Web3 Gaming Investment Trends 20-24: A Fleeting Past, A Reborn Future

TechFlow Selected TechFlow Selected

Web3 Gaming Investment Trends 20-24: A Fleeting Past, A Reborn Future

How does Bitcoin's price volatility affect investment activities in the crypto gaming sector?

Author: Vladimir Sergeevih

Translation: TechFlow

The year 2020 was pivotal not only for the gaming industry but also for the cryptocurrency market. Bitcoin's price surged from around $7,200 at the beginning of the year to $29,000 by year-end, sparking widespread interest in blockchain projects. As gaming and crypto industries converged, the Web3 gaming market emerged, with numerous projects thriving under the "play-to-earn" model.

While we've consistently focused on the gaming aspects of Web3 games since then, we haven't yet explored the close relationship between cryptocurrency dynamics and investment activity in this sector. In this study, we examine several key questions:

-

How does Bitcoin’s price volatility affect investment activity in crypto gaming?

-

What differences exist in investor interest between content-focused and platform-focused crypto gaming startups?

-

Which startups have attracted the most significant investments, and what is their exit potential?

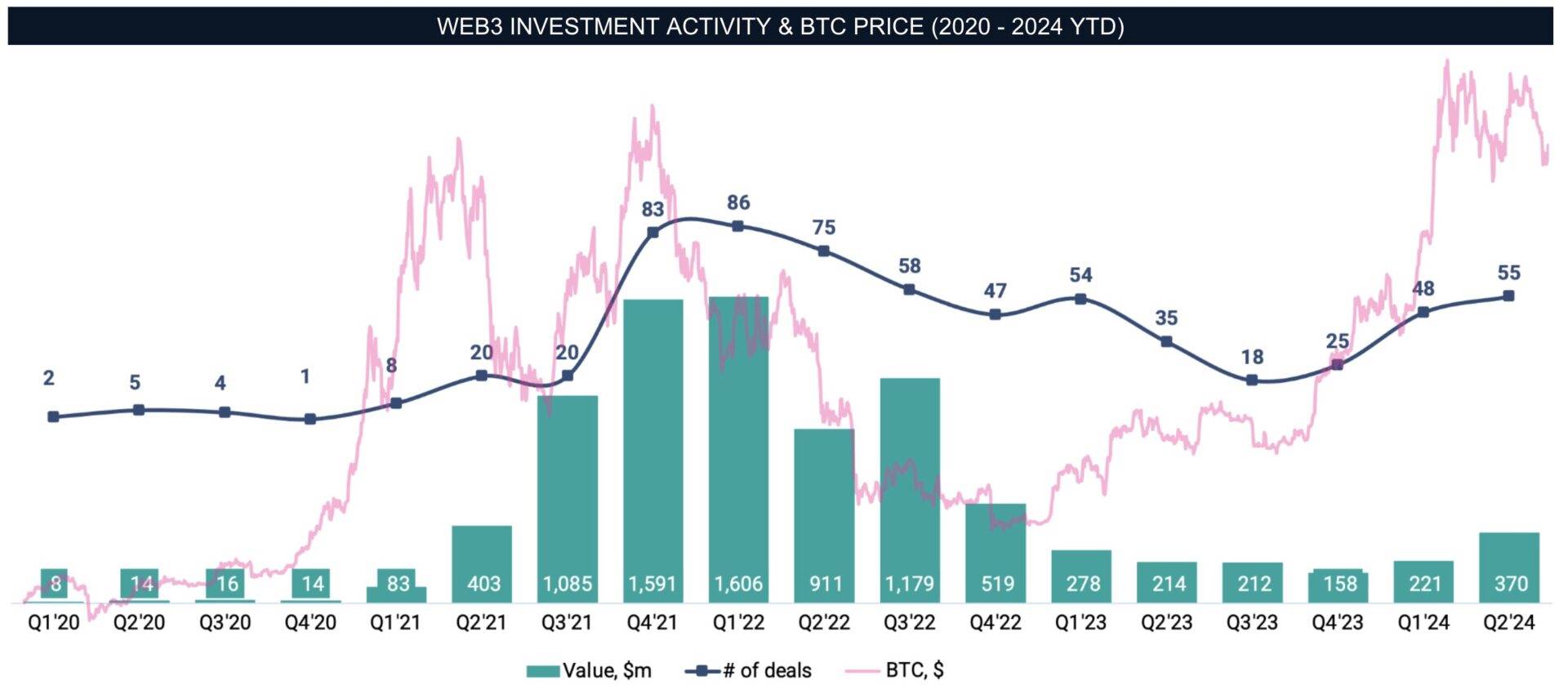

Impact of Bitcoin Price on Crypto Gaming Investments

Our data traces back to 2020. At the start of the year, investment activity in the crypto gaming space was relatively low due to limited general interest in cryptocurrencies, market volatility caused by the COVID-19 pandemic, and a lack of effective integrations between gaming and crypto. However, the situation changed significantly as the bull market cycle began toward the end of 2020 and peaked in early 2021.

The surge in Bitcoin’s price reignited broad interest in the crypto market, attracting new creators and investors and driving emerging trends in crypto gaming. In the first quarter of 2022, 85 deals raised up to $1.6 billion. Our analysis includes only private investments and excludes public crypto listings and token sales.

2022 marked the beginning of the crypto winter. In March, Ronin—the blockchain behind Axie Infinity—was hacked, resulting in the theft of approximately $625 million in assets. In May, the collapse of LUNA further worsened market conditions. By year-end, another major shock hit the industry: the collapse of the large cryptocurrency exchange FTX. Although these events occurred in quick succession, the decline in investment activity did not immediately reflect this; the downward trend became gradually apparent over several subsequent quarters, likely due to delays in deal announcements and market response lags.

In 2023, transaction activity remained weak and hit its lowest point in the third quarter—a period coinciding with early signs of Bitcoin's recovery. Notably, investment growth has not fully synchronized with Bitcoin’s price movements. Despite a new bull run beginning and Bitcoin surpassing previous highs in the first half of 2024, investment activity in the crypto gaming sector has not yet returned to earlier levels. This is partly because many projects have shut down and because Web3 gaming remains in its infancy, still exploring its user base and business models.

Investment Activity in the Crypto Gaming Sector

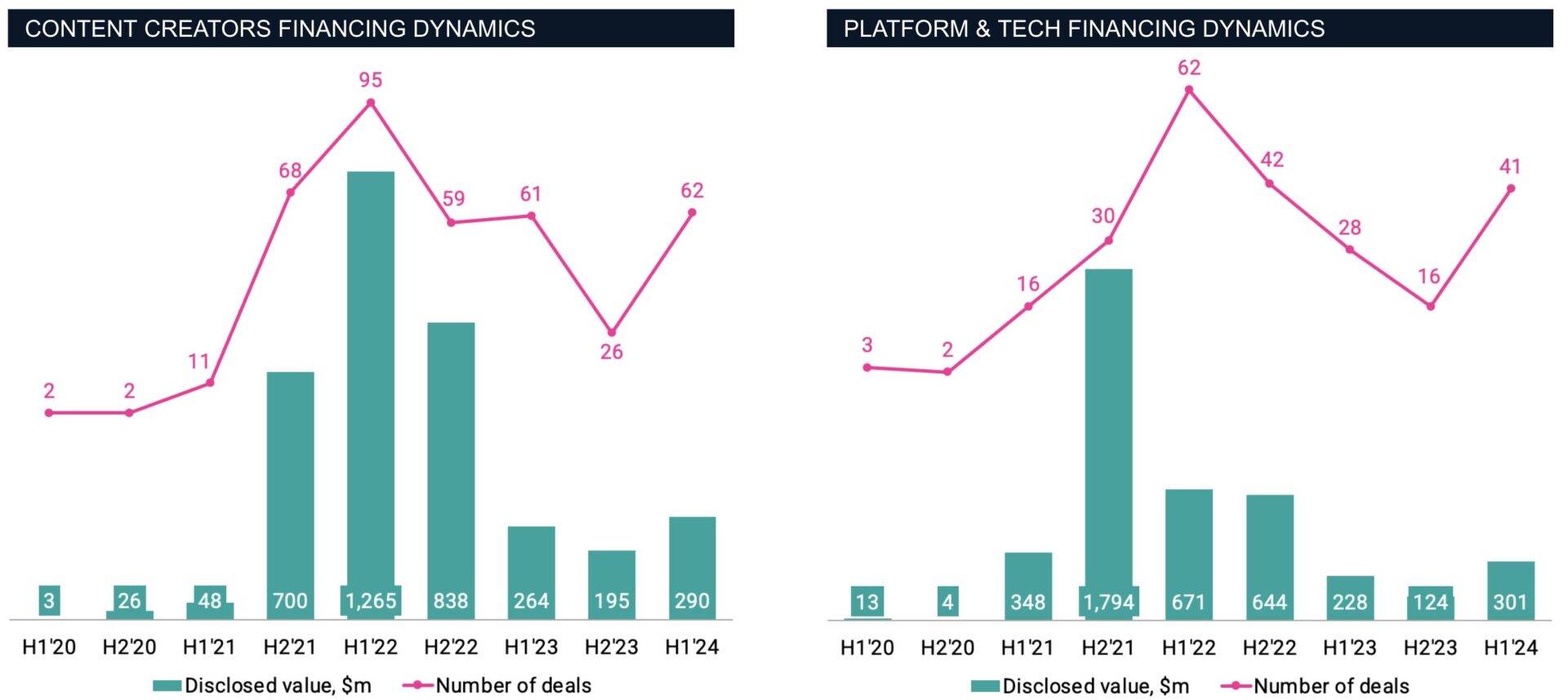

Before diving deeper into transactions, it's important to understand some basic context. Crypto gaming startups can broadly be divided into two main categories:

— Content: Companies that develop games and interactive experiences leveraging blockchain technology.

— Platforms and Technology: Companies providing infrastructure, tools, and technologies required for crypto gaming, such as blockchain infrastructure for games, development tools, and community platforms.

In 2020, NFTs—the core component of most Web3 games—were still relatively niche. That year saw nine announced deals totaling $46 million (four in content, five in platforms and technology). This low level of activity reflected the industry’s early stage and limited mainstream awareness. However, 2021 brought dramatic change.

As NFTs and the metaverse concept entered the mainstream and gained increasing media attention, investment activity surged. In 2021, there were 79 deals in the content category and 46 in platforms and technology, totaling $2.9 billion in funding—an enormous increase compared to the prior year. This growth was driven in part by the popularity of "play-to-earn" games and the early success of pioneers like Axie Infinity, which quickly became focal points for crypto enthusiasts and investors.

Note: Projects combining both content and platform elements have been excluded for clarity.

Initially accounting for 40% of total funding rounds in 2020, investments in content creators have since clearly surpassed those in platform and tech startups—both in number of deals and total capital—representing over 60% of both total fundraising amounts and transaction counts in the Web3 space. This may be due to game development studios offering greater scalability and/or faster return potential compared to other ecosystem participants. In the first half of 2022, investment momentum peaked, with 96 funding rounds completed by content startups versus 62 by platform and tech companies.

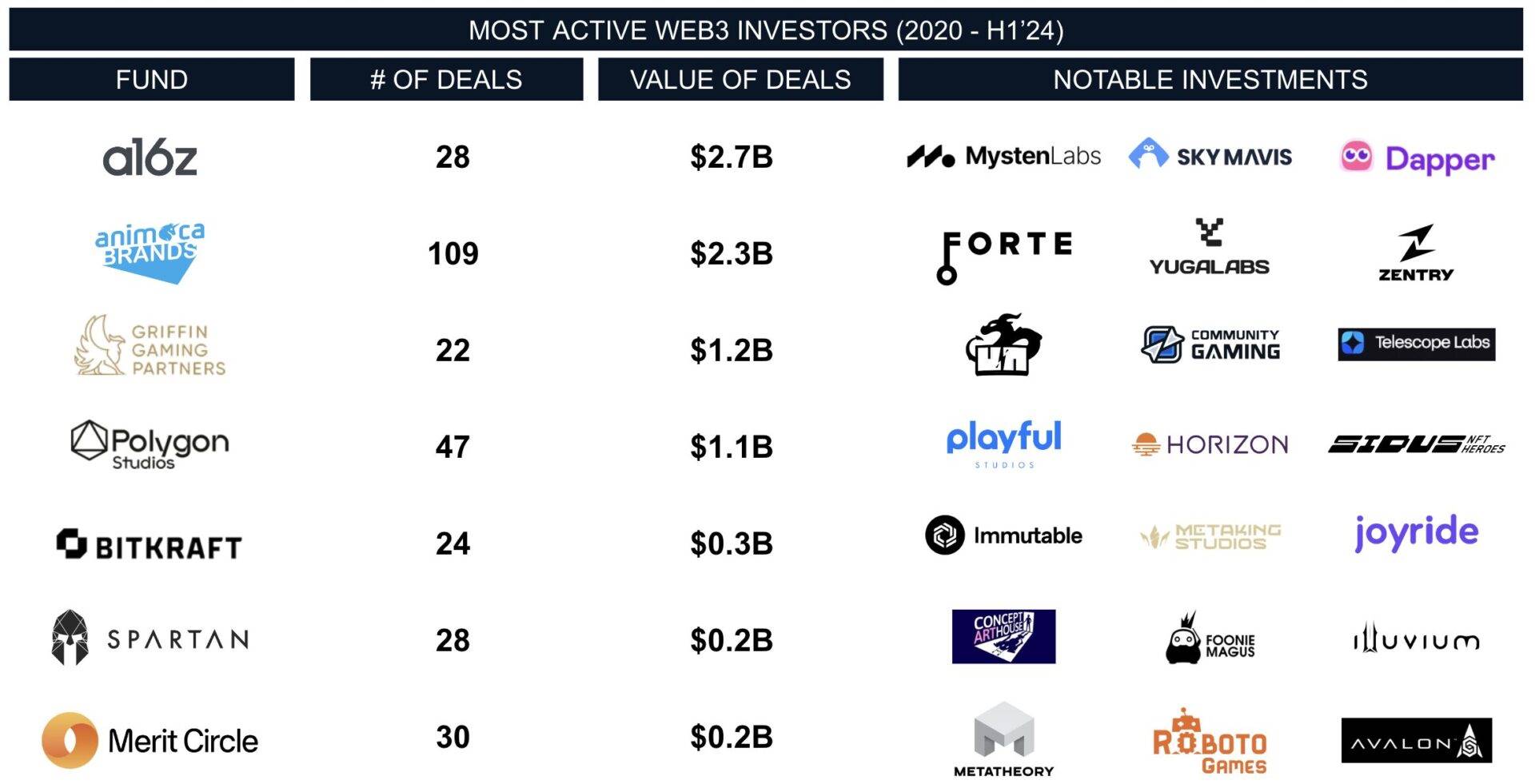

During this period, some of the most notable VC-led investments included Forte, Sorare, Yuga Labs, and Mysten Labs. Together, these four startups attracted nearly $2.4 billion—almost 30% of total crypto gaming investments from 2020 through 2024 so far.

Among the most active investors, Hong Kong-based Animoca Brands (ASX: AB1) stands out, having participated in nearly every major deal. Animoca Brands took part in 109 funding rounds totaling $2.3 billion, establishing itself as a leader in the field. Another key player is Andreessen Horowitz (a16z), a fund frequently featured in our VC rankings, which invested $2.7 billion across 28 deals. Griffin Gaming Partners and BITKRAFT operate at the intersection of Web3 and gaming, while Polygon, Merit Circle, and Spartan Group focus primarily on the crypto space. Today, the market is no longer dominated solely by crypto-native firms; mainstream venture capital firms are increasingly eager to identify and invest in emerging technologies in pursuit of outsized returns.

Exits in Web3 Gaming Startups

However, the M&A landscape tells a different story. The market remains in its early stages, with many startups not yet mature enough to become acquisition targets. While P2E and metaverse trends captured investor attention, their implementation has largely fallen short in practice.

Although there are some acquirers active in the space, such transactions remain relatively rare. For example, Wemade's $115 million acquisition of SundayToz was the largest known deal in the sector. Meanwhile, Animoca Brands has been involved in at least six M&A transactions, though financial details for most remain undisclosed.

Compared to the more common M&A activity in traditional gaming, exits in the crypto gaming market are scarce. Examples like NFT Tech's $6 million acquisition of Run It Wild or Pioneer's $4 million purchase of Bark Ventures represent typical small-scale deals in the sector. We have recorded 33 M&A transactions from 2020 to mid-2024, with a total disclosed value of $146 million.

The stark contrast between high investment levels and limited exits highlights that the crypto gaming industry is still in its early phase. While an increase in M&A activity is expected, the sector must first demonstrate greater maturity.

Key Takeaways

-

Bitcoin-driven investment spikes: The Bitcoin bull runs of 2021 and 2022 significantly boosted investment activity. However, the current bull market has failed to generate the same level of investor enthusiasm and confidence.

-

Crypto winter impact: While falling Bitcoin prices didn’t immediately affect investment flows, a series of negative headlines exacerbated the downturn, eroding trust among crypto enthusiasts and investors.

-

Content-focused investment dominance: Content creators continue to attract more funding than platform and tech companies and have achieved the largest exits in the Web3 space.

-

Disparity between high investment and limited M&A: Despite substantial capital inflows, M&A activity remains low—indicating the market is still immature. As the crypto gaming market matures, we expect both the frequency and scale of acquisitions to grow, gradually aligning with traditional gaming norms.

There is no one-size-fits-all path to success. Both investors and developers recognize that as emerging technologies integrate into daily life, new opportunities continuously emerge. Yet, there is currently no widely accepted business strategy for creating unique gaming experiences—the current approach remains largely speculative. Studios are experimenting with various business models: some focusing on "play-to-earn" mechanics, others relying primarily on one-time NFT resales or token listings for revenue.

In the first half of 2024, financing activity related to Web3 gaming has begun to show signs of recovery. Will this trend persist, or will it fade into history? Will we see top-tier games leveraging blockchain technology to enhance player engagement? These questions remain unanswered—and they will shape the future trajectory of the market and even influence Bitcoin’s price.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News