the agent space over the coming year.

I. Prediction Markets: From Betting Tools to a “Global Truth Layer”

A prediction market is a financial mechanism for trading contracts tied to the outcomes of future events, where contract prices essentially reflect the collective market judgment on the probability of those outcomes. Its effectiveness arises from the synergy between collective intelligence and economic incentives: in an anonymous, real-money betting environment, dispersed information is rapidly aggregated into price signals weighted by participants’ capital commitments—significantly reducing noise and false judgments.

Nominal trading volume trend for prediction markets

Data source: Dune Analytics (Query ID: 5753743)

By the end of 2025, the prediction market landscape had largely consolidated into a duopoly led by Polymarket and Kalshi. According to Forbes, total trading volume in 2025 reached approximately $44 billion, with Polymarket contributing roughly $21.5 billion and Kalshi around $17.1 billion. Weekly data from February 2026 shows Kalshi’s trading volume ($25.9B) has surpassed Polymarket’s ($18.3B), nearing a 50% market share. Kalshi’s rapid expansion stems from its legal victory in the election contract case, its first-mover advantage in compliant U.S. sports prediction markets, and relatively clear regulatory expectations. Today, their development paths have clearly diverged:

- Polymarket adopts a hybrid CLOB architecture combining off-chain order matching with on-chain settlement and decentralized clearing, building a global, non-custodial, high-liquidity market. After regaining compliance in the U.S., it operates under a dual-track “onshore + offshore” model;

- Kalshi integrates into the traditional financial system, connecting via API to mainstream retail brokers and attracting deep participation from Wall Street market makers in macro- and data-driven contracts. Its products remain constrained by traditional regulatory processes, resulting in relative lag in addressing long-tail demand and sudden events.

Beyond Polymarket and Kalshi, other competitive players in the prediction market space are evolving along two primary paths:

- The first is the compliant distribution path, embedding event contracts into existing brokerage or large-platform account and clearing systems—leveraging channel coverage, compliance credentials, and institutional trust for competitive advantage (e.g., Interactive Brokers × ForecastEx’s ForecastTrader; FanDuel × CME Group’s FanDuel Predicts). This path offers significant compliance and resource advantages, though products and user scale remain early-stage.

- The second is the Crypto-native on-chain path, represented by platforms like Opinion.trade, Limitless, and Myriad. These leverage points-based mining, short-duration contracts, and media distribution to achieve rapid scaling, emphasizing performance and capital efficiency—but their long-term sustainability and risk-control robustness remain unproven.

The coexistence of traditional finance compliance gateways and crypto-native performance advantages defines the diverse competitive landscape of prediction markets.

Superficially resembling gambling—and fundamentally zero-sum—the key distinction lies in positive externalities: by aggregating dispersed information through real-money trading, prediction markets perform public pricing of real-world events, generating valuable signal layers. Their trajectory is shifting from gaming toward becoming a “global truth layer”: as institutions like CME and Bloomberg integrate, event probabilities are becoming decision-relevant metadata directly callable by financial and enterprise systems—delivering timelier, quantifiable, market-derived truths.

Globally, regulatory approaches to prediction markets are highly fragmented. The U.S. is the only major economy that explicitly classifies them under the financial derivatives regulatory framework. In contrast, Europe, the UK, Australia, and Singapore generally treat them as gambling and are tightening oversight; China and India outright ban them. Future global expansion thus remains contingent on national regulatory frameworks.

II. Architecture Design of Prediction Market Agents

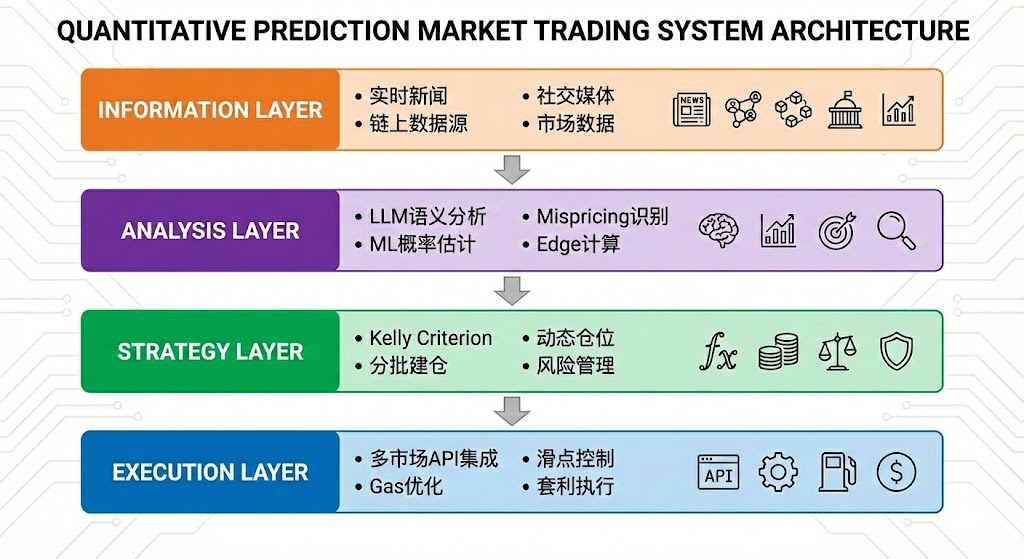

Today, Prediction Market Agents are entering early practical implementation. Their value does not lie in “AI predicting more accurately,” but rather in amplifying information processing and execution efficiency within prediction markets. At its core, a prediction market is an information aggregation mechanism—the price reflects the collective probability judgment. Real-world market inefficiencies stem from information asymmetry, liquidity constraints, and attention scarcity. Thus, the appropriate role for a Prediction Market Agent is executable probabilistic portfolio management: converting news, rule texts, and on-chain data into verifiable pricing discrepancies, executing strategies faster, more systematically, and at lower cost—and capturing structural opportunities through cross-platform arbitrage and portfolio-level risk control.

An ideal Prediction Market Agent can be abstracted into a four-layer architecture:

- The Information Layer aggregates news, social, on-chain, and official data;

- The Analysis Layer employs LLMs and ML to identify mispricing and compute edge;

- The Strategy Layer translates edge into positions using the Kelly Criterion, phased position building, and risk controls;

- The Execution Layer handles multi-market order placement, slippage and gas optimization, and arbitrage execution—forming an efficient, automated closed loop.

III. Strategy Framework for Prediction Market Agents

Unlike traditional trading environments, prediction markets differ significantly in settlement mechanisms, liquidity, and information distribution. Not all markets or strategies are suitable for automation. The core question for a Prediction Market Agent is whether it is deployed in scenarios with clear rules, codifiability, and alignment with its structural advantages. Below, we analyze strategy design across three dimensions: instrument selection, position sizing, and strategy structure.

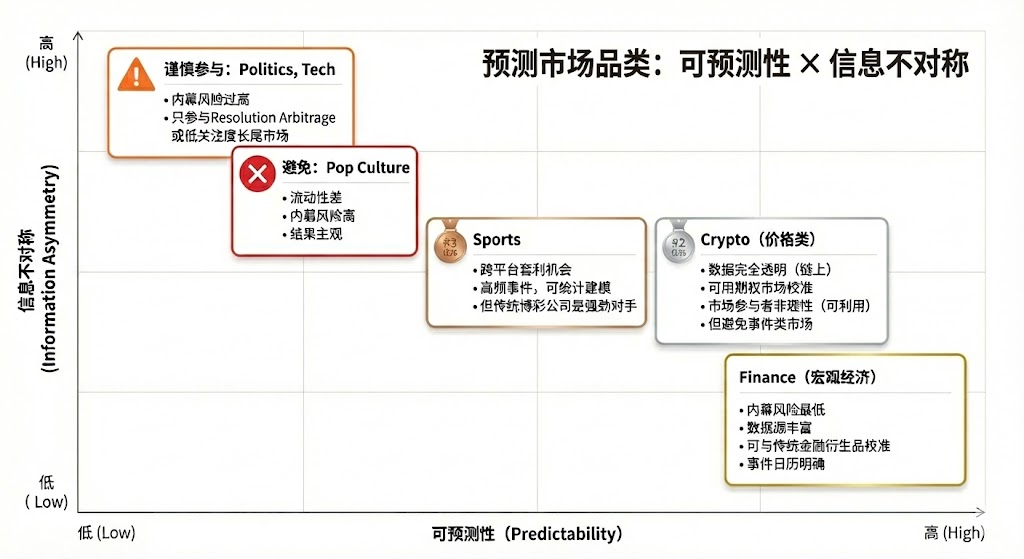

Instrument Selection in Prediction Markets

Not all prediction markets offer tradable value. Their viability depends on: clarity of settlement (clear rules, single authoritative data source), quality of liquidity (market depth, bid-ask spread, volume), insider risk (degree of information asymmetry), temporal structure (time to expiry and event timing), and the trader’s own informational advantage and domain expertise. Only when most dimensions meet baseline requirements does a market warrant participation—and participants should match themselves to markets aligned with their strengths:

- Human core advantages: Domains requiring domain expertise, judgment, and integration of ambiguous information—with relatively relaxed time windows (days/weeks). Typical examples include political elections, macro trends, and corporate milestones.

- AI Agent core advantages: Domains requiring high-speed data processing, pattern recognition, and ultra-rapid execution—with extremely tight decision windows (seconds/minutes). Typical examples include high-frequency crypto price movements, cross-market arbitrage, and automated market making.

- Misaligned domains: Markets dominated by insider information or pure randomness/high manipulation—offering no edge to any participant.

Position Sizing in Prediction Markets

The Kelly Criterion is the most representative capital management theory for repeated games. Its objective is not maximizing single-trade returns, but maximizing the long-term compound growth rate of capital. Based on estimates of win probability and odds, it calculates the theoretically optimal bet size—enhancing capital growth efficiency under positive expected value. It is widely applied in quantitative investing, professional gambling, poker, and asset management.

- Its classic form is:

where f∗ is the optimal betting fraction, b is the net odds, p is the win probability, and q = 1 − p.

- In prediction markets, it simplifies to:

where p is the subjective true probability and market_price is the market-implied probability.

The theoretical validity of the Kelly Criterion heavily depends on accurate estimation of true probability and odds. In practice, traders rarely sustainably estimate true probability precisely. Consequently, professional gamblers and prediction market participants often prefer more executable, less probability-dependent, rule-based approaches:

- Unit System: Capital is divided into fixed units (e.g., 1% of portfolio), with varying numbers of units allocated based on confidence level—automatically capping per-trade risk. This is the most common practical method.

- Fixed Fraction Betting: A fixed percentage of capital is wagered each time—emphasizing discipline and stability, suitable for risk-averse or low-confidence environments.

- Confidence Tiers: Discrete position tiers are predefined with absolute caps—reducing decision complexity and avoiding the “false precision” pitfalls of Kelly modeling.

- Inverted Risk Approach: Position size is derived backward from maximum tolerable loss—starting from risk constraint rather than return expectation—to establish stable risk boundaries.

For Prediction Market Agents, strategy design should prioritize executability and stability over theoretical optimality. Key criteria include clear rules, simple parameters, and tolerance to judgment error. Under these constraints, Confidence Tiers combined with a fixed position cap is the most universally suitable position-sizing framework for PM Agents. It avoids reliance on precise probability estimates, instead categorizing opportunities into limited tiers based on signal strength—each mapped to a fixed position size—and enforcing explicit caps even in high-confidence scenarios.

Strategy Selection in Prediction Markets

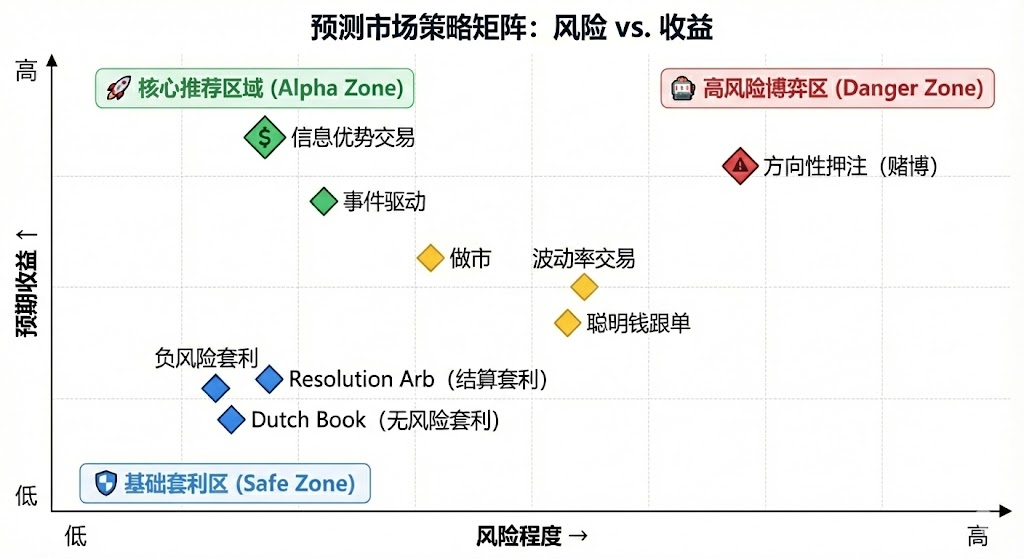

From a structural perspective, prediction market strategies fall mainly into two categories: deterministic arbitrage strategies (Arbitrage), characterized by clear rules and codifiability; and speculative directional strategies (Speculative), relying on information interpretation and directional judgment. Additionally, market-making and hedging strategies exist—primarily employed by professional institutions and demanding substantial capital and infrastructure.

Deterministic Arbitrage Strategies (Arbitrage)

- Resolution Arbitrage: Occurs when an event outcome is effectively certain but the market hasn’t fully priced it yet. Returns derive primarily from information synchronization speed and execution latency. With clear rules, low risk, and full codifiability, this is the most suitable core strategy for Agent execution in prediction markets.

- Dutch Book Arbitrage: Exploits structural imbalances where the sum of prices for mutually exclusive and exhaustive event sets violates probability conservation (∑P ≠ 1), locking in directionally neutral profits via combinatorial positioning. Relying solely on rules and price relationships, it carries low risk and is highly rule-based—making it a classic deterministic arbitrage form well-suited to Agent automation.

- Cross-Platform Arbitrage: Profits from pricing discrepancies for identical events across different markets. Low-risk but demanding high-speed, parallel monitoring and low-latency infrastructure. Suitable for Agents with infrastructural advantages—though intensifying competition continuously erodes marginal returns.

- Bundle Arbitrage: Trades pricing inconsistencies among related contracts. Logically clear but limited in opportunity frequency. Executable by Agents, though requiring moderate engineering effort for rule parsing and combinatorial constraints—medium Agent suitability.

Speculative Directional Strategies (Speculative)

- Structured Information Trading: Focuses on well-defined events or structured information—e.g., official data releases, announcements, or ruling windows. As long as information sources are clear and triggers definable, Agents excel in monitoring and execution speed/discipline. However, once information evolves into semantic judgment or scenario interpretation, human intervention remains essential.

- Signal Following: Generates returns by tracking historically high-performing accounts or capital flows. Rules are relatively simple and automatable. Core risks include signal decay and reverse-engineering—requiring filtering mechanisms and strict position sizing. Best suited as a supporting strategy for Agents.

- Unstructured / Noise-Driven Strategies: Highly dependent on sentiment, randomness, or behavioral patterns—lacking stable, replicable edge with unstable long-term expected value. Due to modeling difficulty and extreme risk, these are unsuitable for systematic Agent execution and not recommended as long-term strategies.

High-Frequency Price & Liquidity Strategies (Market Microstructure): Demand ultra-short decision windows, continuous quoting, or high-frequency trading—entailing extreme requirements for latency, modeling sophistication, and capital. Though theoretically suitable for Agents, they are often constrained by liquidity and competition intensity in prediction markets—viable only for a select few with significant infrastructural advantages.

Risk Management & Hedging Strategies (Risk Control & Hedging): Do not seek direct returns but aim to reduce overall risk exposure. With clear rules and defined objectives, they serve as foundational, always-on risk control modules.

In summary, strategies suitable for Agent execution concentrate on rule-clear, codifiable, low-subjectivity scenarios. Deterministic arbitrage should serve as the core revenue driver, supplemented by structured information and signal-following strategies, while high-noise and emotion-driven trading must be systematically excluded. Agents’ long-term edge lies in high-discipline execution, speed, and robust risk control.

IV. Business Models & Product Forms of Prediction Market Agents

The ideal business model design for Prediction Market Agents explores distinct directions across different layers:

- Infrastructure Layer: Offers real-time multi-source data aggregation, Smart Money address databases, unified prediction market execution engines, and backtesting tools—charging B2B fees for stable, accuracy-agnostic revenue.

- Strategy Layer: Introduces community- and third-party strategies to build a reusable, evaluable strategy ecosystem—capturing value via invocation, weighting, or execution revenue sharing—reducing dependence on a single alpha source.

- Agent / Vault Layer: Agents directly participate in live trading via fiduciary management, leveraging transparent on-chain records and rigorous risk controls to charge management and performance fees—monetizing proven capability.

Corresponding product forms for these business models include:

- Entertainment / Gamified Model: Intuitive, Tinder-like interaction lowers entry barriers, offering strongest user growth and market education—ideal for breakout adoption, though monetization requires conversion to subscription or execution-based products.

- Strategy Subscription / Signal Model: No fund custody—regulation-friendly, clear responsibilities, with relatively stable SaaS revenue. Currently the most viable commercial path. Limitations include strategy replicability and execution slippage—addressable via semi-automated “signal + one-click execution” enhancements to improve experience and retention.

- Vault Custodial Model: Benefits from scale effects and execution efficiency—akin to asset management products—but faces structural constraints including AM licensing, trust thresholds, and centralized technical risk. Commercial viability heavily depends on market conditions and sustained profitability. Unless backed by long-term track record and institutional credibility, it should not serve as the primary path.

Overall, a diversified revenue structure of “infrastructure monetization + strategy ecosystem expansion + performance participation” helps mitigate overreliance on the singular assumption that “AI will consistently outperform markets.” Even if alpha converges as markets mature, underlying capabilities—execution, risk control, and settlement—retain enduring value, enabling a more sustainable commercial closed loop.

V. Project Case Studies of Prediction Market Agents

Currently, Prediction Market Agents remain in the early exploration stage. While the market has seen diverse attempts—from foundational frameworks to upper-layer tools—no standardized product has yet emerged that is mature across strategy generation, execution efficiency, risk control architecture, and commercial closed-loop design.

We categorize the current ecosystem into three layers: Infrastructure Layer, Autonomous Agents, and Prediction Market Tools.

Infrastructure Layer

Polymarket Agents Framework:

Polymarket Agents An official developer framework launched by Polymarket, designed to solve engineering standardization for “connection and interaction.” It encapsulates market data fetching, order construction, and basic LLM invocation interfaces. It solves “how to place orders programmatically,” but leaves core trading capabilities—strategy generation, probability calibration, dynamic position sizing, and backtesting—largely blank. It functions more as an officially sanctioned “integration specification” than a ready-to-deploy alpha-generating product. Commercial-grade Agents still require building full research and risk control cores atop this foundation.

Gnosis Prediction Market Tools:

Gnosis Prediction Market Agent Tooling (PMAT) Provides full read/write support for Omen/AIOmen and Manifold, but only read-only access for Polymarket—highlighting clear ecosystem fragmentation. It serves well as a development base for Gnosis-ecosystem Agents, but offers limited practicality for developers focused primarily on Polymarket.

Polymarket and Gnosis are currently the only prediction market ecosystems that have explicitly productized “Agent development” as official frameworks. Other prediction markets—including Kalshi—remain largely at the API and Python SDK level, requiring developers to independently implement critical systems for strategy, risk control, runtime, and monitoring.

Autonomous Agents

Current “Prediction Market AI Agents” remain largely in early stages. Though branded as “Agents,” their actual capabilities fall significantly short of fully delegated, automated closed-loop trading. They commonly lack independent, systematic risk control layers; fail to incorporate position sizing, stop-loss, hedging, and expected-value constraints into decision logic; and exhibit low overall productization—no mature, long-running system has yet emerged.

Olas Predict: The most productized prediction market Agent ecosystem to date. Its flagship product, Omenstrat, is built atop Gnosis’s Omen—utilizing FPMM and decentralized arbitration, supporting small, frequent interactions—but constrained by Omen’s single-market liquidity limitations. Its “AI predictions” rely primarily on general-purpose LLMs, lacking real-time data and systematic risk controls; historical win rates vary markedly across categories. In February 2026, Olas launched Polystrat, extending Agent capabilities to Polymarket—users define strategies in natural language, and the Agent automatically identifies and executes trades on probability deviations in markets settling within four days. The system runs locally via Pearl, uses self-hosted Safe accounts, and enforces hard-coded limits—making it the first consumer-grade autonomous trading Agent for Polymarket.

UnifAI Network Polymarket Strategy: Offers a Polymarket automated trading Agent centered on a tail-risk-bearing strategy: scanning near-settlement contracts with implied probability >95% and buying them to capture 3–5% spreads. On-chain data shows win rates approaching 95%, but returns vary significantly across categories—strategy efficacy highly dependent on execution frequency and category selection.

NOYA.ai Aims to integrate “research → judgment → execution → monitoring” into a closed Agent loop, with architecture spanning intelligence, abstraction, and execution layers. Omnichain Vaults have already been delivered; the Prediction Market Agent remains under development—yet to achieve full mainnet closed-loop operation—currently in vision-validation phase.

Prediction Market Tools

Current prediction market analytics tools fall short of constituting complete “Prediction Market Agents.” Their value concentrates in the information and analysis layers of the Agent architecture, leaving trade execution, position management, and risk control to users. Product-wise, they align more closely with “strategy subscription / signal assistance / research augmentation”—serving as early prototypes of full-fledged Prediction Market Agents.

Through systematic review and empirical screening of projects listed in Awesome-Prediction-Market-Tools, this report selects representative projects that have achieved preliminary product form and real-world usage. Focus areas include: analysis & signal layers, alert & whale-tracking systems, arbitrage discovery tools, and trading terminals & aggregated execution platforms.

Market Analysis Tools

- Polyseer: A research-oriented prediction market tool employing a multi-Agent division-of-labor architecture (Planner / Researcher / Critic / Analyst / Reporter) for bilateral evidence gathering and Bayesian probability aggregation—producing structured research reports. Strengths include transparent methodology, engineered workflows, and full open-source auditability.

- Oddpool: Positioned as the “Bloomberg Terminal for prediction markets,” offering cross-platform aggregation (Polymarket, Kalshi, CME), arbitrage scanning, and real-time data dashboards.

- Polymarket Analytics: A global Polymarket data analytics platform systematically presenting trader, market, position, and trade data—clearly positioned and intuitively visualized, ideal for foundational data queries and research reference.

- Hashdive: A trader-focused data tool using Smart Score and multi-dimensional screeners to quantitatively filter traders and markets—practical for “smart money identification” and copy-trading decisions.

- Polyfactual: Focuses on AI-powered market intelligence and sentiment/risk analysis—embedding analytical outputs into trading interfaces via Chrome extension, oriented toward B2B and institutional users.

- Predly: An AI-driven mispricing detection platform comparing market prices against AI-calculated probabilities to identify pricing deviations on Polymarket and Kalshi—officially claiming 89% alert accuracy, targeting signal discovery and opportunity screening.

- Polysights: Covers 30+ markets and on-chain metrics, with Insider Finder tracking new wallets and large single-bet placements—suited for daily monitoring and signal discovery.

- PolyRadar : A multi-model parallel analysis platform delivering real-time interpretations, timeline evolution, confidence scoring, and source transparency for individual events—emphasizing cross-AI validation, positioned as an analytical tool.

- Alphascope: An AI-driven prediction market intelligence engine providing real-time signals, research summaries, and probability change monitoring—still early-stage, oriented toward research and signal support.

Alerts / Whale Tracking

- Stand: Explicitly targets whale-following and high-confidence action alerts.

- Whale Tracker Livid: Productizes whale position changes.

Arbitrage Discovery Tools:

- ArbBets: An AI-driven arbitrage discovery tool focusing on Polymarket, Kalshi, and sports betting markets—identifying cross-platform arbitrage and positive expected value (+EV) opportunities, positioned at the high-frequency opportunity scanning layer.

- PolyScalping : A real-time arbitrage and scalping analysis platform for Polymarket—scanning all markets every 60 seconds, calculating ROI, pushing alerts via Telegram, and enabling filtering by liquidity, spread, and volume—targeting active traders.

- Eventarb: A lightweight cross-platform arbitrage calculation and alert tool covering Polymarket, Kalshi, and Robinhood—focused functionality, free to use, suitable as a foundational arbitrage assistant.

- Prediction Hunt: A cross-exchange prediction market aggregation and comparison tool providing real-time price comparisons and arbitrage identification (refreshed ~every 5 minutes) across Polymarket, Kalshi, and PredictIt—positioned for information symmetry and market inefficiency discovery.

Trading Terminals / Aggregated Execution

- Verso: An institutional-grade prediction market trading terminal supported by YC Fall 2024—featuring a Bloomberg-style interface, real-time tracking of 15,000+ contracts across Polymarket and Kalshi, deep data analytics, and AI-powered news intelligence—targeting professional and institutional traders.

- Matchr: A cross-platform prediction market aggregation and execution tool covering 1,500+ markets—using smart routing for optimal price matching, and planning automated yield strategies based on high-probability events, cross-market arbitrage, and event-driven triggers—focused on execution and capital efficiency.

- TradeFox: A professional prediction market aggregation and prime brokerage platform backed by Alliance DAO and CMT Digital—offering advanced order execution (limit, take-profit/stop-loss, TWAP), self-custodial trading, and multi-platform smart routing—positioned for institutional traders, with planned expansion to Kalshi, Limitless, SxBet, and others.

VI. Summary & Outlook

Currently, Prediction Market Agents are in the early exploratory phase of development.

- Market Foundation & Evolutionary Essence: Polymarket and Kalshi have formed a duopoly, providing ample liquidity and use-case foundations for Agent development. The core distinction between prediction markets and gambling lies in positive externalities—aggregating dispersed information through real trading to publicly price real-world events, gradually evolving into a “global truth layer”.

- Core Positioning: Prediction Market Agents should be positioned as executable probabilistic portfolio management tools. Their core task is transforming news, rule texts, and on-chain data into verifiable pricing discrepancies—and executing strategies with greater discipline, lower cost, and cross-market capability. The ideal architecture abstracts into four layers: information, analysis, strategy, and execution—but real-world tradability remains highly dependent on settlement clarity, liquidity quality, and information structuring.

- Strategy Selection & Risk Control Logic: Strategically, deterministic arbitrage (including resolution arbitrage, Dutch book arbitrage, and cross-platform spread trading) is best suited for Agent automation, while directional speculation serves only as supplementary. For position sizing, executability and fault tolerance should be prioritized—Confidence Tiers combined with a fixed position cap is optimal.

- Business Model & Prospects: Commercialization unfolds across three tiers: Infrastructure generates stable B2B revenue from data and execution infrastructure; Strategy monetizes via third-party strategy invocation or revenue sharing; Agent/Vault participates in live trading under transparent on-chain risk controls, charging management and performance fees. Corresponding forms include entertainment-oriented entry points, strategy subscriptions/signals (most viable today), and high-barrier Vault custody. A “infrastructure + strategy ecosystem + performance participation” approach offers superior sustainability.

Although the Prediction Market Agent ecosystem has seen diverse attempts—from foundational frameworks to upper-layer tools—no mature, replicable, standardized product yet exists across critical dimensions including strategy generation, execution efficiency, risk control, and commercial closed-loop design. We look forward to the iteration and evolution of Prediction Market Agents in the future.

Disclaimer: This article was assisted during creation by AI tools including ChatGPT-5.2, Gemini 3, and Claude Opus 4.5. The author has made every effort to verify and ensure factual accuracy, but minor oversights may remain. Please accept our apologies. It is especially important to note that in cryptocurrency markets, fundamental project attributes frequently diverge from secondary market price performance. This article is intended solely for information consolidation and academic/research exchange—not as investment advice nor as a recommendation to buy or sell any token.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News