Opinion: Listed companies raising funds to buy Bitcoin is a "toxic" leverage

TechFlow Selected TechFlow Selected

Opinion: Listed companies raising funds to buy Bitcoin is a "toxic" leverage

Issuing more common stock dilutes existing shareholders' equity, and this leverage will eventually come due.

Author: lowstrife, crypto KOL

Translation: Felix, PANews

Recently, companies like MSTR, Metaplanet, Twenty One, and Nakamoto that hold Bitcoin reserves have gained fame. However, in my opinion, their "reserves" represent destructive leverage—the worst thing to ever happen to Bitcoin and what it stands for. Below is an analysis of how this model collapses under certain conditions.

The feedback loop these companies use involves purchasing Bitcoin with corporate funds, recording it on the balance sheet, then leveraging various corporate mechanisms to raise more capital based on that balance sheet. This model is widely praised as the greatest invention in history.

Funds raised through new share issuance (ATM), bonds, preferred shares, loans, etc., are immediately used to buy Bitcoin, driving this flywheel.

A key distinction here is the use of appreciation-based leverage: companies like Tesla simply hold assets in Bitcoin (which I personally have no issue with).

But the crux of this flywheel is that common shareholders are the ultimate holders of these financial assets. All these fundraising mechanisms ultimately lead to dilution of common shares—selling stock into the market to fund the flywheel.

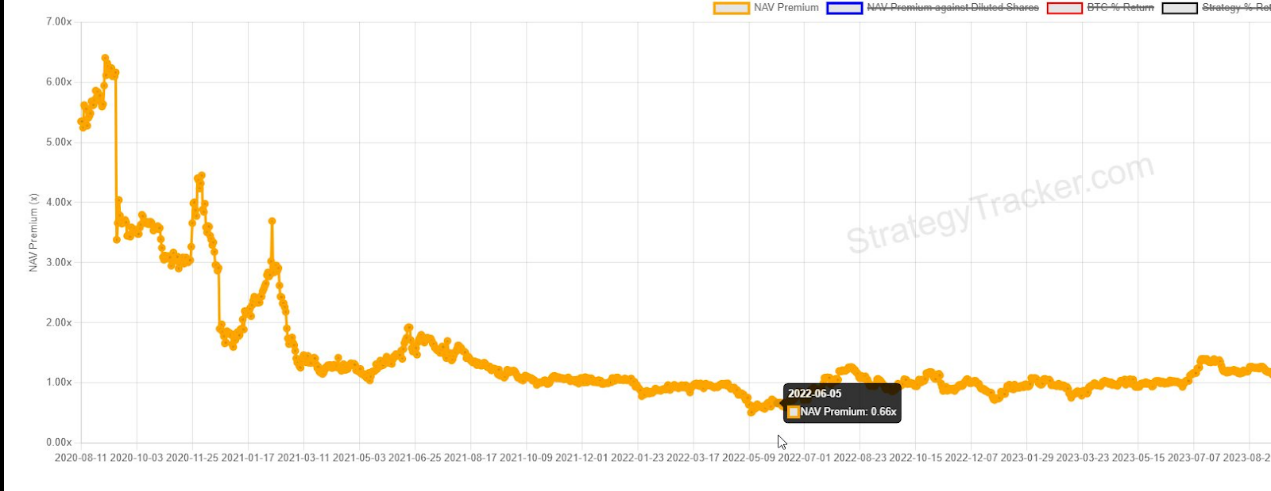

MSTR’s primary method is issuing new shares (ATM) to achieve appreciative dilution. This works well if mNAV (PANews note: representing the ratio between current stock price and the value of its Bitcoin holdings) is greater than 1.0. But the problem is this leverage depends on issuing new shares to meet cash flow needs. If MSTR's stock price falls below 1.0x mNAV (as it did in 2022), problems arise.

Another tool is using leverage to boost product yields, such as convertible bonds and perpetual preferred stock. Because future buy-ins are expected, they accelerate anticipated equity value and amplify share premiums upfront.

Issuing more common stock and diluting existing shareholders, this leverage eventually comes due. But they allow dilution to occur later, exchanging today’s dollars for tomorrow’s cash flows/dilution, postponing these payments and “costs” far into the future. How “clever”.

There are two main issues here:

The first issue is that if the underlying stock fails to meet performance targets, these products cannot serve as levers. For convertible bonds, MSTR must refinance or sell BTC to raise cash.

The second issue is preferred stock. They require paying permanent, non-appreciating dividends (i.e., interest) to debt holders. MSTR plans to issue trillions of dollars worth of such securities, with payments funded by diluting MSTR equity holders.

In particular, Strategy’s STRF (PANews note: a fixed-income product packaged as preferred stock to easily and continuously raise funds to buy Bitcoin) has no maturity date, acts as perpetual debt, and carries a 10% annual interest rate. MSTR will forever rely on non-appreciating ATM issuance, diluting shareholders, to finance every dollar issued. Today’s purchases come at the expense of tomorrow’s shareholders. Does this sound familiar?

The problem with using ATM to generate required cash flow is that it relies on mNAV, which does not originate from its own assets. It is entirely dependent on market sentiment: what people believe the treasury is worth.

This is nothing short of an insult to Bitcoin’s essence.

Although there are provisions allowing dividend suspension, this creates even more problems. STRK must pay all accrued dividends plus penalties before conversion (at maturity). Not to mention, suspending dividends drastically reduces product demand.

If the purpose of yield-bearing assets is risk mitigation, the last thing you want is to destroy the very reason for holding them. These risks are never mentioned by MSTR proponents. Dividend suspension would be a solvency warning.

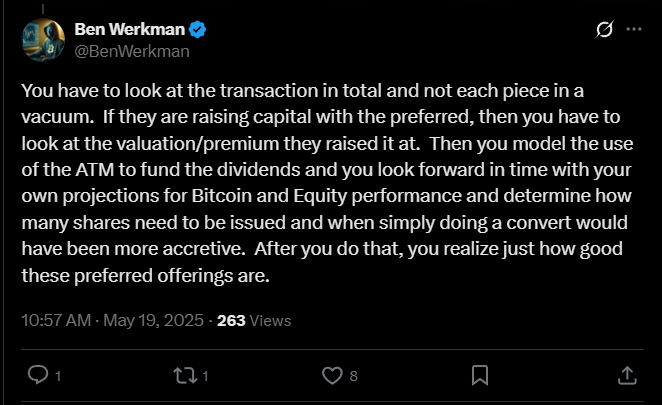

Supporters argue that issuing preferred stock enables immediate Bitcoin purchases, and dividend payments are justified. They claim that if they’ve already “modeled it,” raising funds is worthwhile.

You must view the deal holistically, not in isolation. If they finance via preferred stock, you must consider the valuation/premium at the time of financing. Then, you can simulate using ATM to pay dividends, project forward based on your forecasts of Bitcoin and stock performance, determine how many shares need to be issued, and when conversion becomes more accretive. Once you do this, you realize just how bad these preferred stock issuances truly are.

Currently, about $1.8 billion of such securities are outstanding, making payments still feasible. But Saylor proposes issuing $3 trillion of such securities, requiring $300 billion in annual shareholder dilution—clearly unsustainable.

So how does this all blow up? It starts with mNAV—mNAV is critical. It is life, it is vitality. If mNAV falters, the company’s ability to raise funds disappears, debt conversions harm mNAV, and the company loses its ability to repay debts.

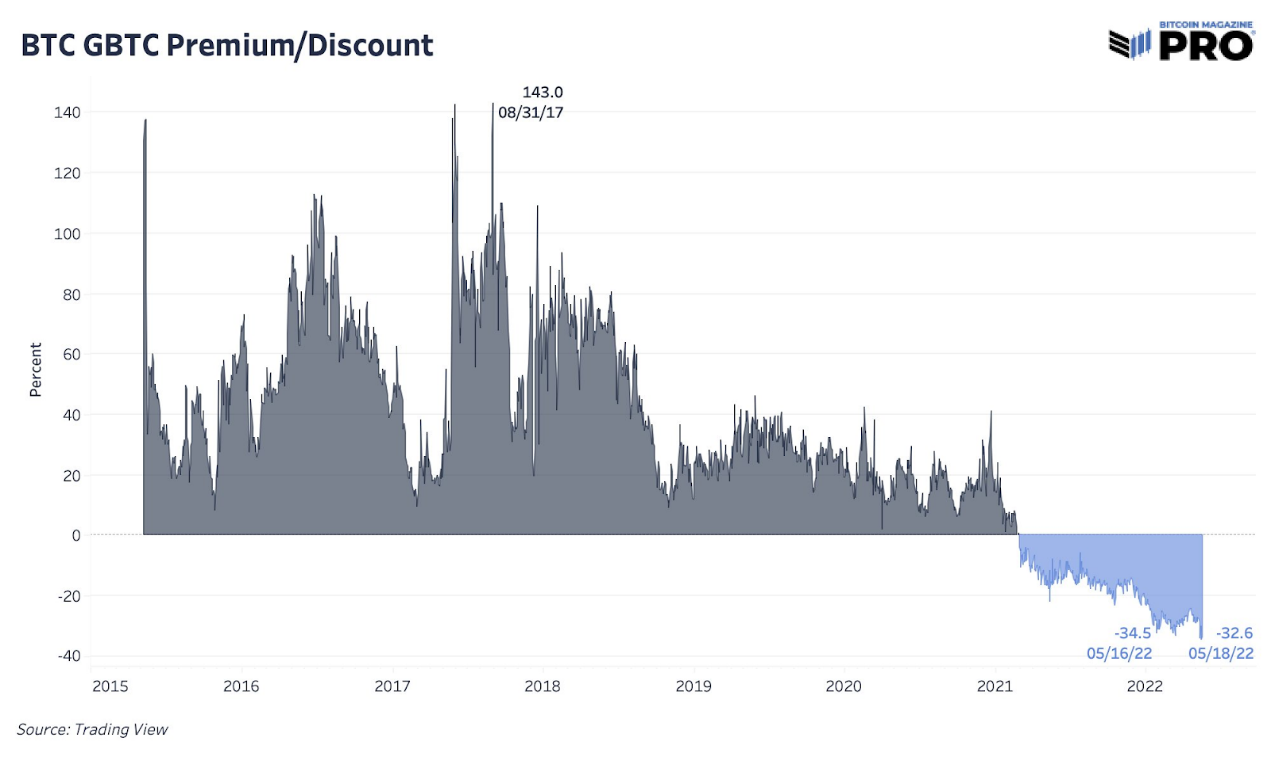

GBTC was another closed-end fund that surged during the 2021 bull market. People used it to invest in BTC because their existing accounts didn’t allow direct access.

Today, MSTR is bought for largely similar reasons. The problem is: Bitcoin access channels are multiplying.

GBTC is a closed-end fund whose price trades at a premium or discount to its underlying asset. Once demand for this investment vehicle dries up, so does the fund’s need to purchase new assets.

Once mNAV collapses, demand vanishes.

Once mNAV falls below 1.0, MSTR’s fundraising ability will falter, much like GBTC’s loss of buying intent and capacity.

Notably, mNAV is entirely based on market sentiment. There is no mechanism or rationale requiring it to trade at asset value.

When mNAV declines, the ability to continue raising funds (and buying Bitcoin) weakens, and the stock’s expected value drops accordingly. This could be exacerbated if debt dividends are forced under unfavorable conditions.

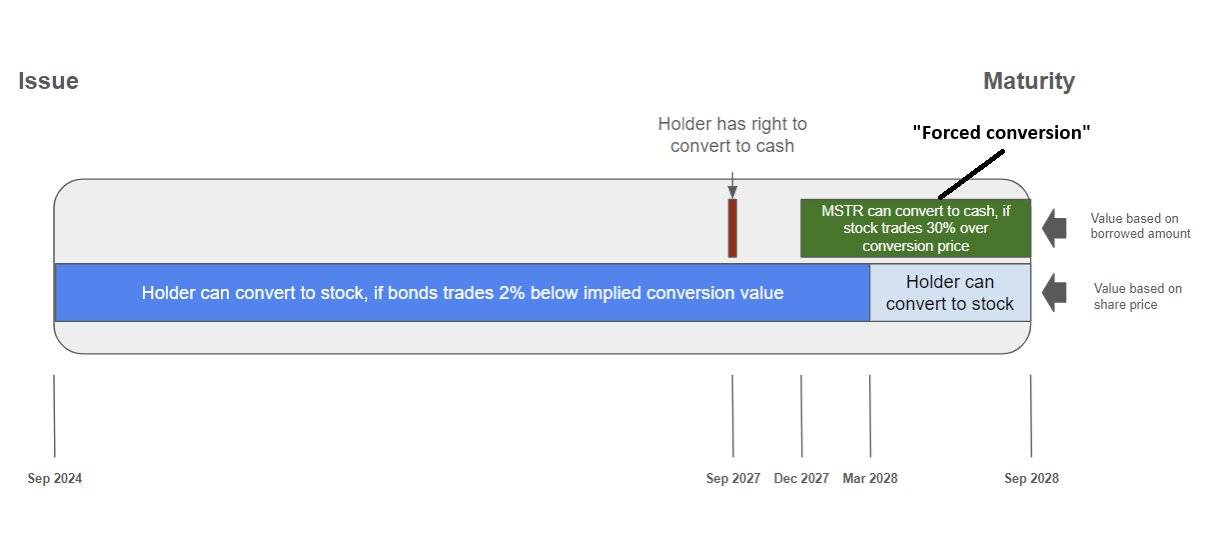

Convertible bonds make things more complicated. Currently, MSTR holds $8.2 billion in convertible bonds maturing between 2028 and 2032. The risk here isn’t price-related; regardless of Bitcoin’s price movement (within reasonable bounds), the bonds won’t “blow up” or face margin calls.

The issue with convertible bonds lies in the name—they must convert. MSTR’s stock needs to appreciate to predetermined price levels for the bonds to convert into new share issuance. Remember: this trigger point is MSTR’s stock price, which floats on mNAV, which itself depends on market sentiment.

If for some reason prices fail to rise, the issue becomes one of time, not price. Regardless of Bitcoin’s underlying price, the bonds may mature. MSTR must refinance or sell BTC to repay the debt in cash.

Ultimately, the flywheel reverses, rendering the entire scheme ineffective. Repurchasing shares trading below mNAV 1.0 and selling underlying assets to raise cash. Some argue this is a fiduciary duty, and Bailey has publicly stated he would do the same.

This isn’t financial revolution. It’s Ponzi enthusiasts chasing leverage. I’ve held Bitcoin personally for a long time, and it pains me to see Bitcoin OGs cheering for Saylor while he reenacts the 2008 financial engineering playbook using Bitcoin—the very system that led to Bitcoin’s creation.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News