Why is ETH treasury said to have more growth potential than Strategy?

TechFlow Selected TechFlow Selected

Why is ETH treasury said to have more growth potential than Strategy?

How to choose between the two giants SBET and BMNR?

Author: Kevin, Co-Investment Director at Penn Blockchain

Translation: Azuma from Odaily (@azuma_eth)

Although the crypto community has long been enthusiastic about tokenizing traditional assets and bringing them on-chain, recent breakthroughs have actually come from the reverse integration—bringing crypto assets into traditional securities. The public market's current enthusiasm for "crypto treasury" stocks perfectly illustrates this trend.

Michael Saylor pioneered this strategy through MicroStrategy (MSTR), pushing its market capitalization beyond $100 billion—a rise that even outpaced NVIDIA during the same period. We previously analyzed this in depth in our dedicated report on MicroStrategy (an excellent resource for newcomers to the treasury space). The core logic of such treasury strategies lies in the fact that publicly listed companies can access low-cost, unsecured leverage unavailable to ordinary traders.

Recently, market attention has expanded from BTC treasuries to ETH treasuries, exemplified by Sharplink Gaming (SBET) led by Joseph Lubin and BitMine (BMNR) chaired by Thomas Lee.

But is an ETH treasury truly justified? As argued in our MicroStrategy analysis, treasury companies are essentially attempting to arbitrage the spread between the long-term compound annual growth rate (CAGR) of the underlying asset and their cost of capital. In earlier writings, we outlined our view on ETH’s long-term CAGR: as a programmable, scarce reserve asset, ETH plays a foundational role in securing the economic safety of blockchain networks as more assets migrate on-chain. This article will explain the overarching bullish case for ETH treasuries and offer strategic guidance for companies adopting this model.

Liquidity Access: The Foundation of Treasury Companies

One primary reason tokens and protocols seek to establish these treasury companies is to unlock traditional finance (TradFi) liquidity for their tokens—especially amid declining altcoin liquidity. These treasury firms primarily raise liquidity to accumulate assets through three channels. Notably, all such liquidity/debt is unsecured and non-redeemable ahead of schedule.

-

Convertible bonds: Debt financing where proceeds are used to purchase additional cryptocurrency, with the debt convertible into equity;

-

Preferred equity: Fundraising via issuing preferred shares that pay fixed annual dividends;

-

At-the-market (ATM) offerings: Direct issuance of new shares in public markets to generate flexible, real-time funding for crypto purchases.

Advantages of ETH Convertible Bonds

In our prior research on MicroStrategy, we highlighted two key benefits convertible bonds offer institutional investors:

Downside protection with upside exposure: Allows institutions to gain exposure to the underlying asset (e.g., BTC or ETH) while retaining the protective features inherent to bonds;

Volatility-driven arbitrage opportunities: Hedge funds often profit from volatility in both the underlying asset and its associated securities using gamma trading strategies.

Gamma traders (hedge funds) now dominate the convertible bond market. Compared to BTC, ETH exhibits higher historical and implied volatility. Convertible bonds (CBs) issued by ETH treasury companies naturally reflect this elevated volatility, making them more attractive to arbitrageurs and hedge funds. More importantly, this volatility enables ETH treasury firms to issue convertibles at higher valuations and under more favorable financing terms.

Odaily Note: Historical volatility comparison between ETH and BTC.

For convertible bond holders, higher volatility means greater profit potential through gamma strategies. Simply put, the greater the underlying asset’s volatility, the richer the gamma trading profits—giving ETH treasury convertibles a distinct edge over BTC treasury equivalents.

Odaily Note: Historical volatility comparison among SBET, BMNR, and MSTR.

However, a critical caveat exists: if ETH fails to maintain long-term compound growth, appreciation in the underlying asset may be insufficient to meet conversion thresholds before maturity. In such cases, the treasury company faces full repayment risk. By contrast, BTC’s more established long-term performance makes this scenario less likely—historical data shows most BTC-based convertibles ultimately convert into equity.

Odaily Note: Four-year CAGR comparison between ETH and BTC.

The Unique Value of ETH Preferred Shares

Unlike convertible bonds, preferred shares are designed for fixed-income investors. While certain convertible preferred shares offer hybrid upside potential, yield remains the primary consideration for most institutional investors. Pricing for these instruments depends on credit risk—the ability of the treasury company to reliably service interest payments.

A key advantage of the MicroStrategy model is using ATM offerings to fund interest payments. Since this typically represents only 1–3% of market cap, dilution risk is minimal. However, this mechanism still relies on the market liquidity and volatility of both BTC and MicroStrategy’s securities.

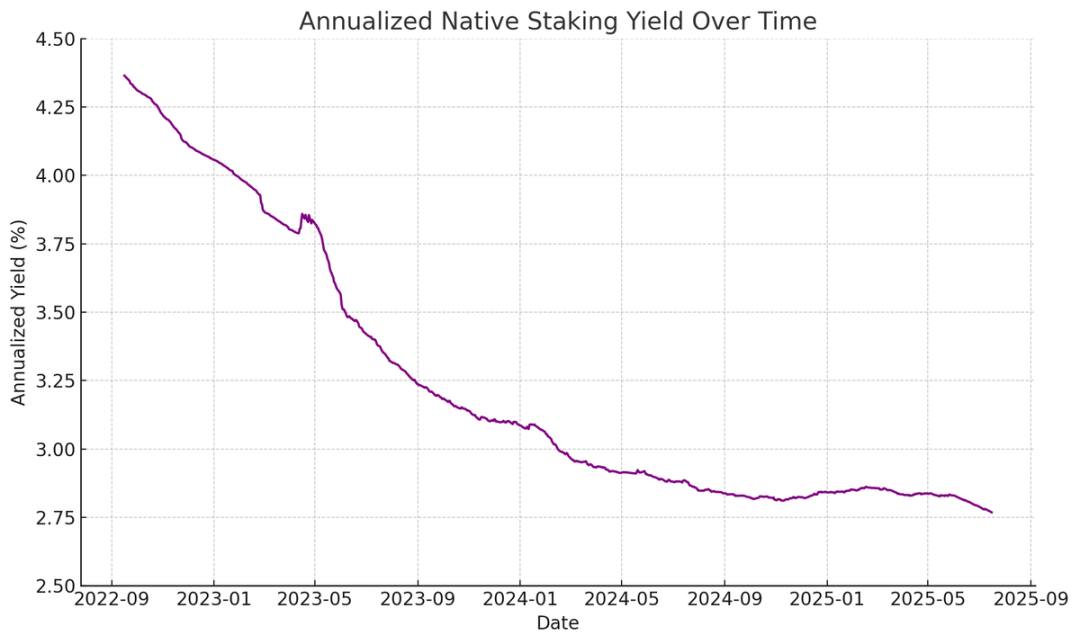

ETH, however, generates native yield through staking, restaking, and lending, providing stronger certainty for interest payments and theoretically warranting higher credit ratings. Unlike BTC, which relies solely on price appreciation, ETH offers returns combining long-term CAGR expectations with protocol-level native yield.

Odaily Note: Annualized native staking yield of ETH.

My proposed innovation is that ETH preferred shares could serve as non-directional investment vehicles, enabling institutions to support network security without taking direct ETH price exposure. As emphasized in our ETH reports, maintaining at least 67% honest validators is crucial for network security. As more assets go on-chain, institutional support for Ethereum’s decentralization and security becomes increasingly important.

Many institutions may hesitate to go long ETH directly, but ETH treasury companies can act as intermediaries—absorbing directional risk while offering institutions fixed-income-like returns. The on-chain preferred shares issued by SBET and BMNR are precisely designed as fixed-yield staking products, enhanced with bundled protocol incentives to appeal to investors seeking stable returns without full market exposure.

Special Advantages of ATM Offerings for ETH Treasuries

The key valuation metric for treasury companies, mNAV (market-to-net-asset-value ratio), is conceptually similar to the P/E ratio and reflects how the market prices future per-share asset growth. ETH treasuries naturally command a higher mNAV premium due to their native yield mechanisms—these activities generate recurring "earnings" or increase ETH per share without requiring additional capital. In contrast, BTC treasuries must rely on synthetic yield strategies (e.g., issuing convertibles or preferred shares), making it difficult to justify any earnings when market premiums approach NAV.

More importantly, mNAV exhibits reflexivity—higher mNAV allows treasury companies to raise capital more efficiently via ATM offerings. They issue shares at a premium, use proceeds to acquire more underlying assets, thereby increasing per-share asset value and creating a positive feedback loop. The higher the mNAV, the stronger the value capture, making ATM offerings particularly effective for ETH treasury firms.

Capital access is another critical factor. Firms with deeper liquidity and broader fundraising capabilities naturally achieve higher mNAVs, while those with limited market access tend to trade at discounts. Thus, mNAV often reflects a liquidity premium—the market’s confidence in a company’s ability to secure further liquidity.

First-Principles Screening of Treasury Companies

ATM offerings can be viewed as retail fundraising, whereas convertibles and preferred shares typically target institutional investors. Therefore, a successful ATM strategy hinges on building a strong retail base, which usually requires credible and charismatic leadership along with consistent, transparent strategic disclosure to earn long-term trust. Conversely, convertibles and preferred shares require robust institutional distribution channels and relationships within capital markets. Based on this logic, I believe SBET holds a retail-driven advantage (thanks to Joe Lubin’s leadership and the team’s ongoing transparency in growing ETH per share), while BMNR is better positioned to access institutional liquidity through Tom Lee’s deep connections in traditional finance.

Ecosystem Significance and Competitive Landscape of ETH Treasuries

One of Ethereum’s biggest challenges is the growing concentration of validators and staked ETH—primarily within liquid staking protocols like Lido and centralized exchanges like Coinbase. ETH treasuries help counteract this trend by promoting validator decentralization. To enhance long-term resilience, these companies should distribute their ETH across multiple staking providers and, where possible, operate their own validator nodes.

Odaily Note: Distribution of Ethereum staking categories.

In this context, I believe the competitive landscape for ETH treasuries will fundamentally differ from that of BTC treasuries. The Bitcoin ecosystem has become winner-takes-all (MicroStrategy’s holdings exceed the second-largest corporate holder by more than 10x), dominating the convertible and preferred share markets through first-mover advantage and narrative control. ETH treasuries, however, are starting from scratch, with no single dominant entity and multiple projects advancing in parallel. This lack of first-mover advantage is not only healthier for the network but also fosters a more competitive and accelerated development environment. Given that leading companies hold comparable amounts of ETH, SBET and BMNR are likely to form a duopoly.

Odaily Note: Comparison of ETH treasury company holdings.

Valuation Framework: A Hybrid of MicroStrategy and Lido

Broadly speaking, the ETH treasury model resembles a fusion of MicroStrategy and Lido tailored for traditional finance. Unlike Lido, ETH treasury firms hold the underlying assets directly, capturing a larger portion of asset appreciation and significantly outperforming Lido in value accumulation.

As a rough valuation benchmark, Lido currently manages around 30% of staked ETH, with an implied valuation exceeding $30 billion. We believe that within one market cycle (four years), SBET and BMNR could collectively surpass Lido in scale, driven by the speed, depth, and reflexivity of capital flows from traditional finance—as demonstrated by MicroStrategy’s growth trajectory.

To add context, Bitcoin’s market cap stands at $2.47 trillion, while Ethereum’s is $428 billion (approximately 17–20% of Bitcoin’s). If SBET and BMNR each reach 20% of MicroStrategy’s $120 billion valuation, their combined long-term value would amount to roughly $24 billion. Currently, their combined valuation is under $8 billion, indicating substantial room for growth as the ETH treasury model matures.

Conclusion

The emergence and evolution of digital asset treasuries represent a major step forward in the convergence of crypto markets and traditional finance, with ETH treasuries emerging as a powerful new force. Ethereum’s unique advantages—including higher convertible bond volatility and native yield for preferred shares—create differentiated growth opportunities for treasury firms. Their ability to promote validator decentralization and foster competition further distinguishes them from the BTC treasury “sovereign debt” ecosystem.

The combination of MicroStrategy-style capital efficiency with ETH’s embedded yield has the potential to unlock tremendous value and drive deeper integration of on-chain economies into traditional finance. Rapid expansion and growing institutional interest signal a transformative impact on both crypto and capital markets in the years ahead.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News