Arthur Hayes: Now is the best time to invest in Bitcoin and altcoins

TechFlow Selected TechFlow Selected

Arthur Hayes: Now is the best time to invest in Bitcoin and altcoins

Fueled by the wave of central bank rate cuts, the cryptocurrency market is poised for a new bull run, with a strong market rebound on the horizon.

Author: Arthur Hayes

Translation: Ismay, BlockBeats

The U.S. dollar–Japanese yen exchange rate is the most important macroeconomic indicator. In my previous article "The Easy Button", I wrote that measures must be taken to strengthen the yen, proposing a solution whereby the Federal Reserve could use newly printed U.S. dollars to exchange with the Bank of Japan (BOJ) for unlimited yen. This would allow the BOJ to provide the Japanese Ministry of Finance (MOF) with unlimited U.S. dollar firepower to purchase yen in global foreign exchange markets.

While I still believe in the effectiveness of this solution, it appears the central bank charlatans running the G7 group of fools have chosen instead to let markets believe that the interest rate differential between the yen and the U.S. dollar, euro, British pound, and loonie (Canadian dollar) will narrow over time. If markets believe in this future state, they will buy yen and sell other currencies. Mission accomplished!

For this magic trick to work, the G7 central banks—the Federal Reserve, European Central Bank (ECB), Bank of Canada (BOC), and Bank of England (BOE)—must lower their "high" policy rates.

Critically, the Bank of Japan’s (BOJ) policy rate (green line) stands at 0.1%, while all others are between 4-5%. The interest rate differential between domestic and foreign currencies fundamentally drives exchange rates. From March 2020 to early 2022, everyone played the same game. As long as you stayed home, caught the flu, and got your mRNA vaccine shot, free money was yours. When inflation became so severe that elites could no longer ignore the suffering of their people, all G7 central banks—except the BOJ—aggressively raised rates.

The BOJ cannot raise rates because it owns over 50% of the Japanese Government Bond (JGB) market. When rates fall, JGB prices rise, making the BOJ appear solvent. However, if the BOJ allows rates to rise, JGB prices will fall, causing catastrophic losses for this highly leveraged central bank. I did some horrifying math for readers in "The Easy Button."

This is why, if G7 policymakers like Yellen want to narrow the rate differential, the only option is for those central banks with "high" policy rates to lower them. In traditional central banking theory, rate cuts are favorable when inflation is below target. But what is the target?

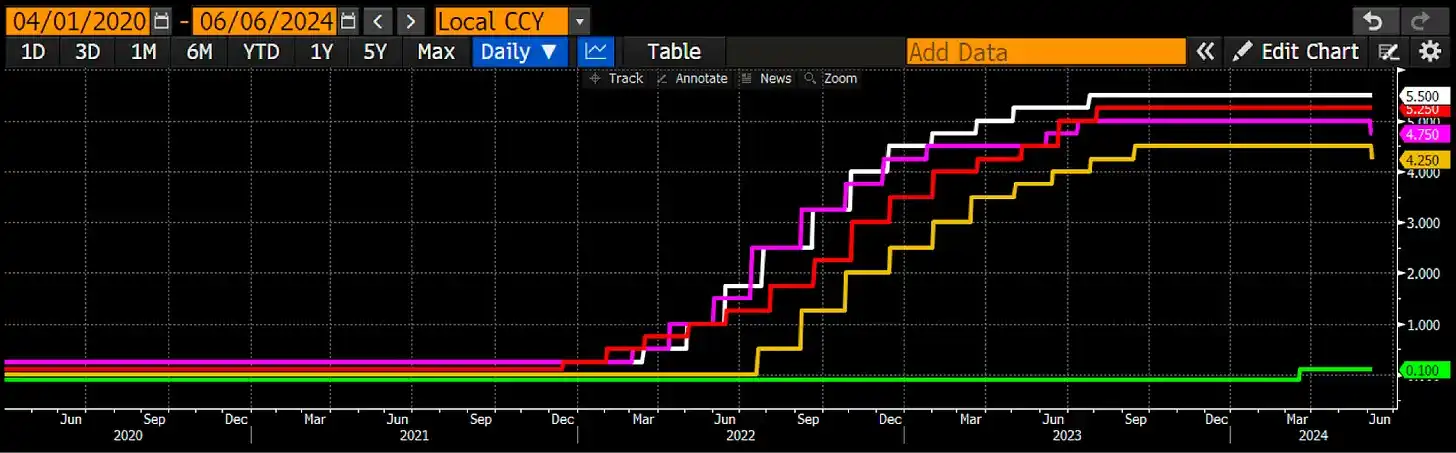

For some reason—unknown to me—every G7 central bank has an inflation target of 2%, regardless of differences in culture, growth, debt, demographics, etc. Are current inflation rates rapidly approaching 2%?

Each colored line represents a different G7 central bank's inflation reading. The horizontal line is 2%. Not a single G7 nation’s inflation data—even the manipulated and dishonest statistics released by governments—is below target. Putting on my technical analysis hat, it seems G7 inflation has formed a local bottom in the 2–3% range and is about to explode higher.

Given this chart, a conventional central banker would not cut rates at current levels. Yet this week, both the Bank of Canada (BOC) and the European Central Bank (ECB) cut rates despite inflation being above target. That’s odd. Is there some financial turmoil requiring cheaper money? No.

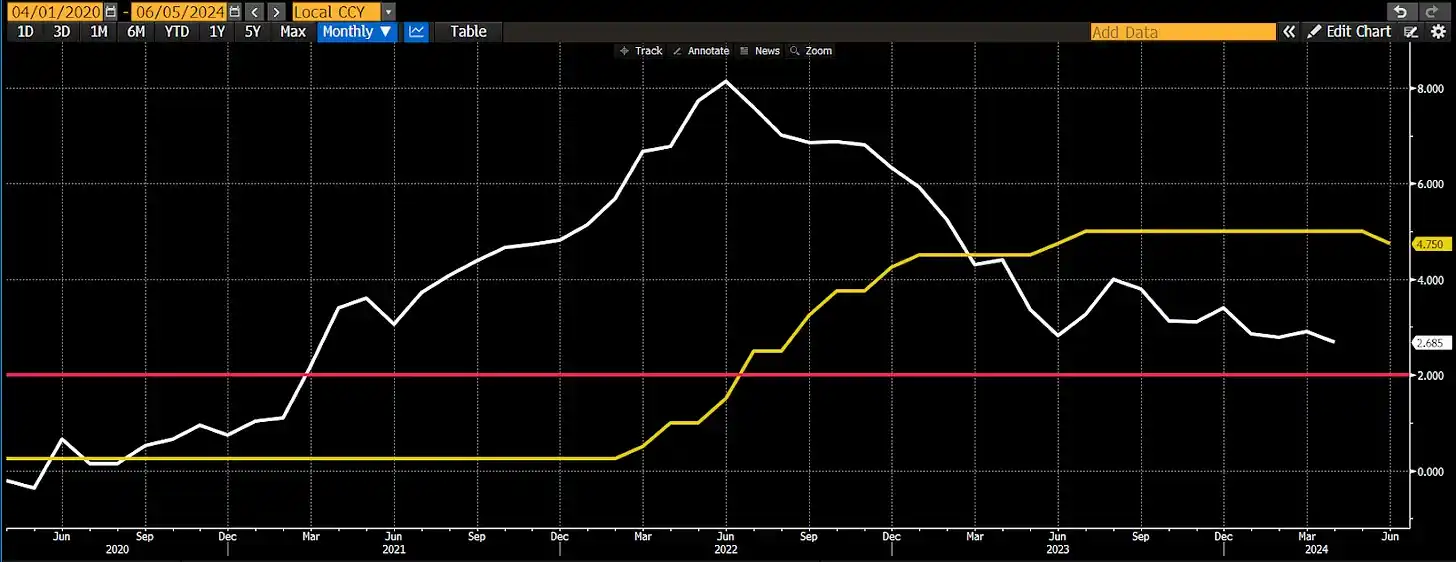

The Bank of Canada (BOC) lowered its policy rate (yellow) while inflation (white) remains above target (red).

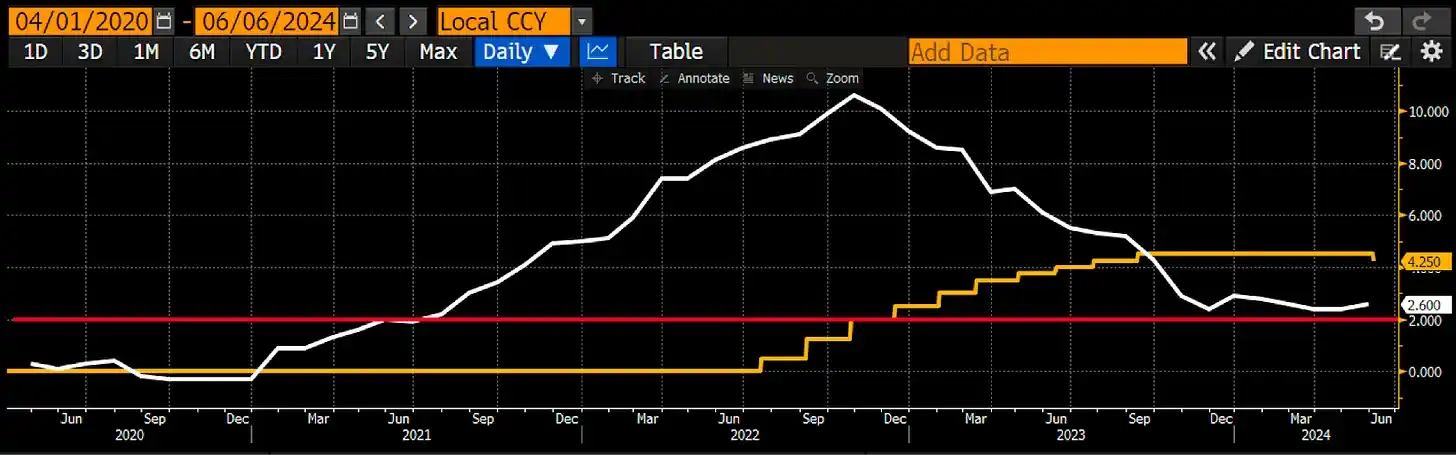

The European Central Bank (ECB) lowered its policy rate (yellow) while inflation (white) remains above target (red).

The problem is yen weakness. I believe Ms. Yellen has ended the rate-hiking "kabuki" show. Now it's time to preserve the U.S.-led global financial system. If the yen isn’t strengthened, China’s red communists—the big bad guys—will unleash a depreciated yuan to match Japan’s ultra-cheap yen, their main export competitor. In the process, U.S. Treasuries will be dumped, and if that happens, it means game over for the "Pax Americana."

What’s Next

The G7 will meet in one week. The communique after the meeting will attract great market attention. Will they announce some coordinated currency or bond market operation to strengthen the yen? Or will they remain silent but agree that, except for the BOJ, all others should begin cutting rates? Stay tuned!

The big question is whether the Fed will start cutting rates so close to the November U.S. presidential election. Normally, the Fed avoids changing policy near elections. However, normally the favored presidential candidate isn’t facing possible imprisonment, so I’m ready to adjust my thinking flexibly.

If the Fed cuts rates at the upcoming June meeting while their preferred adjusted inflation metric remains above target, the dollar-yen exchange rate will drop sharply—meaning the yen strengthens. Given that "Sleepy Joe" Biden has been crushed in polls due to rising prices, I don’t think the Fed is ready to cut. Ordinary Americans clearly care more about expensive vegetables than the cognitive abilities of the elderly man seeking re-election. Fair enough, Trump is also a "vegetable," given his love for McDonald’s fries and watching Shark Week. Nevertheless, I believe rate cuts would be political suicide. My base expectation is that the Fed will hold policy unchanged.

By June 13, when these amateurs sit down to enjoy their taxpayer-funded banquet, both the Fed and BOJ will have concluded their June policy meetings. As I said earlier, I expect no changes in monetary policy from either. Shortly after the G7 meeting, the Bank of England (BOE) will also convene. Although markets widely expect its policy rate to remain unchanged, given the BOC and ECB cuts, I think we might see a surprise cut. The BOE has nothing to lose. The Conservative Party is headed for a crushing defeat in the next election, so there’s no reason to defy orders from its former colonial master just to fight inflation.

Exiting the Turmoil Zone

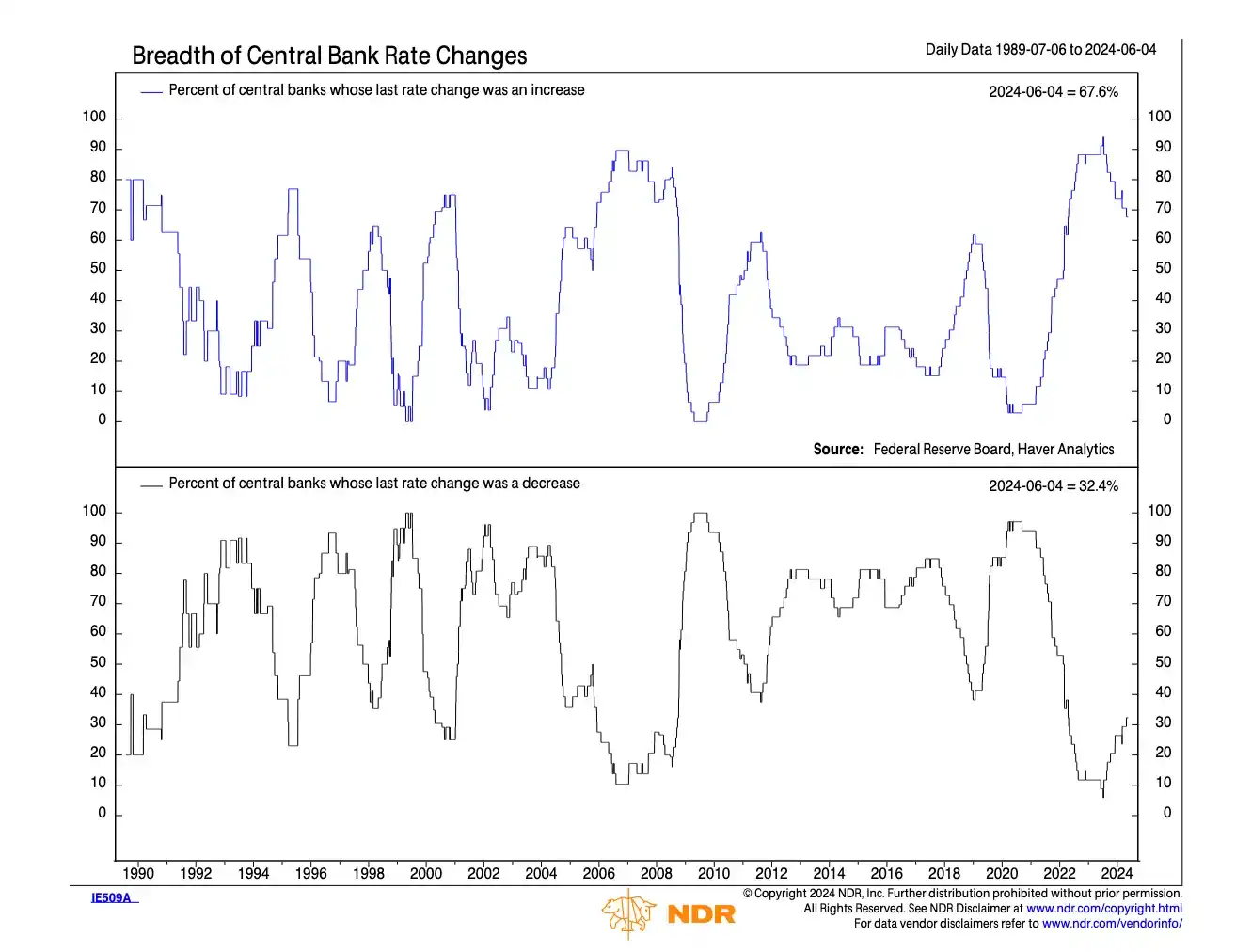

This week’s rate cuts by the Bank of Canada and the ECB mark the beginning of June’s central bank policy shifts, which will lift cryptocurrencies out of their midsummer lull in the Northern Hemisphere. This isn’t my baseline expectation. I originally thought the fireworks would ignite in August, around the time of the Fed’s Jackson Hole symposium—the usual venue for announcing sudden policy shifts in the fall.

The trend is clear. Peripheral central banks are starting their easing cycle.

We know how to play this game. It’s the same game we’ve been playing since 2009, when our savior Satoshi gave us the weapon to defeat the demons of traditional finance.

Go long Bitcoin, then altcoins.

The macro environment has shifted relative to my baseline, so my strategy will shift accordingly. For those Maelstrom portfolio projects asking whether to launch their tokens now or later, my answer is: launch now!

For my excess synthetic U.S. dollar cash holdings (e.g., Ethena’s USD, USDe) that are earning attractive annual yields, it’s time to redeploy into conviction altcoins. Of course, after I buy, I’ll tell readers exactly what they are. But one thing is certain: the crypto bull market is awakening and is about to pierce through the facade of profligate central bankers.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News