Multicoin Capital: Why We Chose to Invest in Pyth Network?

TechFlow Selected TechFlow Selected

Multicoin Capital: Why We Chose to Invest in Pyth Network?

The foundational primitive for developing oracle-based cryptographic applications, serving as a bridge between off-chain and on-chain states.

Author: Shayou Sengupta, Investment Partner at Multicoin Capital

Translation: 0xjs @Jinse Finance

We are excited to have recently invested in Pyth Network, a leading first-party data oracle in crypto.

The implicit premise behind traditional oracles in crypto is that all data—including financial data—is freely available and accessible to on-chain contracts. Thus, oracles only need to incentivize a supply-side network of contributors to collect and aggregate this data, reach consensus on it, and bring it on-chain. While this approach may work for widely available public datasets like weather data or election results, it typically fails for latency-sensitive data such as financial data. For time-critical financial data, large market participants (e.g., high-frequency trading firms, market makers, and order book exchanges) are inherently superior data sources compared to third-party aggregators because they generate the data (rather than merely scrape it), resulting in intrinsically higher-quality, lower-latency information.

Pyth’s oracle design rests on the argument that first-party financial data is not naturally open; rather, it is proprietary to its creators. Financial data is generated through real-time trading activity on centralized financial exchange venues—not by aggregation—and these venues, along with the entities most actively trading on them, represent the best sources of data. Therefore, Pyth partners directly with first-party data providers—market makers, trading desks, exchanges, etc.—instead of relying on third-party aggregators, delivering direct, low-latency price updates on-chain.

Launched in 2021, Pyth has since established partnerships with over 90 first-party data partners including CBOE, Wintermute, Two Sigma, Cumberland, and others. Today, Pyth delivers mid-market prices and credible interval pricing for over 400 assets—including BTC, TSLA, EUR/USD, cryptocurrencies, equities, FX, commodities, and interest rate products—to more than 45 different public blockchains. It secures over $1.7 billion in value across some of the largest protocols in crypto, such as MarginFi, Drift, Helium, Jupiter, Synthetix, Hashflow, and over 90 other protocols.

Beyond pioneering the first-party data contributor model in crypto, Pyth has also introduced a pull-based price publication model. Instead of continuously pushing data onto chains at fixed intervals (e.g., every 50 basis points deviation or hourly updates as with Chainlink), Pyth allows smart contracts to pull precise data exactly when needed. This novel design produces fresher, more accurate prices compared to oracles that update arbitrarily and periodically. It also structurally reduces costs for user protocols and applications, as they no longer pay for unnecessary updates. Furthermore, this design enables Pyth to scale asset and blockchain coverage more efficiently, as the pull mechanism eliminates the need for separate oracle deployments. For instance, applications built on Base and Mantle can integrate Pyth immediately without writing any custom code.

As a firm, we’re deeply interested in oracles because they serve as foundational primitives for crypto application development and act as bridges between off-chain and on-chain states. Their primary role is to keep prices consistent across liquidity venues; however, beneath this function lies a vast design space for capturing and redistributing value from urgent state transitions. In our research, Pyth’s model is currently best positioned to seize this opportunity and pave the way for protocols and applications to unlock new revenue streams via Oracle Extractable Value (OEV).

Introduction to Oracle Extractable Value (OEV)

To recap, Miner Extractable Value (MEV) is largely a misnomer. Today, it broadly refers to profits validators and stakers capture by reordering transactions to exploit arbitrage or liquidation opportunities arising from temporary state inconsistencies. Often, MEV emerges when the price represented within an application diverges from the canonical, accurate external off-chain price. Oracle Extractable Value (OEV) is a subset of MEV where applications depend on oracle updates—initiated by arbitrageurs or liquidators—to resolve such discrepancies.

By bringing external data—such as public market prices—on-chain, oracles naturally intervene in valuable blockspace. This creates profitable windows for arbitrage and liquidations between states and offers oracles themselves an opportunity (directly or through auction dynamics) to capture some of the MEV generated from price updates.

In push-based oracle systems, competition for transaction space following oracle updates is extremely intense. In pull-based oracle systems, applications have greater autonomy in choosing how and when to incorporate updates into their logic, allowing them better control over MEV extraction and/or redistribution mechanisms.

Let’s examine two examples that present MEV opportunities based on state transitions: one without OEV, and one with OEV.

1. MEV (oracle-independent): Application state becomes detached from external reality either organically or via on-chain actions. For example, if a whale executes a large buy order on a constant-function AMM, causing the quoted price to deviate from the external market price, bots can capture MEV by arbitraging the spread back to parity—without relying on a protocol requiring oracle updates.

2. OEV (oracle-dependent): A price change in external markets creates a profitable opportunity to restore the application state to the canonical off-chain state after the oracle imports the updated data on-chain. For instance, after adverse price movements on centralized price discovery venues, MEV bots might choose to liquidate underwater accounts on lending protocols.

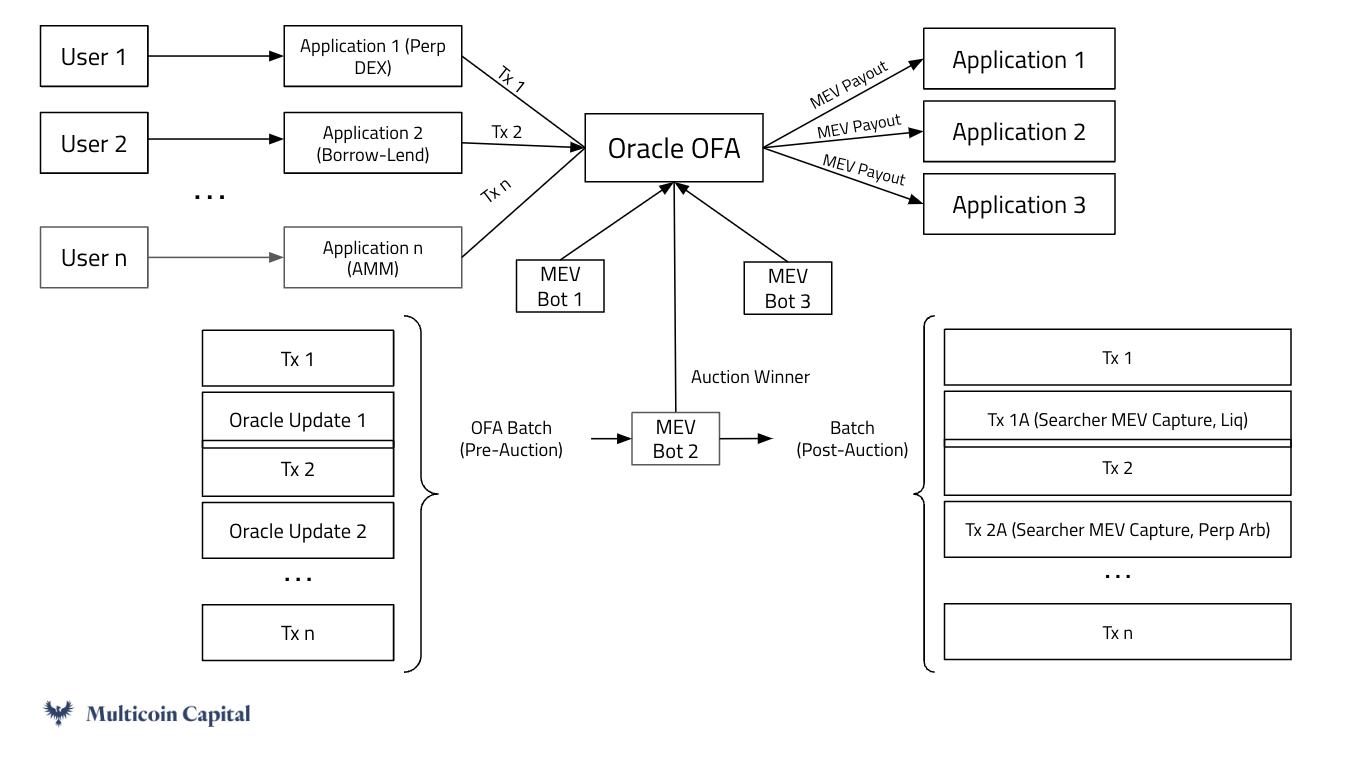

We classify OEV as the latter case, where oracle updates trigger value-capture opportunities. Currently, OEV-generating activities disproportionately benefit validators and stakers at the expense of their users—particularly liquidity providers. If protocols and applications could capture more OEV, they could redistribute these profits to incentivize and reward user loyalty. Ultimately, aligning OEV with users makes application protocols more competitive. Designing applications to capture MEV is challenging. All applications aim to minimize user-facing MEV and either effectively redistribute residual value to users or internalize it. Today, many developers believe the only viable path is deploying their protocol as a dedicated appchain, aiming to accrue value to their native token via MEV—but this introduces significant technical, operational, and interoperability complexity. The first-principles correct solution for internalizing MEV is conducting Order Flow Auctions (OFA). OFA creates a marketplace where the supply side consists of batches of MEV-prone transactions aggregated by the application, and the demand side comprises MEV bots or market makers seeking to insert or reorder these transactions to their advantage. Revenue from the auction flows directly to the application and represents a net share of MEV that the application can capture internally.

Implementing OEV Capture

An intuitive approach would be for applications to launch their own order flow auctions and profit from bids on blockspace surrounding oracle updates. However, this requires substantial effort. Each application controls only a limited amount of order flow, while OFAs are fundamentally markets that rely on deep liquidity from both sides—the maker (user transaction batches) and the taker (MEV bots). Application-specific OFAs fragment liquidity and limit atomic composability (e.g., if MEV bots cannot guarantee both legs of a strategy execute atomically—such as swapping tokens after seizing collateral to complete an arbitrage—they may reject the opportunity entirely). The operational and social overhead of configuring application-specific OFAs may outweigh the benefits, making in-house solutions unjustifiable.

A better path to capturing urgent MEV is outsourcing the auction via a Global Order Flow Auction (GOFA). Pyth is structurally positioned to run OFAs directly for all supported applications, as these applications already depend on Pyth’s oracle updates for system functionality. Consequently, Pyth has access to high-value blockspace across a broad set of applications, making it natural to commoditize the complement by monetizing the blockspace surrounding oracle updates—that is, the portion of blocks where MEV is extracted.

Rather than each application reinventing the wheel, a GOFA operated by the oracle leverages natural economies of scale. Deep liquidity attracts more liquidity: MEV bots are more likely to engage with bundled order flow spanning multiple applications due to atomic composability, and more applications are incentivized to participate when there are more competitive takers placing higher bids—which directly translate into revenue.

A New Frontier for Specialized Application OEV

OEV represents a novel method for oracles and applications to capture value. An oracle-run OFA directly transfers emerging OEV value to applications, enabling them to enjoy the benefits of having their own OFA without any overhead. As a neutral third party facilitating order flow exchange between applications and MEV bots, Pyth can choose to charge fees to either side, introducing a new revenue stream for the network without compromising ecosystem neutrality. We are excited about new mechanisms that enable tighter MEV capture directly at the application layer.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News