The Ethereum VC's "EBOLA" Dilemma: When Investment Logic Is Infected by the Token Burden

TechFlow Selected TechFlow Selected

The Ethereum VC's "EBOLA" Dilemma: When Investment Logic Is Infected by the Token Burden

Stop listening to VCs' forced infrastructure narrative—it's time for liquidity funds to thrive.

Author: Yash Agarwal

Translation: TechFlow

Ethereum venture investors are facing EBOLA — Ethereum Bags Over Logic Affliction.

(TechFlow note: "EBOLA" here is a pun in English. On the surface, it refers to infection with the Ebola virus, but actually describes a state where investors, holding large amounts of Ethereum-related assets ("bags"), neglect or suppress rational logical thinking.)

I will explain the origins of this highly contagious condition and how you can vaccinate yourself against it.

Two weeks ago, _choppingblock, hosseeb, and tomhschmidt from dragonfly_xyz raised a series of arguments in a discussion comparing Ethereum and Solana.

Roughly speaking, they claimed Solana has:

→ An incomplete venture capital ecosystem

→ Less capital than Ethereum

→ A memecoin chain

→ Launching on Ethereum is like "starting up" in the U.S., with higher EV+

We’ll review these arguments and:

— Highlight structural problems among large funds

— Explain how this pushes them toward infrastructure investments

— And worse, how this drowns founders in bad advice.

Finally, we'll share tactical advice on how to avoid catching EBOLA.

Chapter 1: Ethereum Venture Investors Are Infected With Highly Contagious EBOLA

As calilyliu put it, EBOLA (EVM Bias Obsession & Lack of Analysis) is a disease affecting Ethereum venture investors—a structural issue, especially for large "Tier-1" VCs.

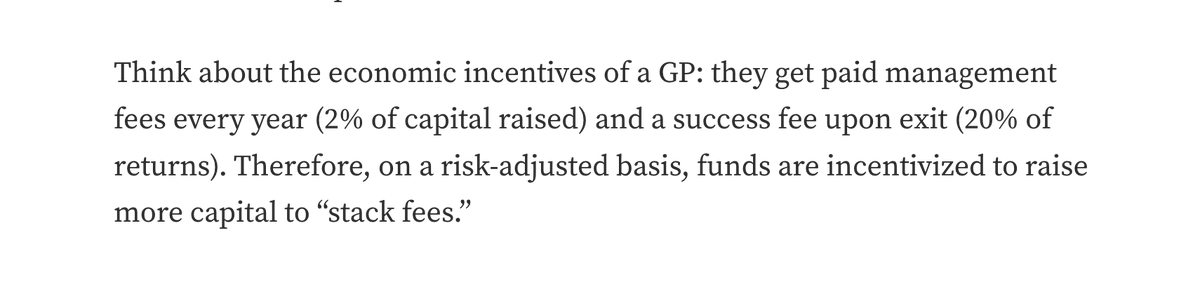

Take dragonfly_xyz (which raised $650 million) as an example—they likely pitched LPs with an infrastructure-heavy thesis.

Large funds are structurally incentivized to deploy capital—say, within 2–3 years—and must therefore fund larger rounds → leading to higher valuations.

If they don’t fund bigger rounds, they can’t deploy capital and would have to return it to LPs.

Given that infrastructure projects (like rollups, interoperability, restaking) can quickly reach FDVs over $1 billion, and considering the billions in infrastructure exits during 2021–2022, investing in infrastructure appears EV+.

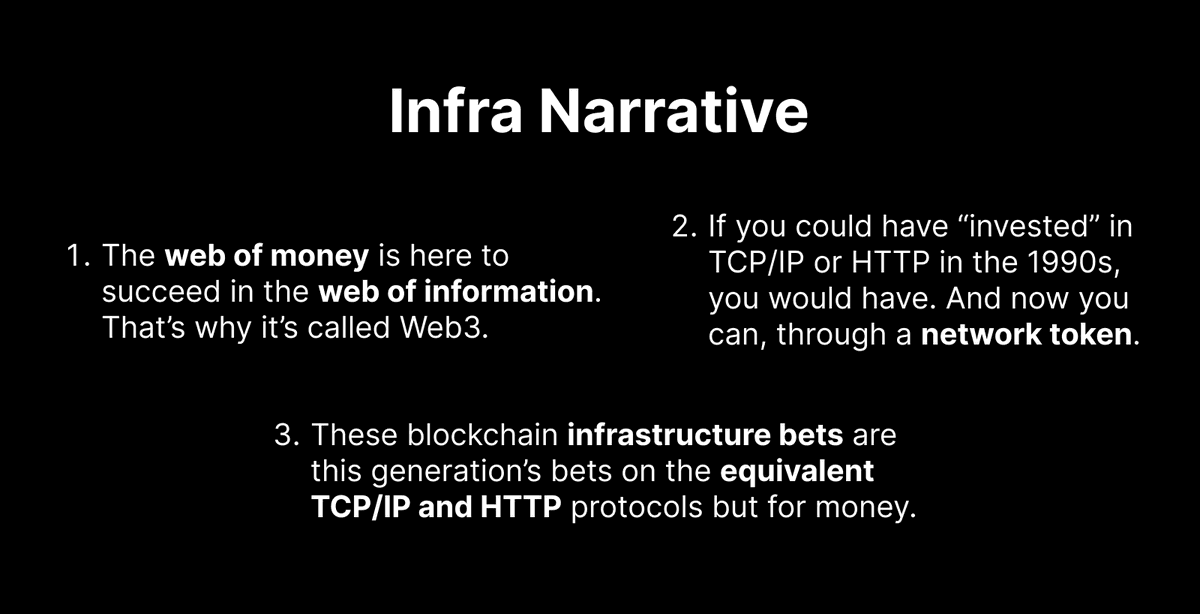

But this is a narrative they created themselves, accelerated by Silicon Valley’s capital and legitimacy engine.

The narrative is compelling—but the question is: when we consider the next EVM infrastructure stack, have we strayed from the original vision of a global monetary TCP/IP? Or is this rationale driven by the fund economics of large crypto funds like Paradigm, Polychain, and a16z crypto?

Chapter 2: EBOLA Makes Founders and LPs Uncomfortable

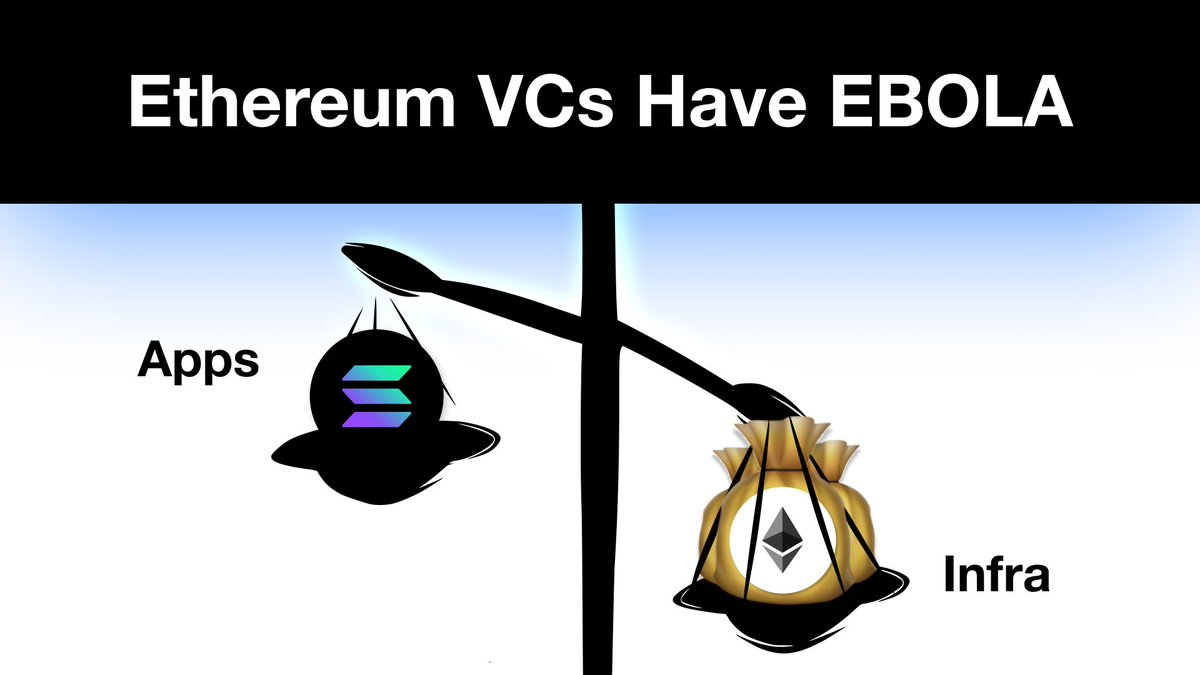

Because infrastructure brands command high valuations, many top-tier EVM applications have announced or launched L2s just to access those valuations.

The chase for EVM infrastructure is so intense that even elite consumer founders like the creator of pudgypenguins felt compelled to launch an L2.

Criticism of low-circulation, high-FDV projects is valid—so what about low-impact, high-FDV projects?

Take EigenLayer—a single project on Ethereum that raised $171 million, yet remains far from delivering any meaningful impact, let alone revenue. It will make certain VCs and insiders (holding 55% of tokens) rich.

The infrastructure bubble is already bursting. Many Tier-1 infrastructure projects from this cycle have launched tokens trading below their private round valuations.

With major unlocks coming in 6–12 months, VCs face losses, turning it into a race to exit first.

There's a reason broader market sentiment is turning anti-VC again—the prevailing feeling is:

More VC funding = more high-FDV, low-circulating infrastructure.

Chapter 3: The Graveyard of Bad VC Advice

Fueled by VCs, EBOLA has also infected promising apps and protocols. From social/consumer apps to high-frequency DeFi, many build on Ethereum despite modem-like performance and unaffordable gas fees—resulting in a graveyard of conceptually strong applications that never progress beyond “proof-of-concept” stage.

LensProtocol is one of the best examples of poor infrastructure advice.

The $140 million raise for StoryProtocol, led by a16zcrypto, aiming to “provide blockchain for intellectual property,” shows Tier-1 VCs doubling down on the infrastructure narrative—the only evolution being from “infrastructure” to “application-specific infrastructure.”

Chapter 4: Structurally Broken Venture Markets

Current venture markets fail to efficiently allocate capital between private and public markets.

Crypto VCs manage billions of dollars and are essentially mandated to deploy capital within the next 24 months—from private seed to Series A projects.

Insufficient public market capital leads to poor price discovery. For instance, all tokens launched in the first half of 2024 had a combined FDV of ~$100 billion—just half the market cap of the top 10–100 tokens.

Private venture markets are already shrinking. Even Haseeb admits it—these new funds are smaller than their predecessors, for obvious reasons. If they could, Paradigm would have raised at 100% of its prior fund size.

This structurally broken venture market isn't just a crypto problem.

The crypto market clearly needs more liquidity providers as structural buyers in public markets, which would help fix these broken venture dynamics.

Chapter 5: Vaccinate Yourself Against EBOLA

Enough. Let’s discuss potential solutions and what the industry needs to do—for both founders and investors.

For investors—favor liquid strategies. Scale by embracing public markets, not fighting them.

As Arthur_0x pointed out, an efficient liquid crypto market requires active fundamental investors—liquid crypto funds have massive room to grow.

19/ Multicoin’s TusharJain_ and KyleSamani summarized this well seven years ago: liquid funds can have the best of both worlds—VC economics (investing in early-stage tokens for outsized returns) combined with public market liquidity.

20/ In contrast to Ethereum, average fundraising sizes on Solana in 2023–24 were quite small, except for DePIN; nearly all initial raises were under $5 million.

Besides ColosseumOrg, key investors include _Frictionless_, 6thManVentures, goasymmetric, and BigBrainVC.

As liquid markets on Solana mature, liquid funds can act as contrarian investors for individuals and small institutions.

Large institutions should start targeting increasingly large liquid funds.

For founders—choose an ecosystem with low launch costs until you find product-market fit (PMF).

As naval said, stay small until you figure out what works.

Solana offers significantly lower launch costs compared to Ethereum.

As tarunchitra noted, on EVMs, achieving sufficient novelty and securing a good valuation often requires extensive infrastructure development—by nature resource-intensive (e.g., the entire app-as-a-Rollapp trend).

Apps typically don’t need huge funding to start—see Uniswap, pumpdotfun, and Polymarket.

Solana is the best place to “start up” because:

→ Community/ecosystem support

→ Scalable infrastructure

→ Fast execution mindset

Solana is more than just memecoins.

Many might say Solana DeFi is dead, and blue-chip projects like Orca and Solend/Save are underperforming—but data suggests otherwise:

While one might argue Solana DeFi token prices have crashed, so have Ethereum’s DeFi blue chips, highlighting structural issues with governance tokens in value accrual.

Final Chapter: Advice for Application Founders

The larger the fund, the less you should listen to their advice.

Pursuing Tier-1 VCs and high valuations—especially before finding PMF—leads to valuation burdens and discovery challenges at launch, making it harder to build a genuinely decentralized community around your project.

Fundraising—Raise Small. Be More Community-Oriented.

Raise from angel syndicates via platforms like echodotxyz—seek relevant founders/KOLs, or join accelerators like alliancedao or ColosseumOrg.

This is underrated: you trade valuation for distribution, enabling a strong launch.

Use superteam in very early stages—it’s a shortcut.

Consumer-Focused—Embrace Speculation. Capture Attention.

When VCs see billions in exits here, they’ll likely apply the same infrastructure playbook to consumer apps. We’ve already seen apps generating $100M+ annual revenue (e.g., pumpdotfun).

In short;

-

Stop listening to VCs pushing mandatory infrastructure narratives.

-

It’s time for liquid funds to thrive.

-

Build for consumers. Embrace speculation. Chase revenue.

-

Solana is the best place to experiment due to low launch costs.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News