The De-tradabilization of Cryptocurrencies Composes a Tune for Exploring Web3's Way Forward

TechFlow Selected TechFlow Selected

The De-tradabilization of Cryptocurrencies Composes a Tune for Exploring Web3's Way Forward

In the long term, the entire Web3 industry's shift toward off-chain and real-world consumption scenarios is already a settled trend.

By: Zuo Ye

De-Commoditizing Cryptocurrencies: Composing a Path Forward for Web3

Compared to Ethereum's fragmented ecosystem, Solana’s is smaller but more agile. After the FTX collapse, Solana staged a phoenix-like comeback through high performance, strong marketing, and various hardware products—successfully achieving a second wave of popularity.

To be specific, "high performance" refers to the Firedancer upgrade, "strong marketing" to the meme season, and "hardware" to various Web3 phones. Yet these efforts alone aren’t enough. PayFi, proposed by Lily Liu, Chairwoman of the Solana Foundation, has also become a hot topic. Although discussing a trend from July in October might seem outdated, in the long run, the entire Web3 industry shifting off-chain and into real-world consumption scenarios is now inevitable.

"Long, long ago, you had me, and I had you."

This article isn't a ballad for Solana—it’s a composition charting a path forward for Web3.

The Unfulfilled Promise of Crypto Wallets: The Prelude to PayFi

Before presenting Lily Liu’s definition of PayFi, let’s first discuss Web3 wallets. From 2022 to 2023, as smart contract wallets, account abstraction (AA), and exchanges grappled with traffic anxiety, a new wave of Web3 wallets reached their second peak since the 2017–2021 “shitcoin” era.

From an exchange’s perspective, wallets are the primary gateway for users to interact with blockchains, serving as conduits for incoming and outgoing traffic—and potentially even replacing CEXs. Furthermore, amid intensifying competition among Ethereum L2s, multi-chain wallets are clearly becoming central hubs for aggregating liquidity.

Yet the wallet ecosystem in 2024 hasn’t been particularly impressive. OKX’s built-in Web3 wallet stands out as a leader, but most wallets still haven’t evolved into standalone products. A key reason is that Web3 wallets have traffic but lack transaction closure mechanisms—they can’t solve the profitability problem. If they charge fees, users simply open desktop apps instead, happily saving on transaction costs.

From a more “path-dependent” standpoint, the core issue with crypto wallets lies in their overemphasis on trading functionality. Note that this doesn’t contradict the revenue challenge mentioned earlier. The defining feature of crypto wallets is enabling richer on-chain trading experiences—from supporting more chains to dApp recommendation systems with competitive ranking algorithms.

Unlike Alipay, users don’t keep their money in crypto wallets. Non-custodial models offer peace of mind, but fail to win users’ loyalty. In short, crypto wallets bear no resemblance to Web2 wallets—they neither manage money nor offer financial services.

All these factors prevent crypto wallets from building closed-loop payment systems like PayPal, WeChat Pay, or Alipay. In broader commercial terms, Web3 wallets serve only users, not merchants. Even if dApps count as merchants, they represent only a tiny fraction of on-chain businesses.

Wallets do generate significant traffic, and DeFi gains or losses on-chain could indeed translate into off-chain spending power—though losses are equally possible, depending on whether one measures value in ETH, stablecoins, or fiat.

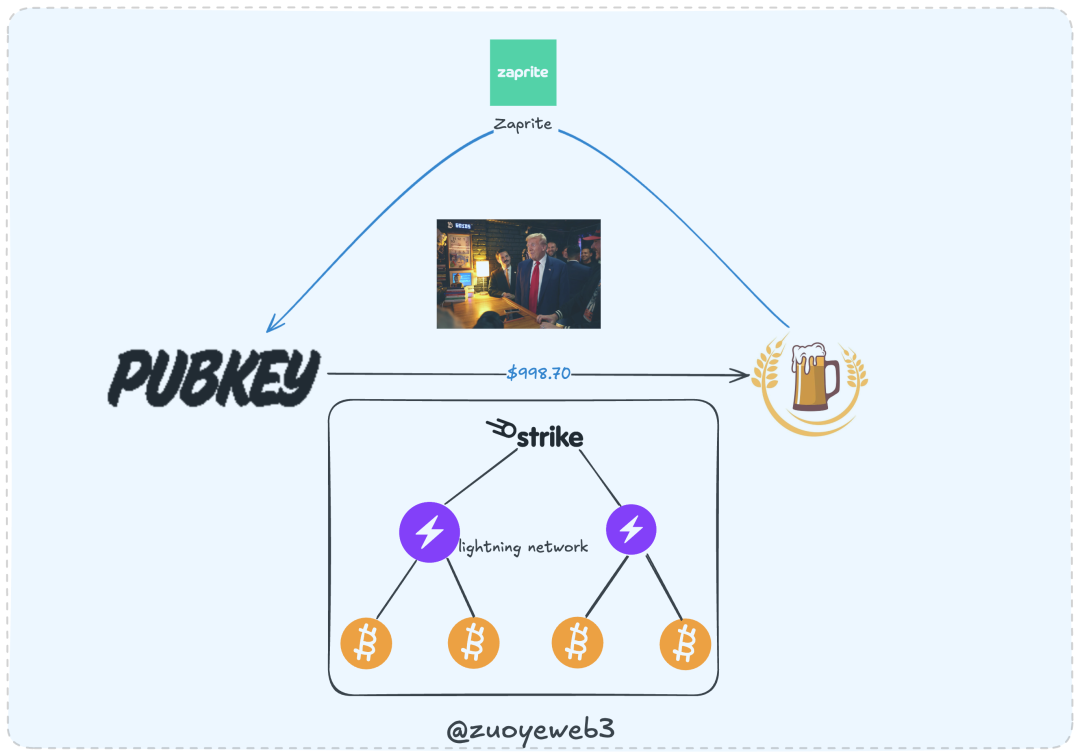

A proper payment system requires support on both merchant and user sides—an area where the current industry falls short. Consider our top-tier male entrepreneur, President Trump: On September 19, 2024, he visited PubKey bar in New York and bought a $998 beer to celebrate his supporters, paying via Strike while the merchant received funds via Zaprite.

In this case, the payer and payee used different payment systems—a scenario unimaginable in Web2, akin to paying with Alipay while the merchant receives via WeChat. But in Web3, it makes sense because both parties use Bitcoin’s network as the settlement layer. Here's how it works:

-

Trump initiates payment via Strike, which triggers the Lightning Network; after confirmation on the Bitcoin network, the transaction proceeds;

-

PubKey uses Zaprite to receive funds, which confirms the payment status via the Lightning Network. Once confirmed on the Bitcoin network, the transaction concludes.

Zaprite charges only a $25 subscription fee. Beyond that, merchants pay only miner fees—the rest is pure profit. Compare this to Visa/MasterCard/AE, which charge around 1.95%-2% in fees. Meanwhile, Bitcoin miner fees average about $1.46 recently, and receiving Bitcoin incurs zero fees.

Looking ahead, Web2 payments function similarly to Trump buying beer—but involve many intermediaries, a flaw inherent to Web2. Opportunities for Web3 payments and PayFi lie precisely within this gap.

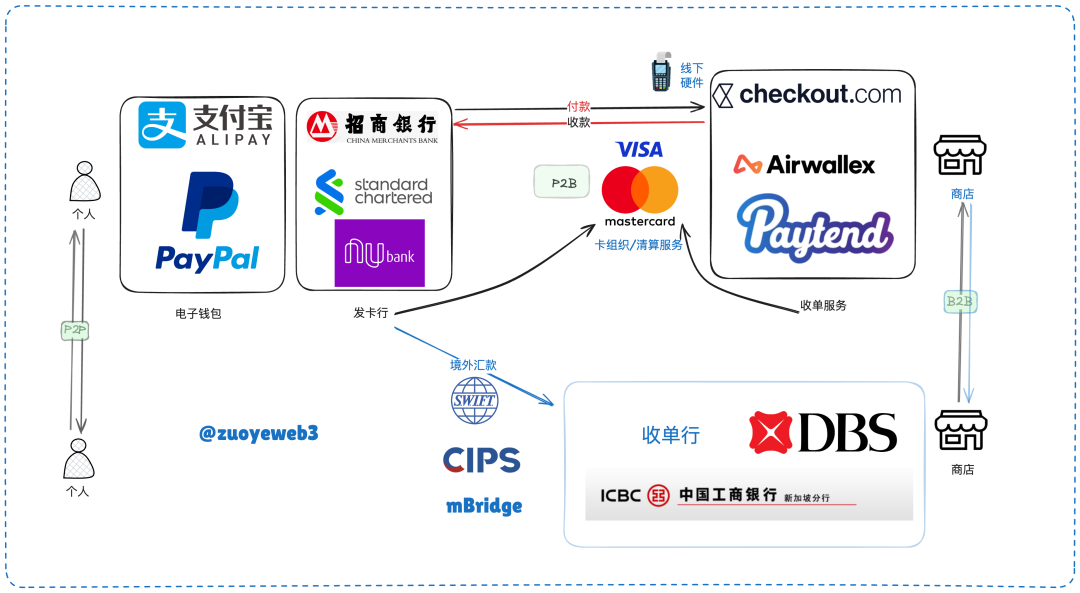

Let’s map the concepts: Products like Alipay, WeChat Pay, and PayPal are electronic wallets targeting consumers (C-end). Correspondingly, businesses (B-end) rely on merchant acquiring systems. By building a fund-clearing network similar to the Lightning Network, we can establish a basic P2B (person-to-business) interaction system. Typically, such clearing networks require card networks and payment protocols working together.

Taking the above diagram as an example, Web2 payment systems include P2P (peer-to-peer), P2B/B2B (person-to-business/business-to-business), and inter-merchant transactions. Banks also settle via systems like SWIFT or CIPS, or cross-border CBDC platforms like mBridge.

Note, however, that strictly speaking, payments occur between individuals and businesses or between businesses themselves. We include P2P and interbank transactions here mainly to facilitate comparison with Web3, where the dominant payment use case is actually peer-to-peer—Bitcoin being a classic example of a peer-to-peer electronic cash system.

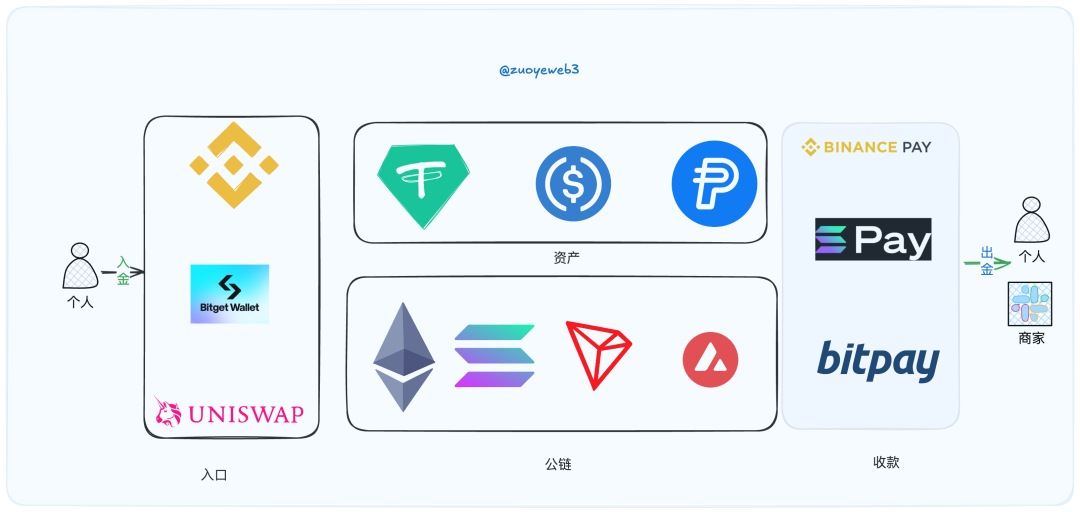

If we model Web3 payments after Web2, the system appears surprisingly simple. But theoretical simplicity masks ecological fragmentation. A key difference: traditional systems have many banks but few card networks, creating powerful network effects. Web3 does the opposite—numerous blockchains/L2s coexist, yet the main assets are limited to USD-pegged stablecoins like USDT and USDC.

Even under optimistic estimates, globally there are only around 30,000 merchants accepting Bitcoin. While some major brands like Starbucks participate in certain regions, adoption remains far behind traditional card networks or e-wallets.

Merchants accepting Binance Pay or Solana Pay are mostly online—platforms like travel OTA provider Travala. Scaling up to the billion-user scale of card networks remains a distant dream.

We’ll elaborate further on payment systems later. Now, it’s time to introduce the concept of PayFi.

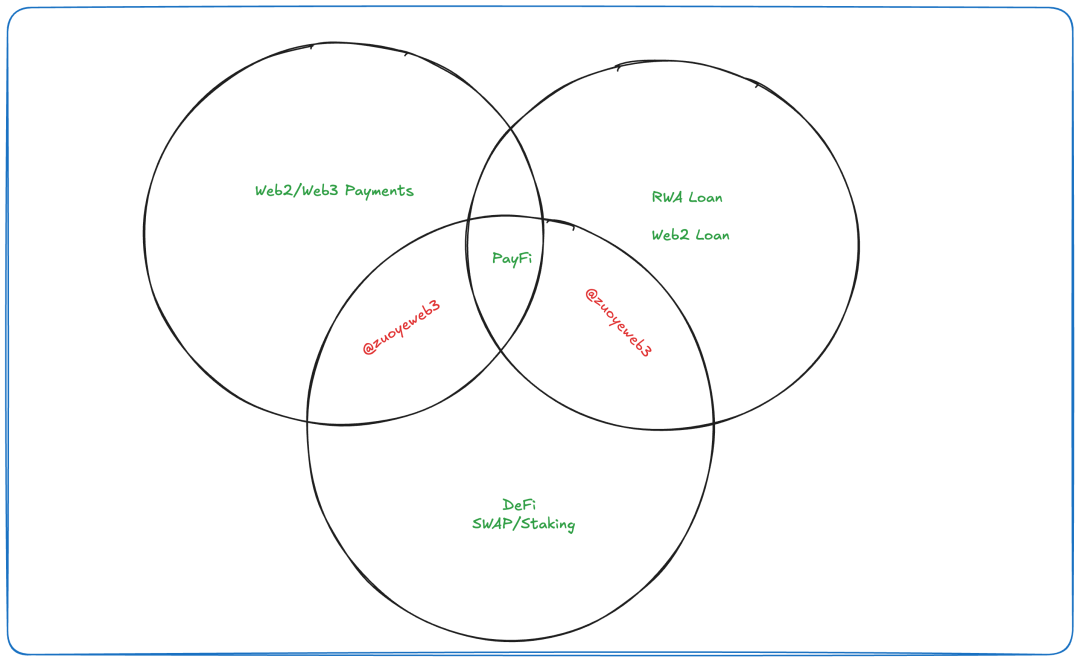

The PayFi Stack: The Intersection of DeFi, RWA, and Payments

The narrative structure—discussing Payments before introducing PayFi—is intentional, as the two differ significantly. Broadly speaking, PayFi resembles DeFi + stablecoins + payment systems, bearing little resemblance to Web2 Payments, as readers may already sense.

Here’s Lily Liu’s explanation: PayFi leverages the time value of money (TVM). For instance, earning yield from DeFi investments embodies TVM. However, this often requires time—such as staking tokens with lock-up periods. As long as tokens exist, they carry appreciation potential. Traditionally, users reinvest earnings back into DeFi, cycling endlessly to maximize returns.

Now, those yields can be redirected elsewhere—for example, using expected future income to enable present-day spending. Consider this:

-

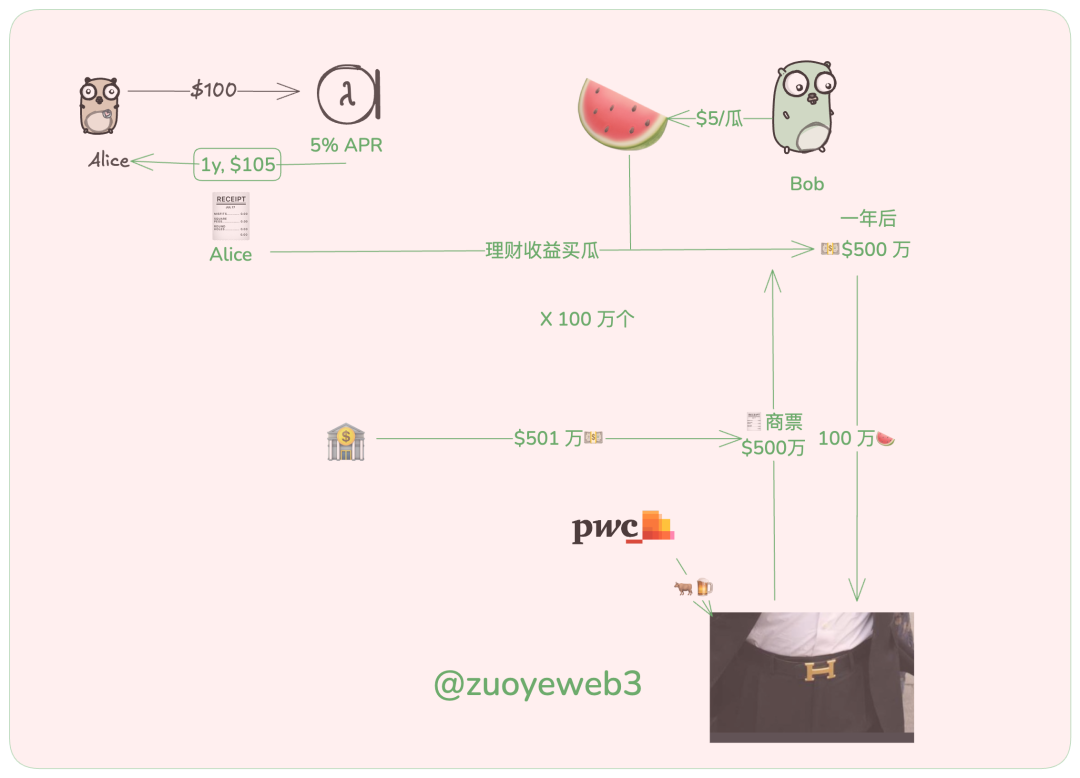

Alice invests 100 USDC in a product with a 5% annual percentage rate (APR), yielding $105 after one year;

-

Bob runs a watermelon stand. To boost sales, he allows Alice to eat $5 worth of melon now, promising to redeem the $5 interest at maturity using her investment proof.

This example is overly simplistic and barely holds up under scrutiny—how do Alice and Bob ensure contract execution? What if Alice’s returns fall short? But setting aside such concerns, Alice enjoys melon at no cost, while Bob gains a $5 accounts receivable.

A year later, a bull market arrives. Bob collects many such $5 claims and decides to expand into supplying large enterprises. He spots Evergrande looking for watermelon suppliers, placing an order worth $5 million. Delighted, Bob accepts a commercial bill (commercial paper) based on prior experience with Alice. They agree Bob will receive cash in a year—or property if payment fails.

After six months, Bob wants to enter the stock market and needs to liquidate the commercial paper. PricewaterhouseCoopers rates it AAA—deeming it a high-quality asset. Banks, non-financial institutions, and even individuals rush to buy, driven by confidence in Evergrande’s real estate quality and its strong appreciation potential.

Bob successfully sells the paper at a premium of $5.01 million. The bank gets the paper, Evergrande gets free funding, Bob captures stock market gains—all seemingly heading toward bright futures. (In reality, commercial paper usually trades at a discount with fees; this illustrates workflow only. Prior to its default, Evergrande’s paper traded at roughly 70–80% of face value.)

Another aspect of TVM involves monetizing non-circulating assets—even treating them as money or equivalents. This shares logic with re-staking. See Triangle Debt or Mild Inflation: An Alternative View on Restaking for details.

In the Web3 context, monetizing non-circulating assets can only happen via DeFi. Thus, PayFi is a natural extension of DeFi—taking part of the on-chain Lego and redirecting liquidity off-chain to improve real-life experiences.

The relationship between PayFi and Payments lies in payments being the simplest and most convenient way to move funds off-chain. PayFi overlaps with RWA too, though traditional RWA emphasizes “onboarding”—like tokenization processes requiring securities, gold, or real estate to be tokenized for on-chain circulation. Many familiar domestic consortium chains focus on exactly this—blockchain invoices or projects like GXChain.

PayFi isn’t necessarily a subset of RWA. Much of PayFi activity is “off-chain,” and whether something goes on-chain isn’t central to the concept—only that interactions with off-chain elements are involved.

Still, there’s no need to overanalyze. Many Web3 concepts lack large-scale products or user bases, revolving more around hype and token sales than substance. Roughly speaking, products involving PayFi / Payments and RWA can be grouped chronologically:

-

Old Era: Ripple, BTC (Lightning Network, BTCFi, WBTC), Stellar

-

2022 RWA Triad: Ondo/Centrifuge/Goldfinch

-

New Era – 2024 PayFi: Huma (founded earlier, resurged in 2024), Arf

Looking at this product evolution timeline, you could reasonably argue PayFi continues where RWA left off. Traditional narratives—especially models involving on-chain capital lending to off-chain entities—are essentially what PayFi means in 2024. Back in 2022, they were called RWA.

You could boldly claim that RWA lending, Ripple-style cross-border settlements, and stablecoin-based off-chain spending collectively define today’s PayFi landscape. At its core, that’s all there really is.

Web3 software and hardware are built upon Web2’s material and ideological foundations—so too is Web3 PayFi. Its similarities with Payments outweigh differences. Lending products are defined more by capital flow direction—if off-chain applications generate higher yields, those returns can feed back into payment activities.

Misunderstanding is the fate of every communicator. Whether Lily Liu agrees with this interpretation, I don’t know. But I believe only by tracing it this way does the logic become coherent. Any model using on-chain yields for off-chain consumption fits the PayFi concept. Hence, the market’s immediate focus will be on Web3 Payments, RWA Loans, and stablecoins—three components often forming a self-reinforcing cycle.

For example: An RWA enterprise loan denominated in U (stablecoin). Individuals provide funds via DeFi protocols into an RWA-linked lending pool. After evaluation, the RWA lending protocol disburses loans to real-world businesses. Upon repayment, liquidity providers earn protocol profits, withdraw via a Mastercard U card, and spend seamlessly at merchants supporting Binance Pay—a perfect closed loop.

History belongs to pioneers, not summarizers. Defining PayFi matters less than urgently exploring real yields beyond DeFi’s on-chain rat race. Demand from billions of people in the real world will bring richer liquidity and higher-leverage valuations to on-chain ecosystems. Whoever cracks the code gets to define the market.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News