How does PolyFlow help PayFi applications go live?

TechFlow Selected TechFlow Selected

How does PolyFlow help PayFi applications go live?

As infrastructure, PolyFlow has long sown the seeds of PayFi, quietly awaiting blossoming—its future holds great promise.

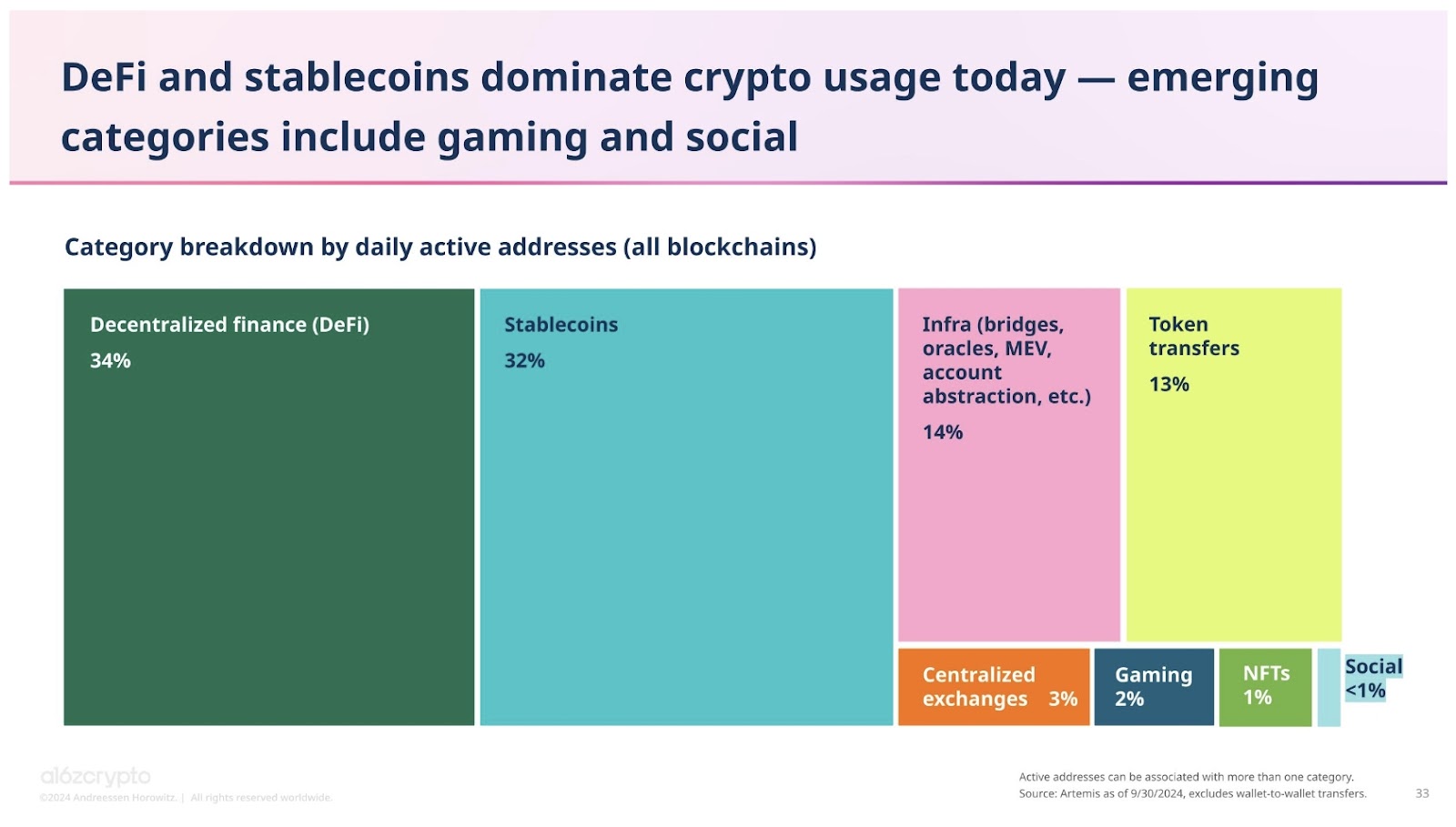

A recent State of Crypto Report 2024 released by a16z Crypto has clearly stated that stablecoins have become one of the most prominent "killer applications" in the Web3 space. Thanks to the widespread adoption of smartphones and the real-world implementation of blockchain technology, stablecoins could become the greatest financial empowerment movement in human history.

Stablecoins have simplified value transfer—their quarterly transaction volume is already more than twice that of Visa's $3.9 trillion—and they settle trillions of dollars in assets annually, demonstrating their immense practical utility. Furthermore, measured by daily active addresses, stablecoins account for nearly one-third of daily cryptocurrency usage at 32%, second only to decentralized finance (DeFi) at 34%.

(State of Crypto Report 2024: New data on swing states, stablecoins, AI, builder energy, and more)

Recently emerged PayFi represents an innovative application integrating Web3 payments with decentralized finance (DeFi).

PolyFlow, as the infrastructure behind PayFi, is harnessing the transformative power brought by digital currencies and blockchain technology to build a new PayFi crypto payment network. It accelerates the deployment of PayFi applications, drives paradigm shifts toward innovative finance, unlocks the true value of Web3.0, and ultimately turns the grand vision laid out in the Bitcoin whitepaper into reality.

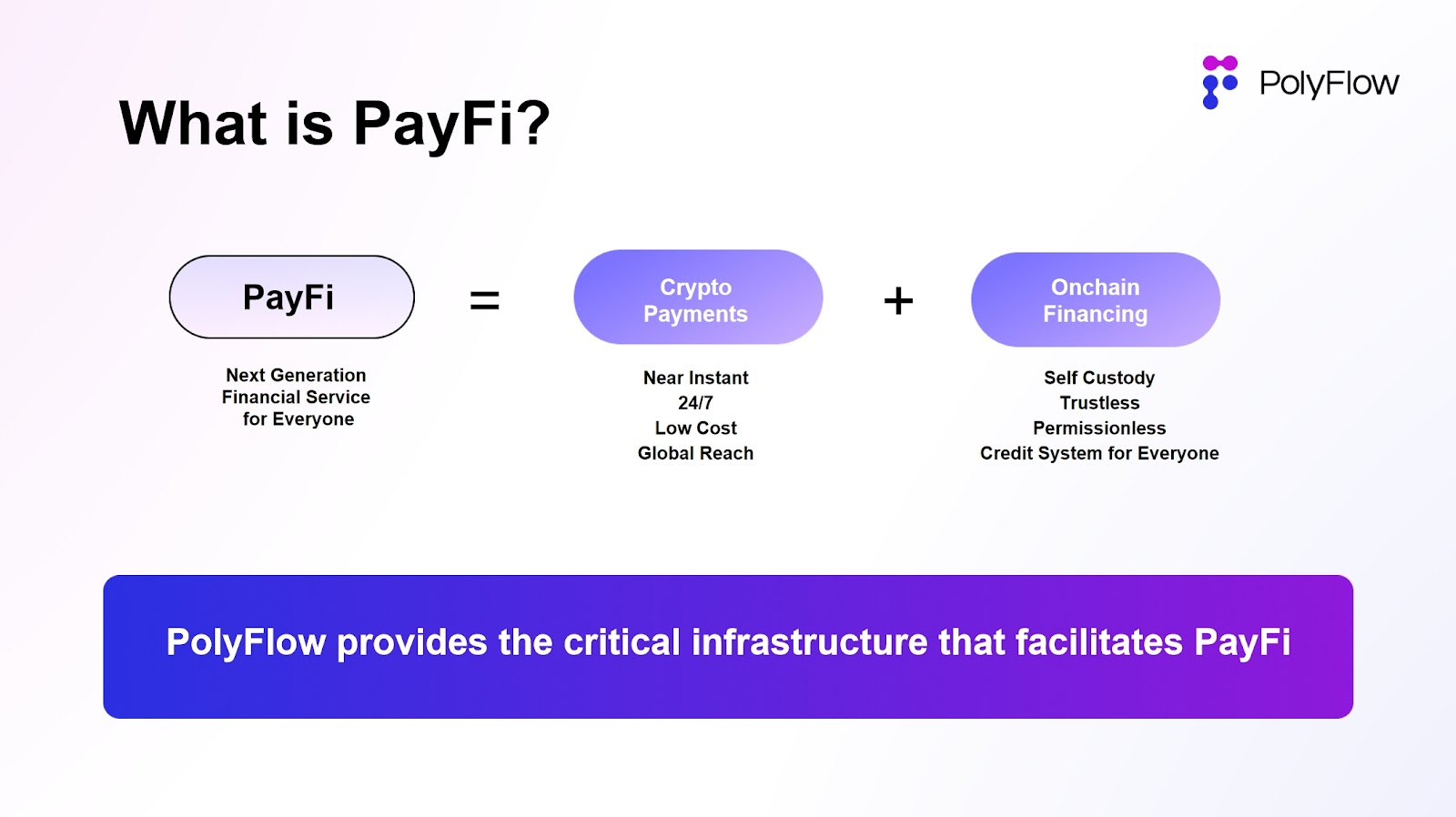

1. What Is PayFi?

PayFi, short for Payment Finance, refers to an innovative application model based on blockchain and smart contract technologies that integrates payment functions with financial services. At its core, PayFi leverages blockchain as a settlement layer, combining the strengths of Web3 payments and decentralized finance (DeFi) to enable efficient and frictionless value movement.

The goal of PayFi is to realize the vision outlined in the Bitcoin whitepaper—building a peer-to-peer electronic cash system without trusted third parties—while fully leveraging the advantages of DeFi to create a new financial market. This includes offering novel financial experiences, developing complex financial products and use cases, and ultimately forming an entirely new value chain.

PayFi was first introduced as a new narrative by Lily Liu, President of the Solana Foundation, during the Hong Kong Web3 Festival in 2024. In her view, PayFi builds a new financial market around the time value of money (TVM)—something difficult or impossible to achieve in traditional finance.

This emerging PayFi financial market not only improves upon traditional finance in terms of Web3 payment efficiency—enabling instant settlements, lower costs, transparency, and global reach—but also leverages DeFi to ensure decentralization, permissionless access, asset ownership, and personal sovereignty across a global network.

(https://x.com/Polyflow_PayFi)

2. PolyFlow — The PayFi Infrastructure

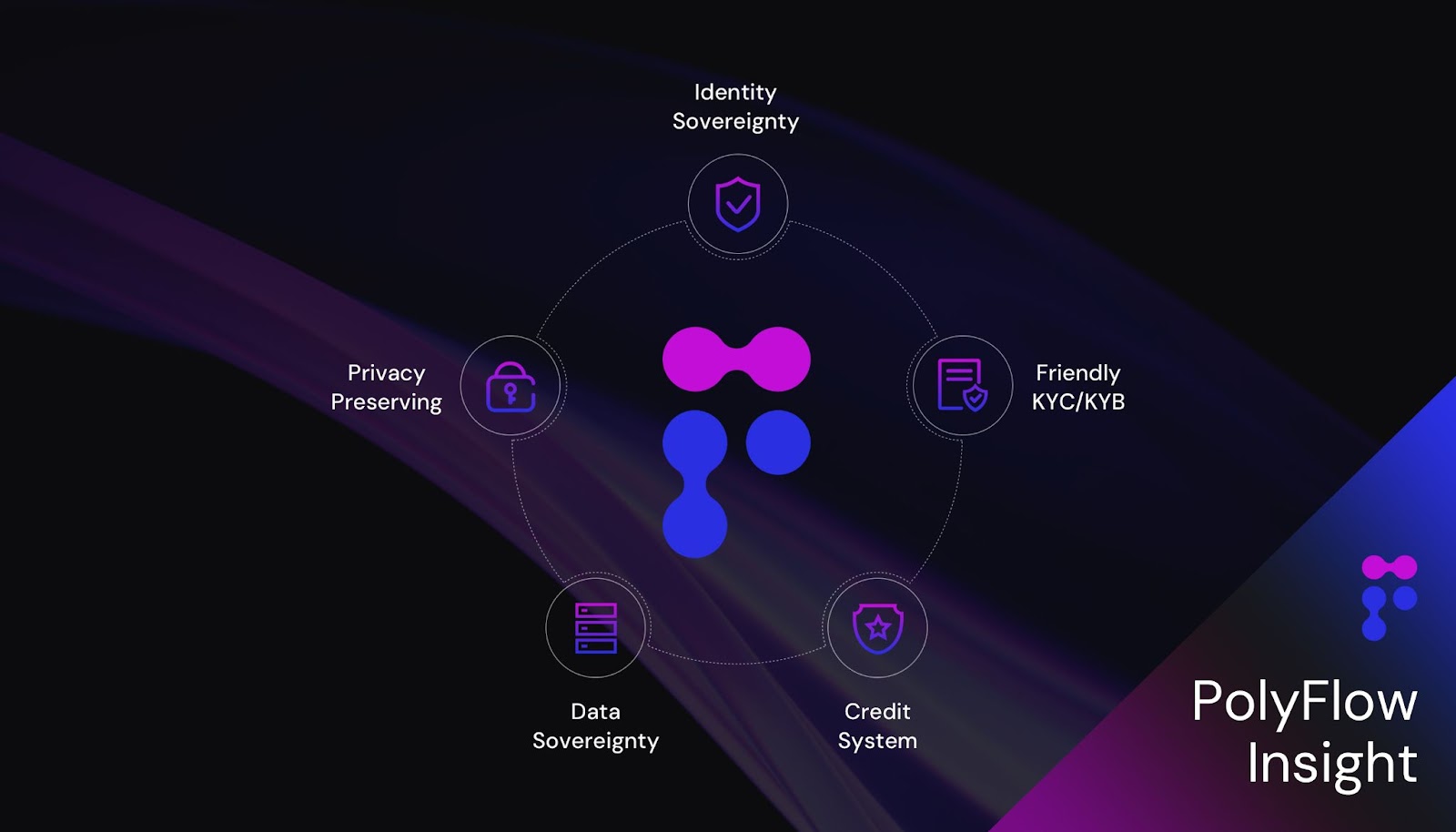

The original mission of PolyFlow is to build a decentralized infrastructure that enables more PayFi applications to launch, participate in the construction of a global payment network, reduce regulatory compliance burdens, eliminate custodial risks, and minimize reliance on intermediaries.

PolyFlow’s core philosophy is to use modular design to effectively separate transaction information flows from capital flows—previously controlled by centralized institutions—using decentralized methods. This approach ensures better compliance with regulations, eliminates custody risks, and leverages blockchain features to connect with the DeFi ecosystem, enabling large-scale adoption of PayFi applications.

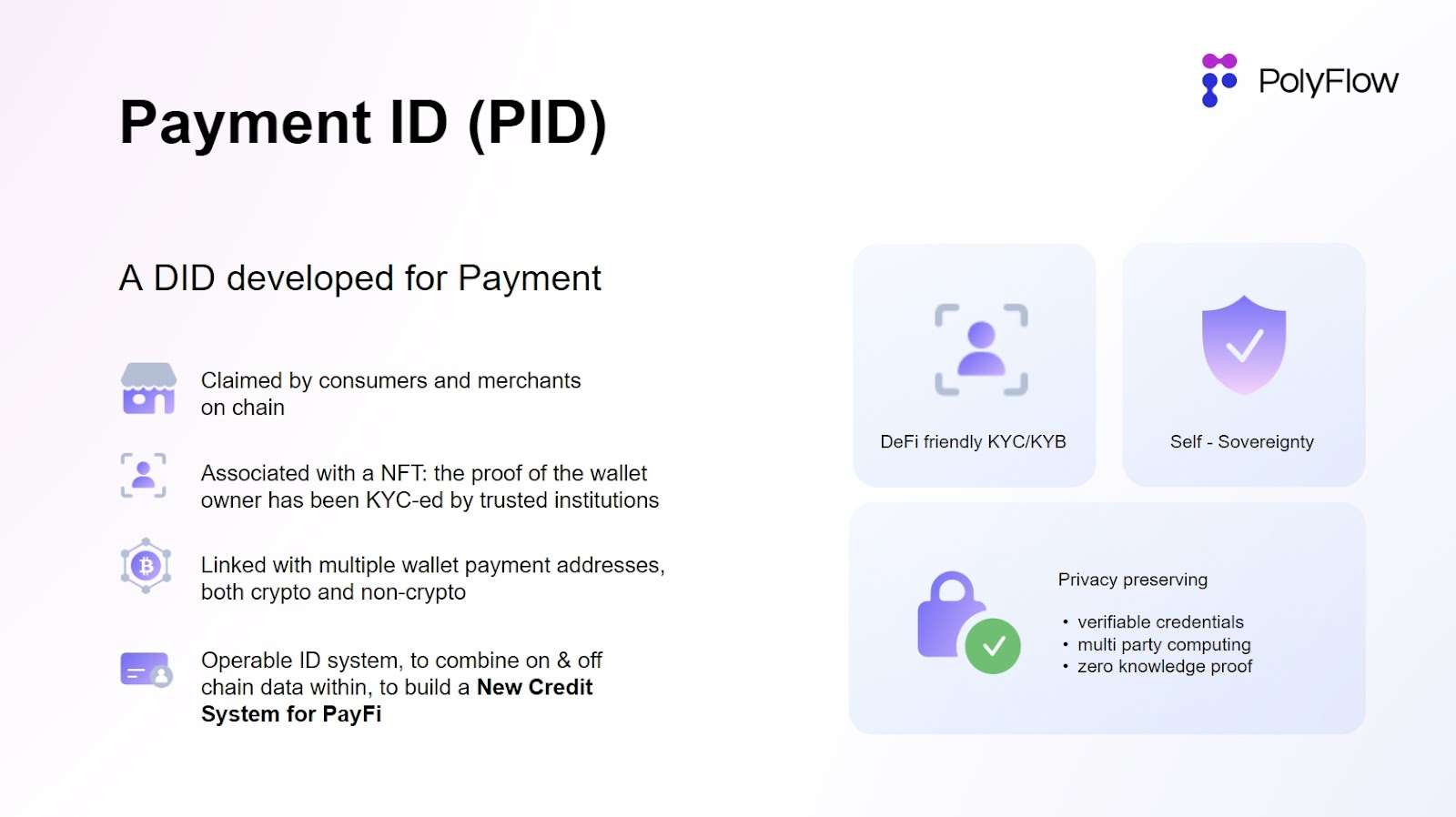

To this end, PolyFlow has introduced two key components: Payment ID (PID) and Payment Liquidity Pool (PLP):

-

PID is linked to the information flow and serves as a powerful tool enabling user identity verification and compliant onboarding, privacy protection and data sovereignty, AI-driven data processing, and X-to-earn functionalities;

-

PLP is tied to the capital flow and managed by smart contracts for payment transactions. It provides a secure and compliant framework for digital asset transfers, custody, and issuance while introducing composability and scalability from the DeFi ecosystem.

Together, these components allow PolyFlow to establish a lightweight, regulation-friendly, non-custodial, and DeFi-compatible architecture for PayFi applications, along with a secure and compliant framework for digital asset transfer, custody, and issuance.

(https://x.com/Polyflow_PayFi)

It's important to understand that the Bitcoin system and blockchain network created by Satoshi Nakamoto represent a new solution in the digital age to long-standing financial and monetary challenges—not just how to move value across time and space, but also how to eliminate reliance on third-party trust in transactions. These are precisely the goals that PolyFlow aims to achieve.

3. How PolyFlow Enables PayFi Applications

Current Web3 payments remain in an early, foundational stage, primarily using cryptocurrencies as transactional media in scenarios like cross-border remittances, OTC trading, and payment cards. These centralized approaches struggle to integrate with the DeFi ecosystem and are limited in scope.

To fully merge Web3 payments with decentralized finance (DeFi) and build innovative PayFi applications, we need a new infrastructure—PolyFlow—and its core modules: Payment ID (PID) and Payment Liquidity Pool (PLP).

PayFi applications can freely choose their preferred blockchain settlement layer (Transaction Settlement Layer) and currency layer (Currency Layer) based on specific use cases. For example, they might select the high-performance Solana blockchain to support use cases involving PayPal's PYUSD stablecoin ecosystem.

Beyond this, PayFi must address the most critical aspects of the tech stack: asset custody and compliant onboarding.

3.1 Asset Custody

Asset custody is crucial in finance, both on-chain and off-chain. For off-chain payment applications, funds typically require licensing and strict compliance measures. For on-chain blockchain-based payment apps, considerations include ensuring smart contract security, private key management, and compatibility with both traditional finance and DeFi systems.

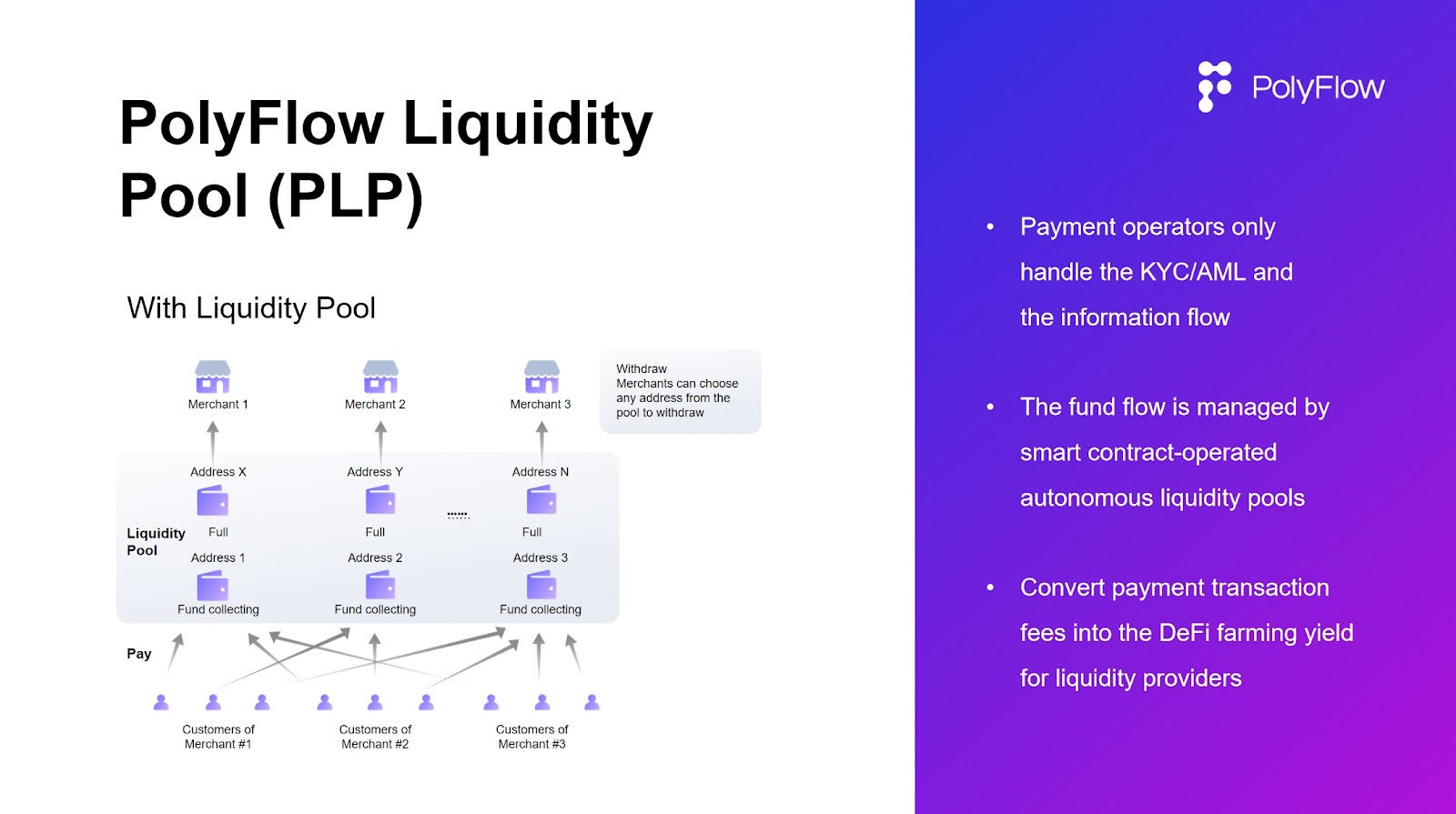

To address this, PolyFlow’s Payment Liquidity Pool (PLP) uses smart contract addresses to receive funds from payment transactions, enabling on-chain custody instead of relying on expensive enterprise wallets operated by centralized entities.

(https://x.com/Polyflow_PayFi)

This more decentralized PLP model enables:

-

Decentralized asset custody: Offers PayFi applications a convenient, secure, and compliant way to manage custody—ensuring fund safety while minimizing dependence on transaction intermediaries.

-

Liquidity pools: By aggregating transaction funds through smart contract addresses, PLPs can provide liquidity to meet financing needs within payment transactions.

-

DeFi compatibility: Centralized applications cannot seamlessly interact with decentralized DeFi ecosystems. Being built on blockchain, PLPs can natively integrate with DeFi and bring DeFi business logic directly into PayFi applications.

-

Risk-free RWA yield category: Yields generated by the protocol are directly reflected in the PLP. This revenue stream, derived from real-world payment transaction scenarios, offers DeFi a stable and low-risk source of returns.

This flexible PLP architecture allows seamless integration with the broader DeFi ecosystem, ensuring PayFi applications can adapt to the evolving digital asset landscape.

3.2 Compliant Onboarding

It's widely recognized that compliant user onboarding is essential for the healthy development of financial payment ecosystems and services. The fundamental requirement here is ensuring all transactions and fund movements comply with KYC/AML/CTF standards and local jurisdictional regulations.

To solve this, PolyFlow introduces Payment ID (PID), a decentralized identifier (DID) that binds encrypted, privacy-preserving KYC/KYB attestation data. It links verifiable credentials across multiple platforms and enables:

-

Compliant onboarding: PID can aggregate verified information from multiple platforms, helping partners streamline the verification process.

-

Privacy protection: Using zero-knowledge proofs and other advanced techniques, PID allows fulfillment of anti-money laundering and counter-terrorism financing (AML/CTF) obligations without exposing user privacy. This is a prerequisite for users to engage with traditional finance or DeFi ecosystems.

-

Data sovereignty: PID enables reporting transaction data to regulators to meet compliance requirements, while simultaneously returning behavioral data on the chain back to users themselves.

-

AI-driven insights: Beyond KYC/KYB data, PID can also link off-chain uploaded or on-chain collected transaction data. AI can analyze rich everyday transaction patterns to extract additional value for PID holders—an essential function in building a robust on-chain credit system.

The innovative introduction of PID brings transformative advantages to the industry: bridging traditional finance and DeFi ecosystems, and giving users a flexible and reliable way to manage digital identities, conduct cross-platform transactions, and build on-chain credit.

(https://x.com/Polyflow_PayFi)

4. Real-World PayFi Applications Enabled by PolyFlow

With a general-purpose blockchain settlement and currency layer, combined with PolyFlow’s asset custody and compliant onboarding modules, PayFi applications can be deployed in real-world settings and achieve interoperability with decentralized finance (DeFi).

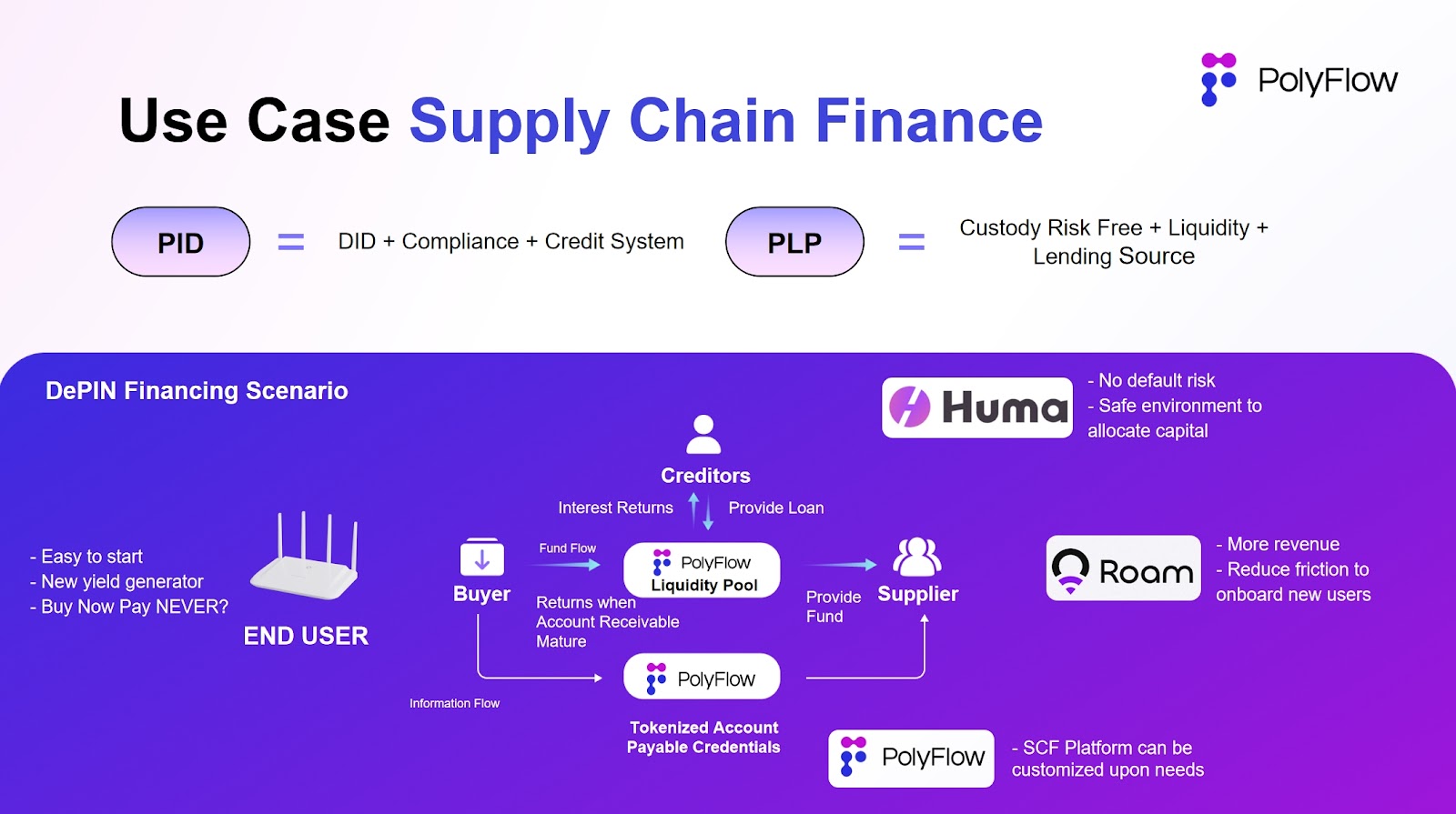

Recently, DePIN project Roam partnered with RWA platform Huma Finance to launch a DePIN hardware loan program, helping Roam rapidly deploy its core hardware infrastructure and accelerate the growth of a global decentralized Wi-Fi network.

PolyFlow provided critical underlying support for constructing this PayFi use case for DePIN hardware loans.

(https://x.com/Polyflow_PayFi)

PID establishes the credit foundation for loans, extending the overall network credit of Roam to individual miner users (End Users), enabling microloans for single or multiple miners. PLP acts as the carrier for loan funds, providing secure and compliant custody, eliminating intermediaries, and allowing all parties to rely on Solana’s consensus ledger rather than establishing strong mutual trust manually.

Users can stake future cashflows generated by Roam Growth products and use Roam Tokens or NFTs as collateral to quickly obtain loans for purchasing Roam Wi-Fi hardware, participate in building the global decentralized Wi-Fi network, and earn RoamPoints rewards.

Through this innovative “Buy Now Pay Never” PayFi model built on PolyFlow, a new financial application scenario (micro-lending) has been established for the DePIN industry, significantly accelerating DePIN network development and pushing the sector into its next phase of growth.

In addition, PolyFlow is actively collaborating with various traditional financial institutions, Web3 projects, and other partners to explore further PayFi application scenarios such as cross-border trade, payment cards, payment gateways, wallet settlement networks, supply chain finance, and DePIN.

5. The Future of PayFi Is Bright

The rapid rise of stablecoins over the past five years shows they now operate as a parallel monetary system alongside traditional financial infrastructure. We are also witnessing stablecoins increasingly being adopted beyond trading, entering everyday life.

The emergence of PayFi will further expand stablecoin use cases, promote financial inclusion globally, and drive crypto toward true mass adoption.

As an infrastructure provider, PolyFlow has already sown the seeds of PayFi—now it waits for the flowers to bloom. The future is full of promise.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News