Flowers in full bloom, fire fueling oil: A brief analysis of Pendle and airdrop projects' dual growth flywheels

TechFlow Selected TechFlow Selected

Flowers in full bloom, fire fueling oil: A brief analysis of Pendle and airdrop projects' dual growth flywheels

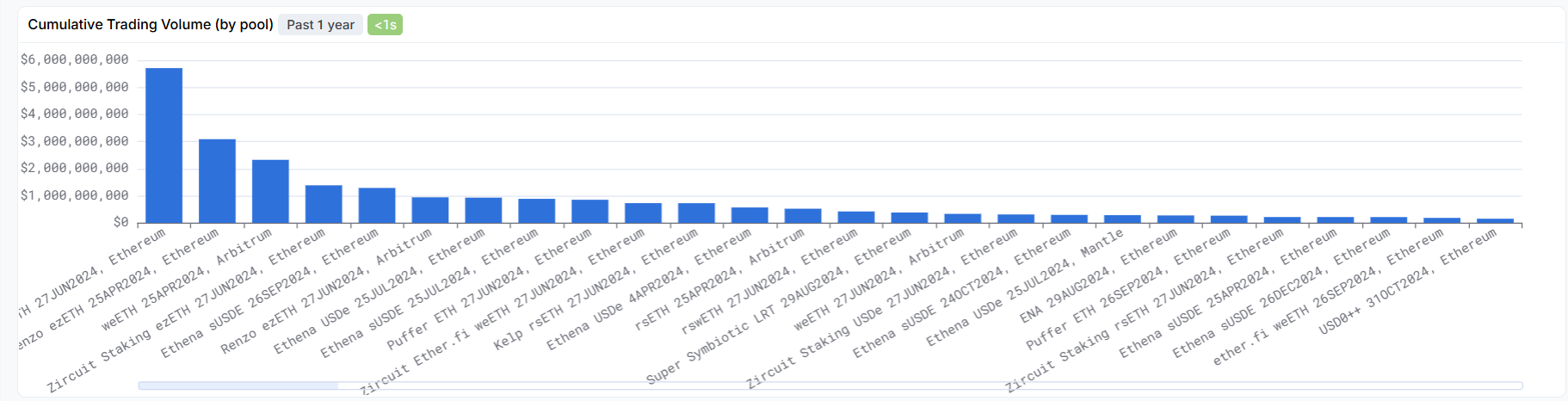

From the trading volume, it is evident that what has supported Pendle's peak TVL of several billion dollars are the ever-emerging ETH staking/re-staking/liquid staking protocols and the flagship project Ethena.

What is Pendle and How Does It Work?

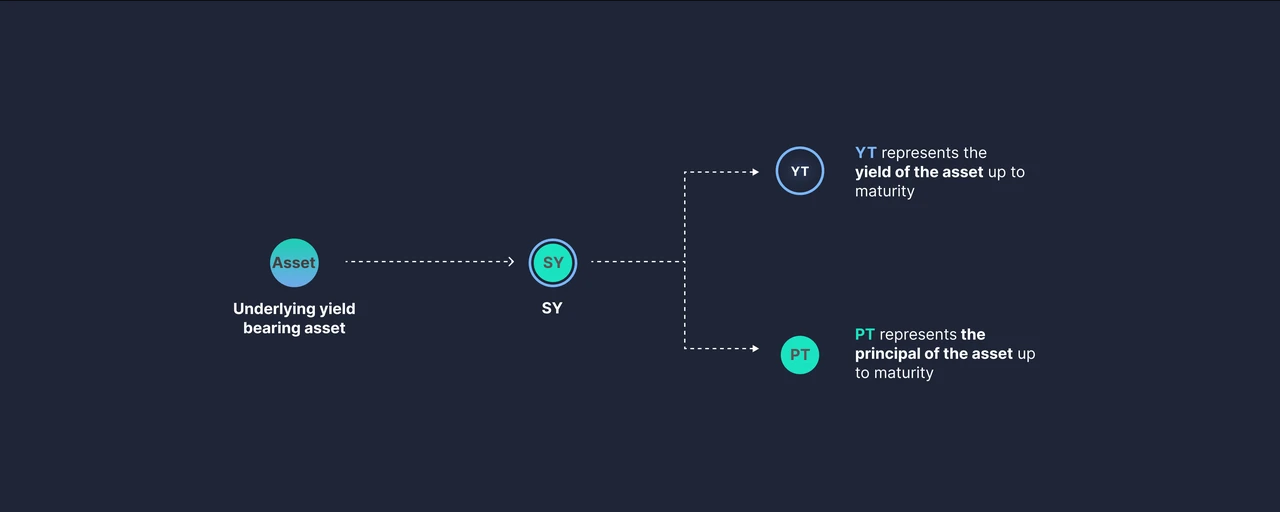

The core idea behind Pendle is to tokenize the future yield of interest-bearing assets, enabling them to be freely traded on secondary markets. Specifically, Pendle splits interest-bearing assets (such as stETH) into:

1. Principal Token (PT): Represents ownership of the underlying asset. PT holders can redeem an equivalent amount of the base asset upon maturity.

2. Yield Token (YT): Represents the expected yield generated over a future period. YT holders can capture these yields upfront.

Illustration of asset separation

Within the Pendle protocol, users can exchange their interest-bearing assets (SY) for a pair of PT + YT, offering several strategic options:

If a user anticipates that annualized yields will decline—for example, in Ethena’s case, where staking ETH and minting USDe currently results in falling native income (from funding rates of short perpetual contracts denominated in crypto)—they can sell their YT to lock in profits early. When the term ends, they may repurchase YT, pair it with their PT, and redeem the original SY asset;

Chart showing USDe yield from Ethena protocol, remaining low (APY < 5%) since May

If a user believes yields will rise, they can buy YT, which could appreciate in value. Since YT represents yield rights, it is cheaper than the principal. For instance, within 100 aUSDC, the YT might only be worth $5. This effectively gives the user 20x exposure to yield; or equivalently, 20x leverage on USDC.

If a user expects yields to remain stable, they can provide liquidity by supplying PT and YT pairs to liquidity pools, earning trading fees in addition to the base yield.

This approach is not novel in traditional finance, where interest and principal of income-generating instruments are routinely separated and used in derivatives to amplify returns or hedge risks.

However, upon closer inspection of trading volumes across Pendle’s various pairs, certain issues become apparent.

Source: app.sentio.xyz/share/lv18u9fyu1b558xf?from="-2M"&to="now"

From volume data, we see that Pendle’s peak TVL of several billion dollars was primarily driven by a continuous stream of ETH staking, restaking, liquid staking protocols, and flagship projects like Ethena—representing the most ambitious and best-executed supply-side efforts from Ethereum-based teams.

Yet today, no rational investor or speculator can deny that the staking frenzy triggered by the Shanghai upgrade in 2023 and the Merge back in 2022 failed to generate the anticipated wealth effect. Moreover, Pendle’s native design restricts it to only splitting interest-bearing assets, inherently filtering out potentially high-return "farm-and-dump" projects (like past examples such as OP, ARB, and Aptos).

In the first half of 2024—a period widely perceived as the beginning of a bull market—Pendle’s TVL surged dramatically. It grew from under $400 million in late January to nearly $5 billion by end-April. This explosive growth was fueled both by Ethena’s initial deposit campaigns and token airdrop, as well as a wave of restaking initiatives including EthFi, Renzo, and Puffer. However, without exception, these projects offered relatively generous short-term rewards, but after token listings, market participants quickly realized that the restaking narrative lacked broad acceptance. Meanwhile, Ethena’s synthetic dollar struggled to find real-world utility, and its core revenue source—funding rates from short perpetual positions—continued to decline. Collectively, these factors led to a collapse in both the broader narrative and ETH's value.

Historical TVL chart of Pendle based on DefiLlama data

The author does not dispute that Pendle represents a significant innovation in DeFi at the foundational level—even though its conceptual roots lie in traditional financial derivatives. The fundamental logic of splitting yield-bearing assets to achieve more stable or higher returns will likely remain a market necessity over the long term.

However, regarding Pendle’s token, its current market cap exceeds $600 million, supported by less than $2 billion in TVL, while its fully diluted valuation surpasses $1 billion. In the foreseeable future, its TVL is expected to continue declining.

Pendle’s tokenomics fundamentally depend on new LP pools formed from the yield-bearing assets it splits.

vePENDLE is Pendle’s governance token. By locking PENDLE, users receive vePENDLE, which grants voting rights in protocol governance and entitles holders to a share of Pendle’s revenue. Income for vePENDLE holders consists of: approximately 3% yield collected from YTs, and surplus income from unredeemed PTs after maturity—forming the base APY of vePENDLE. Additionally, vePENDLE voters can claim 80% of swap fees from the voting pool. Users who deposit vePENDLE into LP pools to provide liquidity also earn additional PENDLE rewards, potentially increasing total returns by up to 250%. PENDLE obtained through staking vests linearly over time, with a maximum lock-up period of two years. Ways to acquire PENDLE include depositing LSTs or native asset tokens into selected PT liquidity pools for rewards, or providing liquidity with vePENDLE in LP pools to earn further incentives.

Imagine a scenario where YT (yield tokens) deliver persistently negative annualized returns, and PT assets yield below 10%, even dipping below 5%. Meanwhile, the original projects behind these yield-bearing assets are one by one reaching their ultimate listing moments—when anticipated yields transition from abstract numbers into actual tokens in users’ wallets. At that point, how many will still choose to reinvest into Pendle to earn meager annualized returns?

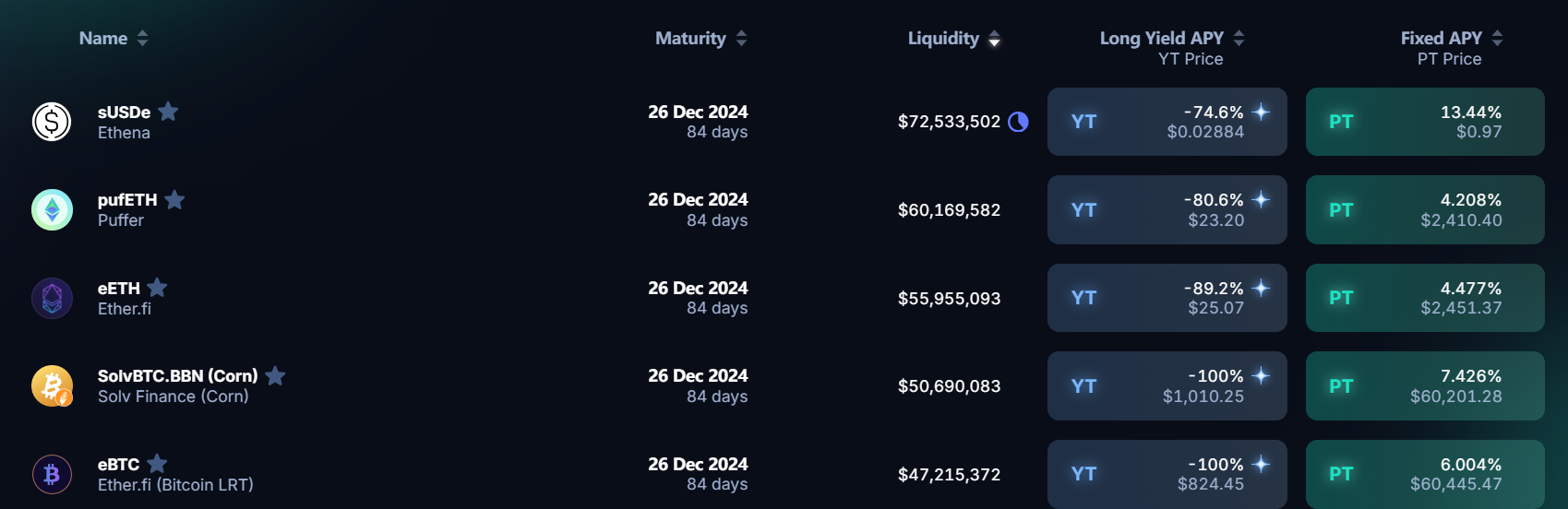

Pendle trading pairs ranked by liquidity at the time of writing

Let the author conclude with a quote from Wagner’s *Ring des Nibelungen*:

The young queen does not yet know that everything fate bestows has already been priced in secret.

Reference

app.sentio.xyz/share/lv18u9fyu1b558xf?from="-2M"&to="now"

PENDLE: A Severely Undervalued New Leader in DeFi – News-Odaily

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News