Which crypto VCs are the ultimate power couples, teaming up to co-invest in projects?

TechFlow Selected TechFlow Selected

Which crypto VCs are the ultimate power couples, teaming up to co-invest in projects?

Past co-investments do not necessarily translate into future collaboration; during frenzied periods, co-investments tend to increase.

Author: @shloked_ and @joel_john95

Translation: TechFlow

This is a condensed version of our newsletter published on Decentralised.co. We examined how crypto venture capital firms (VCs) choose co-investors and analyzed historical patterns in their investment strategies. The related tool is available here.

As an asset class, venture capital follows an extreme power law. Yet the specifics of this phenomenon haven't been deeply studied, as we're constantly chasing the latest narratives. Over recent weeks, we've built an internal tool to track the networks of all crypto VCs. But why?

The core logic is simple. As a founder, knowing which VCs frequently co-invest can save time and optimize your fundraising strategy. Each deal is a fingerprint. When visualized on a chart, these fingerprints reveal underlying stories.

In other words, we can trace the nodes responsible for most capital raising in the crypto space—modern-day ports within trade networks, not unlike those used by merchants a thousand years ago.

We believe this experiment is interesting for two reasons.

1. The VC network we operate in functions somewhat like *Fight Club*. While no one fights (yet), we rarely talk about it either.

This VC network includes around 80 funds. Across the entire crypto VC landscape, approximately 240 funds have deployed over $500K at the seed stage. This means we directly engage with one-third of them, and nearly two-thirds read our content. This level of influence was unexpected but real.

However, tracking exactly where funds deploy capital is typically difficult. Sending founder updates to every fund becomes noise.

This tracker emerged as a filtering mechanism, helping us understand which funds have deployed capital, in what areas, and alongside whom.

2. For founders, knowing where capital is being deployed is just the first step. More valuable is understanding fund performance and their typical co-investment partners.

To do so, we calculated a fund’s historical probability of its portfolio companies receiving follow-on funding, although this becomes murkier at later stages (like Series B), when companies often issue tokens instead of raising traditional equity.

Helping founders identify active investors in crypto VC is step one. Next is identifying which capital sources perform better. Once we have this data, we can explore which co-investment groups yield the best outcomes.

Of course, this isn’t rocket science.

No one can guarantee that writing a check leads to a Series A round. Just as no one can guarantee marriage after a first date. But understanding what lies ahead certainly helps—whether dating or fundraising.

Building the Architecture of Success

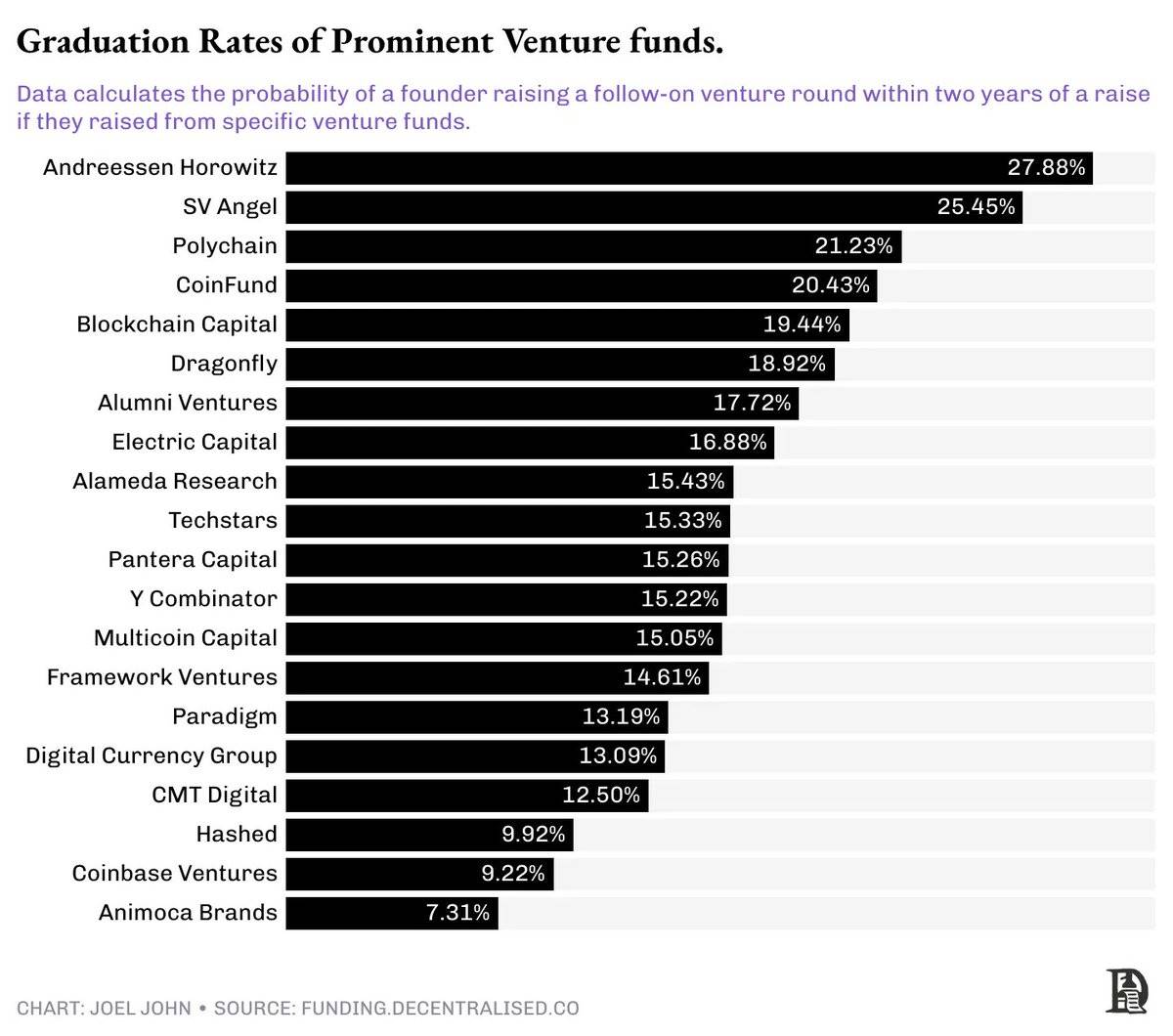

We applied basic logic to identify funds whose portfolios see the most follow-on rounds. If a fund sees multiple companies successfully raise after seed stage, it’s likely doing something right. When startups raise subsequent rounds at higher valuations, a VC’s stake increases in value. Thus, follow-on financing serves as a solid proxy for performance.

We selected the top 20 funds with the most follow-on rounds in their portfolios, then calculated how many total companies they backed at seed stage. This allows us to estimate a founder’s probability of securing follow-on funding. For example, if a fund wrote 100 seed checks and 30 of those companies raised again within two years, we calculate a 30% progression rate.

A caveat: we limited the timeframe to two years. Startups may choose not to raise again, or delay fundraising beyond this window.

Even among the top 20 funds, the power law remains extremely pronounced.

For instance, raising from a16z means a one-in-three chance of raising again within two years. In other words, one out of every three startups funded by a16z goes on to secure a Series A.

That’s a high graduation rate—especially compared to the bottom of this list, where the odds are just 1 in 16.

Near the bottom of this top 20 list, risk funds have only a 7% probability of their portfolio companies raising again. These numbers might seem close, but contextually, a one-in-three chance is like rolling less than three on a die, while 1 in 14 is roughly equivalent to the odds of having twins. These are vastly different outcomes, both literally and probabilistically.

Jokes aside, this highlights the concentration within crypto venture capital. Some VCs can engineer follow-on rounds for their portfolio companies because they also operate growth-stage funds.

Thus, they deploy capital in the same company at both seed and Series A stages. When a VC doubles down by acquiring more shares in a later round, it sends a strong positive signal to future investors.

In other words, the presence of a growth-stage fund within a VC firm significantly impacts a startup’s chances of success over the next few years.

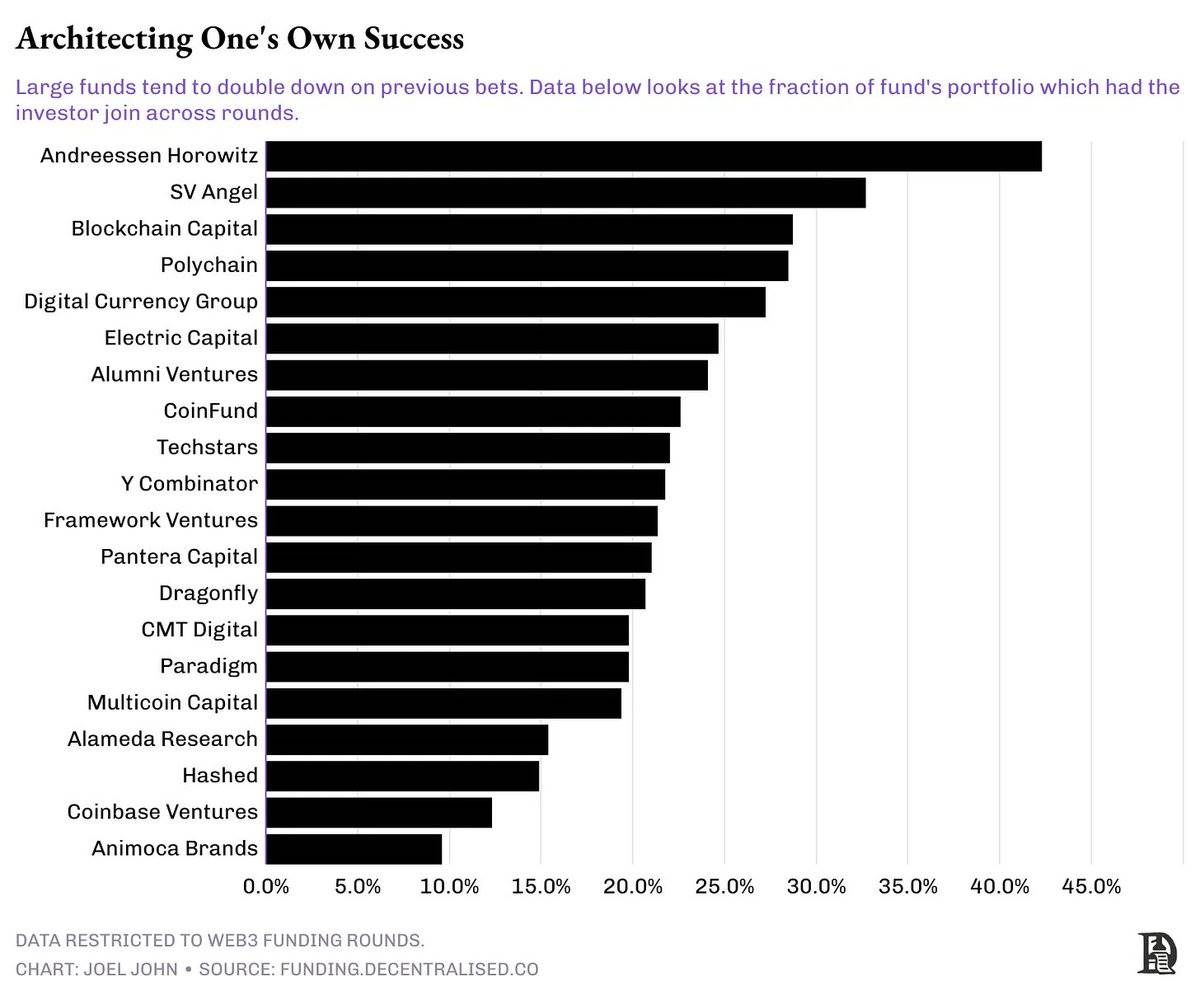

The long-tail effect of this trend is that crypto VCs are evolving into private equity investors for revenue-generating projects. We’ve theorized about this shift before. But what does the data actually show? To investigate, we looked at the number of startups within our investor cohort that secured follow-on funding, then calculated the proportion where the same VC reinvested in the next round.

That is, if a company raised seed capital from a16z, what’s the probability that a16z participates again in the Series A?

A clear pattern emerges. Large funds managing over $1 billion tend to participate heavily in follow-ons. For example, 44% of a16z-backed startups that raised additional capital saw a16z participate in the next round. Blockchain Capital, DCG, and Polychain reinvested in one out of every four follow-on financings.

In other words, who you raise from at seed or pre-seed stage matters far more than you might think—because these investors are much more likely to double down on their own companies.

Habitual Co-Investment

These co-investment patterns are identified in hindsight. We don’t mean to suggest startups failing to raise from top-tier VCs are doomed. All economic activity aims at growth or profit creation. Companies achieving either will naturally see rising valuations over time. Of course, this improves the odds of success. If you can’t raise from this top 20 group, one way to improve your odds is through their networks—or put differently, by connecting with these capital hubs.

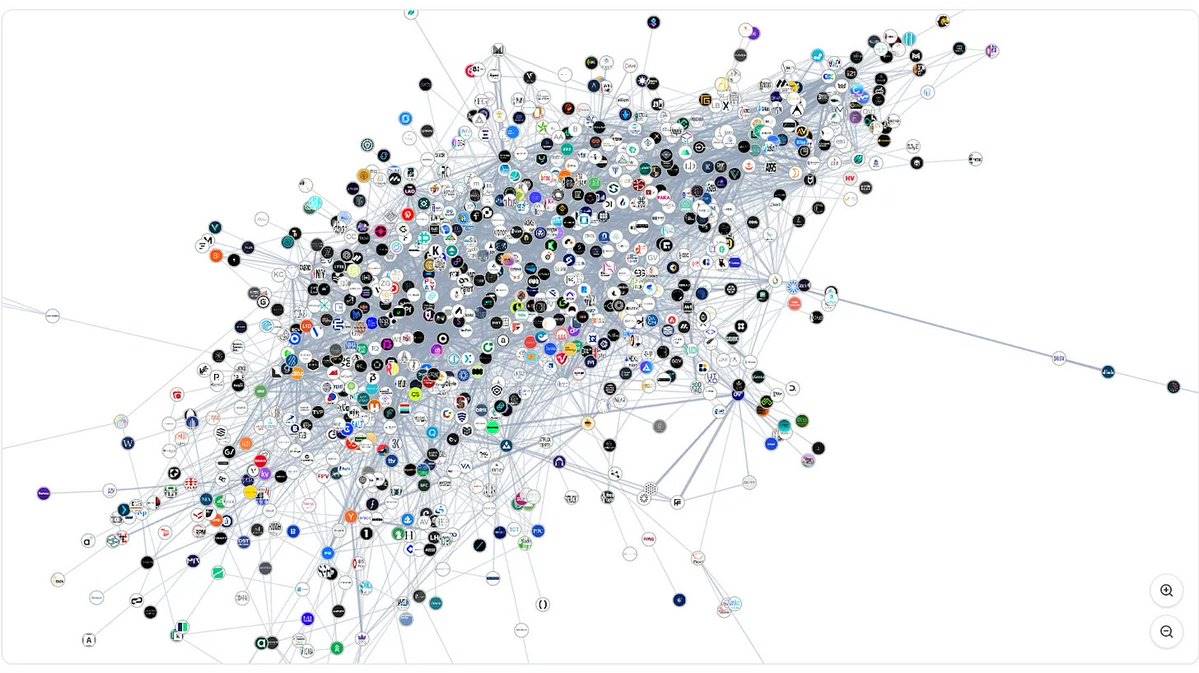

The image below shows the network of all crypto VCs over the past decade. It includes 1,000 investors sharing approximately 22,000 connections. A connection forms whenever two investors co-invest. It may look crowded, even overwhelming. But it also includes defunct funds, those that never returned capital, or ones no longer deploying.

I know—it looks messy.

Yet the reality of market structure becomes clearer in the next visualization. If you’re a founder seeking a Series A, the pool of funds investing over $2M per round is about 50. The network of investors participating in such rounds includes roughly 112 funds. These funds are increasingly centralized, showing stronger preferences for specific co-investment partners.

From seed to Series A, you can raise from many investors. Over time, funds develop co-investment habits. That is, when a fund invests in a company, it often brings along a peer fund—due to complementary skills (like technical support or go-to-market expertise) or established partnerships. To study how these relationships function, we explored co-investment patterns among funds over the past year.

For example, in the last year:

-

Polychain and Nomad Capital co-invested 9 times.

-

Bankless and Robot Ventures co-invested 9 times.

-

Binance and Polychain co-invested 7 times.

-

Binance and HackVC also co-invested 7 times.

-

Similarly, OKX and Animoca co-invested 7 times.

Large funds are becoming increasingly selective about co-investment partners.

For instance, Robot Ventures participated in 3 of Paradigm’s 10 investments last year. Dragonfly shared 3 of its 13 total investments with both Robot Ventures and Founders Fund.

Likewise, Founders Fund co-invested with Dragonfly in 3 of its 9 deals.

In short, we’re moving toward an era where a few funds make large bets with fewer co-investors. And many of these co-investors are well-established names that have been around for years.

Entering the Capital Matrix

Another way to analyze the data is by studying the behavior of the most active investors. The matrix above examines the funds with the highest number of investments since 2020 and their interrelationships. You’ll notice accelerators (like Y Combinator or Outlier Ventures) rarely co-invest with exchanges (such as Coinbase Ventures).

On the other hand, exchanges clearly have preferences. For example, OKX Ventures has a high degree of co-investment with Animoca Brands. Coinbase Ventures has co-invested over 30 times with Polychain and another 24 times with Pantera.

We observe three structural phenomena:

-

Despite high investment frequency, accelerators tend to co-invest less with exchanges or large funds. This may stem from stage-specific focus.

-

Major exchanges prefer growth-stage VCs. Currently, Pantera and Polychain dominate this space.

-

Exchanges favor local players. OKX Ventures and Coinbase show distinct co-investment partner preferences, highlighting the global nature of capital allocation in Web3.

So, if VCs are consolidating, where will the next marginal capital come from? I noticed an interesting pattern: corporate capital forms its own clusters. For example, Goldman Sachs co-invested twice during its lifecycle with PayPal Ventures and Kraken. Coinbase Ventures co-invested 37 times with Polychain, 32 with Pantera, and 24 with Electric Capital.

Unlike traditional venture capital, corporate capital pools typically target growth-stage companies with strong product-market fit (PMF). How this capital behaves during periods of declining early-stage fundraising remains to be seen.

Evolving Networks

From "The Square and the Tower"

After reading Niall Ferguson’s *The Square and the Tower* a few years ago, I became interested in studying relationship networks within crypto. The book reveals how ideas, products, and even diseases spread through networks. Only weeks ago, after building our funding dashboard, did I realize it was possible to visualize the network of capital sources in crypto.

I believe these datasets—and the nature of economic interactions between entities—can be used to design (and execute) M&A and token acquisitions for private companies. These are directions we’re exploring internally. They can also inform business development and partnership initiatives. We’re still figuring out how to grant specific companies access to these datasets.

Back to the question: Do networks actually help funds perform better?

The answer is nuanced. A fund’s ability to pick strong teams and deploy capital at scale matters more than its connections to other funds. What truly counts are personal relationships between general partners (GPs) and co-investors. Venture capital firms don’t share deal flow with brands—they share it with people. When a partner switches funds, their connections move with them.

I had intuitions about this, but limited means to verify it. Fortunately, a 2024 paper studied the performance of the top 100 venture capital firms over time. It analyzed 38,000 funding rounds across 11,084 companies and even accounted for seasonal market shifts. Their findings boil down to a few key points:

-

Past co-investments don’t guarantee future collaboration. If prior investments failed, funds may avoid working together again.

-

Co-investment tends to increase during hype cycles, as funds rush to deploy capital aggressively. During such periods, VCs rely more on social signals and less on due diligence. In bear markets, with lower valuations, funds deploy cautiously and often act alone.

-

Funds select peers based on complementary skills. Therefore, crowded rounds with overlapping investor expertise often lead to trouble.

As I said earlier, co-investment doesn’t happen at the fund level—it happens at the partner level. In my own career, I’ve seen individuals move between organizations. The goal is usually to keep working with the same person, regardless of which fund they join. In an age where AI may replace human labor, remembering that personal relationships remain foundational to early-stage venture capital is helpful.

There’s much more work to be done in studying how crypto VC networks form. For example, I’d like to examine liquidity hedge funds’ capital allocation preferences, how late-stage crypto deployment evolves with market seasonality, or how M&A and private equity play a role. The answers lie within the data we already have—but it takes time to ask the right questions.

Like many things in life, this will be an ongoing inquiry, and we’ll make sure to surface signals as we find them.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News