Understanding EthenaLabs ($USDe): Why USDe and Stablecoins Matter?

TechFlow Selected TechFlow Selected

Understanding EthenaLabs ($USDe): Why USDe and Stablecoins Matter?

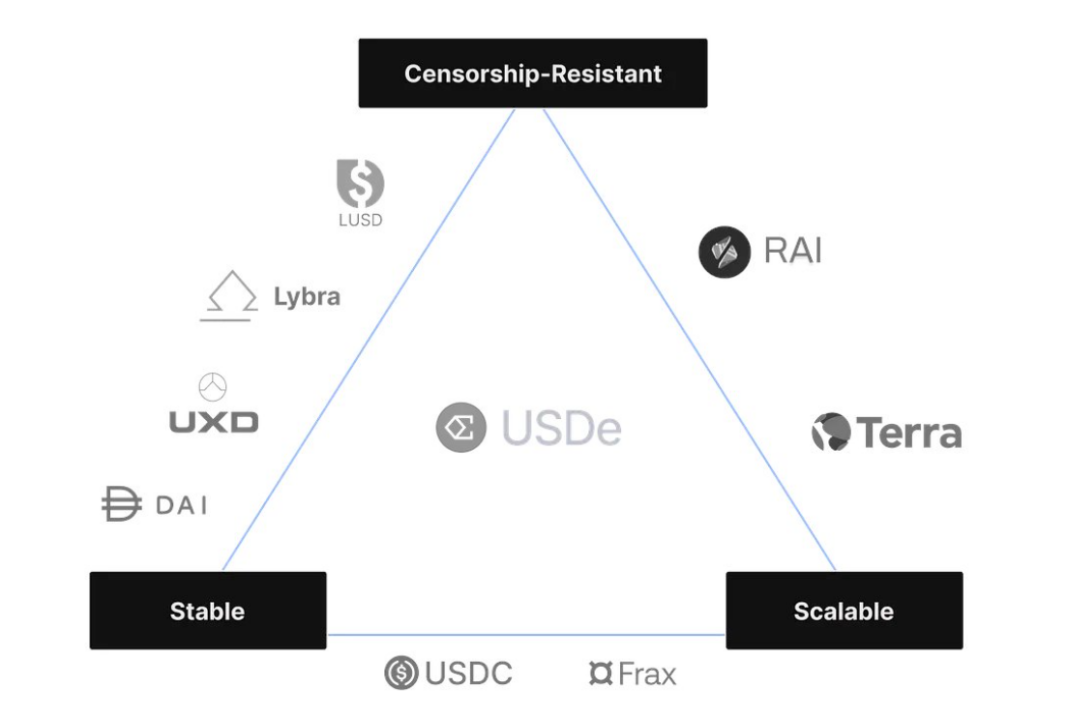

USDe aims to meet this growing demand by providing a censorship-resistant, scalable, and stable market option.

Author: Greythorn

Project Name: EthenaLabs

Network: Ethereum L1

Current TVL (Total Value Locked): $410 million

Project Type: CDP (Collateralized Debt Position)

Tokens: $USDe & $ENA

Crypto Ranking: #NA

Market Cap: NA

FDV (Fully Diluted Valuation): NA

Circulating Supply: NA

Total Supply: NA

Introduction

Following the collapse of Terra and its associated UST and Anchor protocols in 2022, interest in decentralized stablecoins sharply declined. However, as web3 continues to evolve, market cycles shift rapidly. Now, the Greythorn team observes projects such as Prisma, Liquity, and Lybra at the forefront of innovation in the LSD/CDP space. Meanwhile, Maker and Curve remain steady in terms of total value locked (TVL).

Source: Defillama

Many experts are questioning whether EthenaLabs’ new project, USDe, can sustain its ~27% annual percentage yield (APY) without replicating the investor trap seen with Anchor.

EthenaLabs reignited DeFi enthusiasm after announcing funding on July 12, 2023, by creating a dollar-pegged digital currency using LST (stETH). This raises an important question: Will it fully leverage Ethereum’s Layer 1 and Layer 2 ecosystems, or will it follow in LUNA’s footsteps as the next major failure in the crypto market?

Why USDe and Stablecoins Matter

Stablecoins have become key players in decentralized financial markets, significantly influencing market dynamics. They play a vital role in both spot and futures trading across centralized and decentralized platforms, supporting transactions and enhancing stability within the volatile cryptocurrency ecosystem.

In recent years, the stablecoin sector has experienced remarkable growth, with on-chain transaction volumes this year exceeding $9.4 trillion. Stablecoins represent two of the top five assets in DeFi and account for over 40% of total value locked (TVL). They dominate trading activity—data shows that over 90% of order book trades and more than 79% of on-chain transactions involve stablecoins.

Source: X: Route2FI

AllianceBernstein, a leading global asset management firm with $725 billion in assets under management (AUM), predicts the stablecoin market could reach $2.8 trillion by 2028. This forecast suggests massive growth potential from the current $13.8 billion market cap (which previously peaked at $18.7 billion).

The increasing adoption and consistent performance of stablecoins in both centralized and decentralized environments highlight their indispensable role in the crypto ecosystem. With optimistic projections indicating up to 2000% growth potential in this sector, significant opportunities emerge for investors and market participants to engage with innovative projects like EthenaLabs' USDe.

Specifically, USDe aims to meet this growing demand by offering a censorship-resistant, scalable, and stable market option.

Project Overview

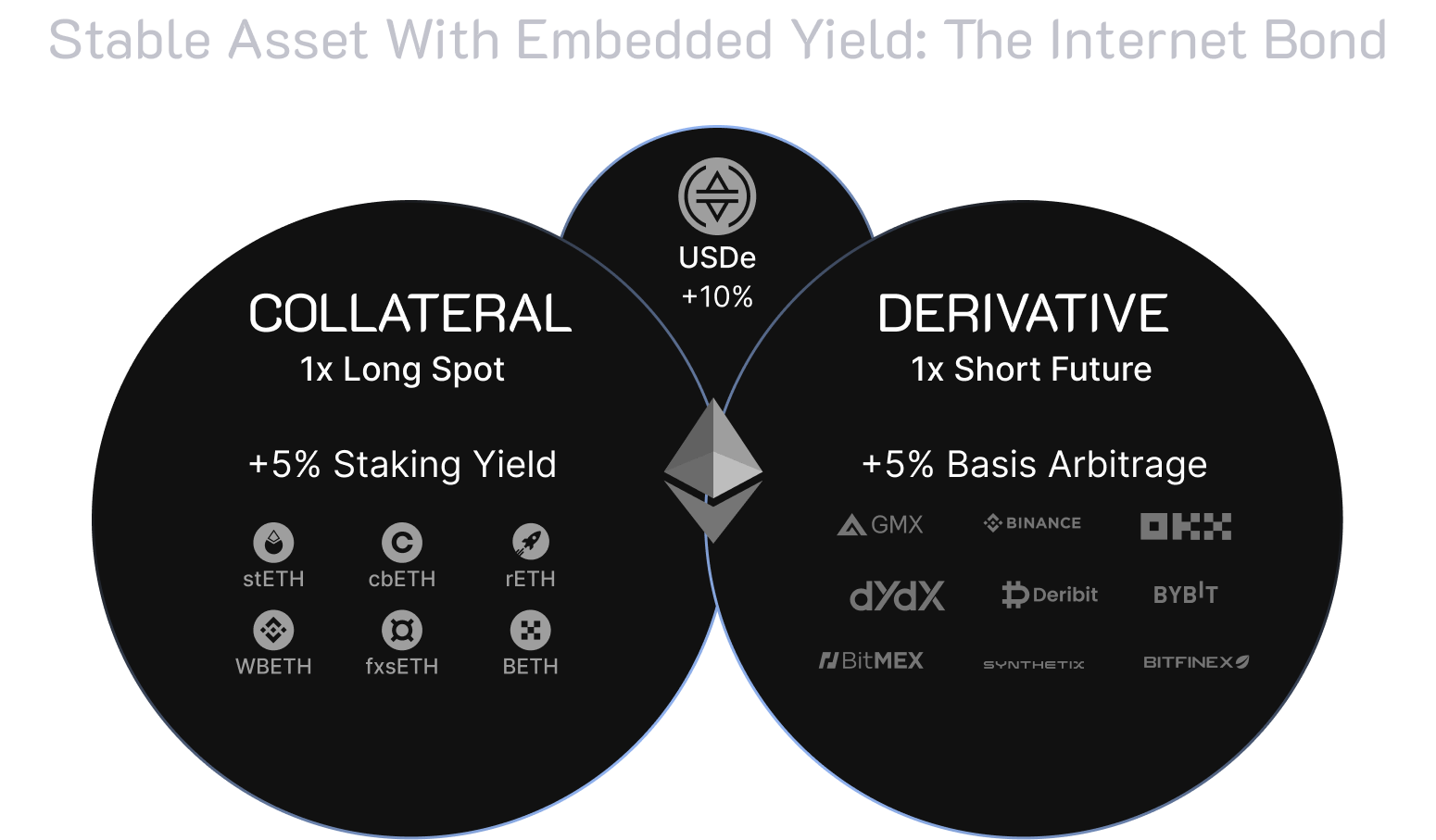

Inspired by Arthur Hayes’ “Dust to Crust” article, EthenaLabs is committed to creating a derivatives-backed stablecoin to address the crypto industry's reliance on traditional banking systems. Their goal is to offer a decentralized, permissionless savings product accessible to a broad audience. EthenaLabs’ synthetic dollar, USDe, aims to be the first crypto-native, censorship-resistant, scalable, and stable financial solution, achieved through delta hedging of staked Ethereum collateral.

EthenaLabs plans to introduce what they call the “Internet Bond,” alongside USDe. According to the EthenaLabs Gitbook, this will be a crypto-native, yield-generating, USD-denominated savings instrument backed by staked Ethereum and leveraging funding rate and basis differentials in perpetual contracts and futures markets.

EthenaLabs stands out due to its unique mission and innovative approach. Unlike other CDP projects such as Maker’s DAI, Liquity’s LUSD, and Curve’s crvUSD, EthenaLabs generates USDe’s USD value and yield through two primary strategies:

Utilizing stETH and its inherent yield.

Taking short ETH positions to balance delta and capture funding rates from perpetuals/futures.

This strategy enables the protocol to create a delta-neutral CDP by combining stETH spot deposits with corresponding short positions established via partnerships with centralized exchanges (CEXs) such as ByBit and Binance.

Holding sUSDe (staked USDe) essentially becomes a basis trade, balancing a spot stETH position against a short ETH position in the market. This setup exposes users to the yield differential between these positions, currently generating an approximate yield of ~27%.

Source: EthenaLabs Gitbook

USDe: Key Risks and EthenaLabs’ Mitigation Measures

Before diving into the risk-return analysis of staking USDe, it is essential to address several potential risks associated with EthenaLabs:

● Custodial Risk

EthenaLabs uses “off-exchange settlement” (OES) providers to custody assets, creating dependency on these providers’ operational capabilities. Challenges in executing key functions such as deposits, withdrawals, and swaps may impact protocol efficiency and USDe minting/redemption.

Mitigation Strategy: Custodian diversification – EthenaLabs effectively manages concentration risk by distributing collateral across multiple OES providers, minimizing exposure.

● Centralized Exchange (CEX) Risk

The protocol uses derivatives on centralized exchanges (e.g., Binance, Bybit) to delta-hedge collateral, posing risks if any exchange suddenly becomes unavailable.

Mitigation Strategy: Diversified CEX channels – By spreading assets across multiple exchanges, EthenaLabs reduces the risk of failure at any single exchange.

● Collateral Risk

The divergence between the collateral asset (stETH) and the underlying asset in perpetual futures (ETH) introduces “collateral risk.” Critical bugs in LSTs could lead to liquidity issues.

Mitigation Strategy: Active monitoring and partnerships – EthenaLabs actively monitors the on-chain integrity of stETH and maintains relationships with liquidity sources, ready to switch collateral if necessary.

● Liquidation Risk

Posting stETH as collateral for short ETHUSD and ETHUSDT positions introduces liquidation risk if the spread between ETH and stETH widens significantly.

Mitigation Strategy: Systematic collateral management – EthenaLabs has processes in place for rebalancing collateral, transferring assets, and utilizing insurance funds to guard against liquidation risk.

i. Systematic Collateral Rebalancing

Ethena will systematically allocate additional collateral during any risk scenario to improve the margin position of our hedged positions.

ii. Asset Transfer and Cyclical Collateral Deployment

Ethena can temporarily cycle collateral between exchanges to support specific situations.

iii. Insurance Fund Deployment

Ethena has the ability to rapidly deploy insurance funds to support hedged derivative positions on exchanges.

iv. Protecting Collateral Value

In extreme cases, such as critical smart contract flaws in staked Ethereum assets, Ethena will immediately take action to mitigate risk, solely motivated by protecting the value of the collateral. This includes closing hedged derivative positions to prevent liquidation concerns and converting affected assets into alternative ones.

● Funding Rate Risk

Persistent negative funding rates could reduce Ethena’s yield.

Mitigation Strategy: Insurance fund as yield protector – The insurance fund acts as a safety net when aggregate yield turns negative, ensuring collateral stability.

● Withdrawal Queue / Slashing Risk

Long queues for ETH withdrawals could negatively impact stETH.

Mitigation Strategy: This primarily depends on stETH and Lido’s performance; EthenaLabs does not have direct mitigation measures.

● Regulatory Risk

Concerns about regulatory controls on USDT, USDC, and DeFi may affect USDe’s growth in TVL, including challenges in user acquisition and retention.

Mitigation Strategy: EU-based operations with MiCA licensing – By aiming to operate under the EU’s MiCA regulations, EthenaLabs positions itself to effectively adapt to regulatory changes, reducing the impact of potential legal shifts.

EthenaLabs has developed a comprehensive approach to managing various operational risks, emphasizing diversification, active monitoring, and strategic planning to protect the protocol and its users.

Comparison with Anchor: Is the Yield Worth It?

Investors are encouraged to conduct their own research, especially when considering USDe, which offers a high stablecoin yield of approximately 27%. This yield draws comparisons to the Anchor protocol, highlighting systemic risks in the market where the failure of a single protocol could trigger broader financial turmoil.

Anchor’s downfall was primarily due to inherent risks in UST’s design, which relied on a reflexive mechanism tied to Luna’s price. A significant drop in Luna’s price posed a catastrophic devaluation risk to UST. Anchor offered fixed yields on UST (or aUST) based on Terra’s rate, promising a 19.45% APY regardless of market conditions.

Moreover, Anchor’s “real yield” from staked bAssets was only about 5.81%, far below the payout rate. This gap, combined with its dependence on Luna’s performance, laid the groundwork for a financial crisis.

For those interested in learning more about the collapse of Luna and UST, including Anchor’s mechanics, we previously covered it in detail in articles titled “Demystifying Anchor” and “The Collapse of Anchor.”

For USDe, its yield generation mechanism, associated risks, and marketing approach differ significantly from Anchor:

Transparent Marketing: Unlike Anchor’s promotion of “risk-free” returns, USDe’s marketing openly acknowledges risks and rewards. Its yield sources—from perpetual contracts (perps) and staked Ethereum (stETH)—are clearly communicated, setting realistic expectations.

Real Yield: sUSDe does not promise unsustainable high deposit rates. Instead, it delivers actual yield from its underlying assets, avoiding the trap of incentivizing borrowers with rates unsupported by asset earnings.

Avoiding Self-Collateralization: Unlike models that use their own tokens as collateral, sUSDe relies on stETH. Shifting the collateral base from the project’s own token to a more stable asset like stETH fundamentally alters the risk profile. The focus moves away from speculative risks tied to the project token toward more manageable liquidity risks related to ETH and stETH, along with other aforementioned risks.

Comparing USDe to UST’s collapse is misleading, as they differ fundamentally in risk structure and operational model. USDe investors should focus on understanding the specifics of perpetual funding, centralized exchange liquidity, and custodial risks—not the unsustainable high-yield strategies seen in the UST model.

Overall, compared to Terra’s UST, USDe presents a more thoughtful and potentially safer option in terms of risk mitigation and product design. By leveraging native yield and effectively managing risks from derivative sources, USDe stands out not only for its yield potential but also for its strategic design and risk management practices.

Outstanding Team and Support

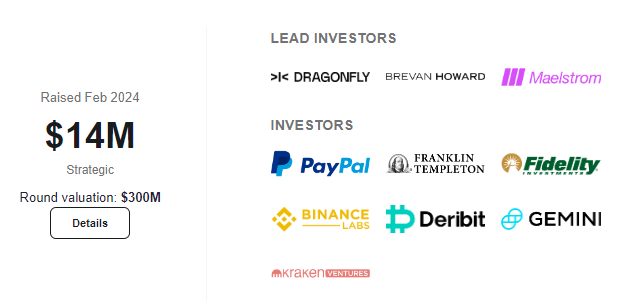

Under the leadership of @leptokurtic_, the Ethena team successfully completed three funding rounds, attracting substantial participation from centralized exchanges, market makers, DeFi innovators, and traditional financial institutions. This broad support underscores the project’s credibility and potential impact on the ecosystem.

Despite tight deadlines, the team demonstrated exceptional planning and coordination, ensuring the protocol was ready for mainnet launch. They prioritized risk management and security, conducting thorough audits before release.

Source: ICO Analytics: Ethena

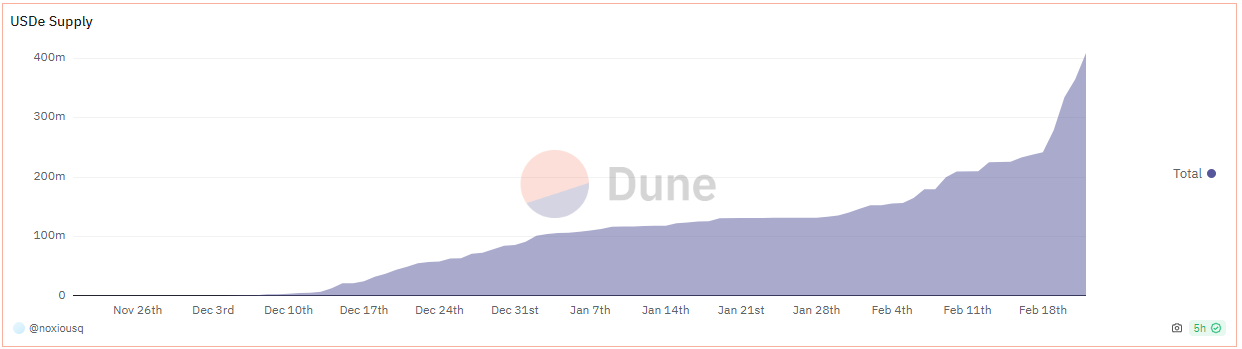

The success of the Shard airdrop campaign revealed strong market interest in decentralized stablecoins. Since early December 2023, total value locked (TVL) has increased 135-fold, reaching over $410 million—an impressive start to the initiative.

Source: @noxiousq Dune Analytics

This momentum indicates strong demand for products like USDe, attracting not only significant TVL but also investor attention aligned with its vision. As USDe moves forward, it aims to bring the next billion dollars of TVL into DeFi, potentially unlocking new opportunities similar to those seen during the Luna cycle. It prompts reflection: Could this mark the beginning of another transformative phase in decentralized finance?

Conclusion

At Greythorn, we focus on on-chain analytics, liquidity movements, and other actionable data. If you find our analysis valuable, we would greatly appreciate your support in joining our community. You can connect with us on LinkedIn, visit our website, or follow our X for deeper insights into the cryptocurrency world.

We also encourage you to stay updated on our latest findings, including comprehensive research on DePIN and ecosystem growth, Bittensor (TAO), and our exploration of ZKML on HyperOracle.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News