DigiFT x HashKey 10,000-Word RWA Research Report: Tokenization of Real-World Assets Ushers in the Next Generation of Capital Markets

TechFlow Selected TechFlow Selected

DigiFT x HashKey 10,000-Word RWA Research Report: Tokenization of Real-World Assets Ushers in the Next Generation of Capital Markets

In the medium to short term, due to the lack of stable-yield products in the crypto market and the demand for risk diversification, RWA market products will still be primarily fixed-income products.

Authored by: DigiFT and HashKey Capital

I. Executive Summary

Limited Scale, Unlimited Potential: Compared to traditional financial markets, the current market capitalization of RWA (Real-World Assets) stands at only several billion U.S. dollars—relatively small in size. However, driven by blockchain technology's efficiency and cost advantages, the potential market cap of RWA could reach tens of trillions of dollars within the next five years.

Supply-side dominated by fixed-income products; tokenized Treasuries rise while private credit shrinks: According to data from RWA.xyz and Dune.com, the total value locked (TVL) of major RWAs is currently concentrated in U.S. Treasury-related products, growing from $100 million in early 2023 to $784 million today—showing strong growth even during the crypto winter. In contrast, private credit TVL has declined from a peak of $1.5 billion in mid-2022 to just $500 million today, due to collapses such as FTX, 3AC, and Luna.

Demand primarily from institutional investors for short-term cash management and portfolio diversification: Analysis of wallet addresses holding Treasury-backed tokens reveals that institutional investors are the main holders. Current demand for RWA centers on short-term cash management needs among crypto investors. Additionally, DeFi protocols—including stablecoin and lending protocols—are increasingly incorporating RWA into their portfolios to achieve diversification and reduce systemic risk.

Regulatory challenges remain severe: Globally, RWA faces diverse regulatory environments. The United States enforces strict securities laws with global influence. In contrast, Switzerland, Singapore, and Hong Kong SAR have demonstrated proactive support, offering more favorable regulatory frameworks for RWA.

Innovative models integrating RWA with DeFi: Innovative business models like lending and token wrapping enable higher-threshold RWAs to be integrated into DeFi. However, unresolved challenges remain around anti-money laundering compliance, sales restrictions, and asset ownership rights. The convergence of RWA and DeFi will likely drive DeFi toward greater compliance.

Outlook: In the near to medium term, due to the lack of stable-yield products in crypto markets and the need for risk diversification, RWA offerings will continue to focus on fixed-income assets. In the long run, as market understanding of compliant assets deepens and legal frameworks mature, we expect to see a broader range of RWA assets—and potentially witness the emergence of a next-generation capital market powered by blockchain and tokenization.

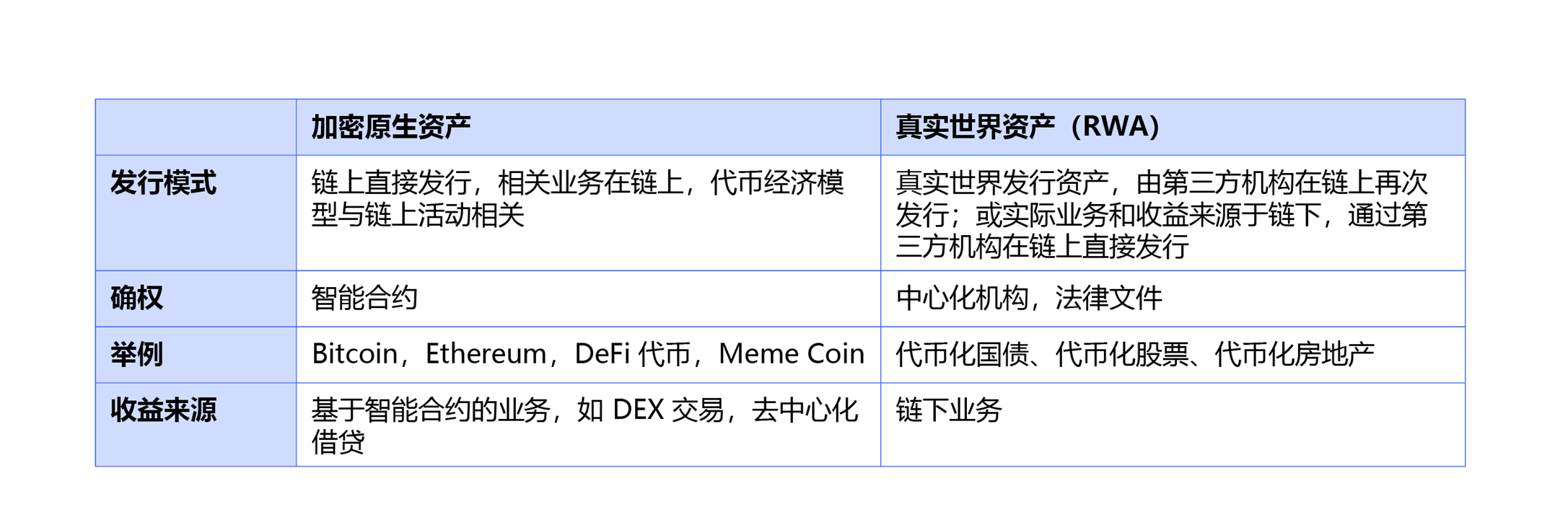

II. Introduction: Crypto-Native vs. Real World

Like the concept of "stablecoins," the idea of "real-world assets" (RWA) emerged in the development of blockchain-based digital assets as a metaphor. These metaphors are not meant to be novel for novelty’s sake, but rather to help people from different backgrounds intuitively understand new concepts through imagination and symbolic representation—without requiring extensive background knowledge. In technological innovation, metaphors serve as management tools, allowing explicit and tacit knowledge to be shared consciously or unconsciously.

Physical assets such as real estate and gold exist in the physical world. Unlike modern electronic systems, these tangible assets cannot inherently exist in digital form. To integrate them into electronic systems, issuers create corresponding digital representations. For electronic systems, such physical-world assets also qualify as “real-world assets.” Yet because they are already deeply embedded in daily life, people rarely view them as a distinct category.

In the crypto space, “real-world assets” refer specifically to tokenized forms where token holders possess legally recognized ownership rights over underlying off-chain assets. These include tokenized equities, bonds, and real estate—assets that originate outside the crypto ecosystem. Given the vast diversity of RWA types and implementation methods, the clearest way to define “real-world assets” may be by first defining “crypto-native assets,” thereby distinguishing between the two categories.

From a technical perspective, “real-world assets” simply involve mapping existing asset types onto blockchains via technological and legal mechanisms, using “tokens” to represent ownership of “underlying assets,” thus benefiting from the high efficiency and low cost of new financial settlement tools.

If a new technology offers breakthrough improvements in efficiency and cost reduction without fatal flaws, it will eventually be adopted. The evolution of financial transaction media—from paper certificates traded at the New York Stock Exchange decades ago, to today’s widely used electronic trading systems, and onward to tokenized formats built on blockchain—is an extremely likely developmental path.

Before the bridge between virtual and real worlds is fully established, crypto and the real economy remain disconnected. Thus, the concept of “real-world assets” serves as a metaphor enabling mutual understanding between these two realms—and is therefore widely discussed.

This research report focuses on one of the most significant—and likely future-dominant—segments of real-world assets (RWA): financial securities. We examine the current state of on-chain capital markets and explore what might shape the next generation.

These metaphors act as transitional forms, bridging crypto’s native assets with real-world integration. Blockchain is the new financial infrastructure, but the essence of finance should not change. This report concentrates on financial securities—the most important segment of RWA today and likely the dominant one in the future—to analyze the current state of on-chain capital markets and envision the next generation.

These metaphors serve as transitional forms, bridging crypto’s initial native assets with real-world integration; blockchain is the new financial technology infrastructure, but the essence of finance must remain unchanged.

III. Introduction: What Is RWA (Real-World Asset), and How Does It Work?

Crypto-native assets are mostly implemented via smart contracts, with all operational logic and business processes executed on-chain—examples include public chain tokens and DeFi tokens. In contrast, real-world assets (RWA) are far more complex and diverse. RWA can refer to any asset whose operations and returns do not originate on-chain—for example, wine, cars, (traditional) financial securities, and precious metals—all of which fall under the RWA umbrella.

Crypto-native assets use smart contracts to define rules—a principle often summarized in the crypto community as “code is law.” For real-world assets, however, the process is achieved through tokenization. Since more asset relationships occur off-chain in the real world, tokenization is not merely a matter of issuing a token on-chain, but involves a series of steps: purchasing the underlying asset, custody arrangements, establishing a legal framework linking the asset to the token, and finally issuing the token. Through tokenization—combined with off-chain regulations and operational procedures—token holders gain legal claims over the underlying assets. Therefore, especially for financial assets, off-chain legal frameworks are crucial, and RWA tokenization cannot happen outside the structures of the traditional world.

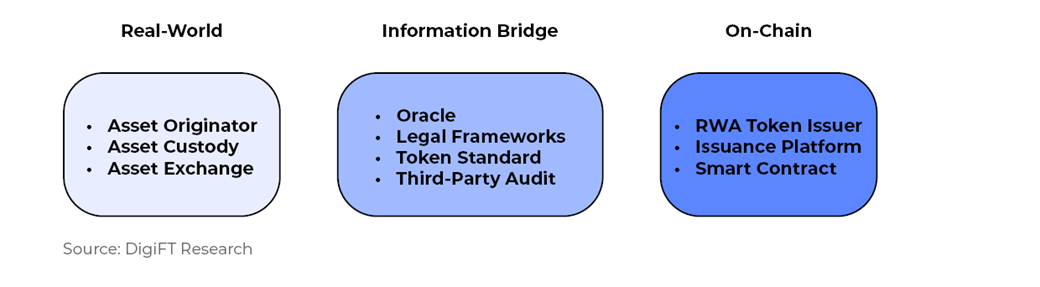

RWA Implementation Structure

RWA tokenization consists of three main components, with different roles fulfilled depending on the asset type:

-

Real World: Asset originator, custodian, purchase channel

-

Information Bridge: Oracle, legal framework, token standard, third-party audit, on/off-ramp payment channels

-

On-Chain: RWA token issuer, issuance platform, smart contract

Figure 1: RWA Implementation Architecture

IV. Issuance Models: Direct Issuance vs. Asset-Backed Model

Securities-type financial assets face relatively strict legal requirements. Starting from securities allows us to cover most scenarios encountered by various assets. Here, we mainly discuss the issuance and trading of security-type tokens.

From an issuance model perspective, crypto assets are typically issued directly, with asset ownership registration occurring directly on the blockchain. Since there are no real-world operations or underlying assets, their nature is difficult to clearly define. Generally, securities must register with relevant authorities; aside from Switzerland’s DLT Act, no jurisdiction explicitly permits direct issuance of securities on a blockchain. With few legal precedents available, current direct issuance models remain largely experimental—such as DigiFT and Diners Club Singapore’s issuance of the Diners Club 1-month note.

Crypto assets are highly homogeneous and volatile, whereas RWA assets exhibit lower volatility and weak correlation with crypto assets. This has created investor demand for RWA within the crypto world. To make RWA more acceptable, widely accepted assets are preferred—first the U.S. dollar (i.e., stablecoins), followed by U.S. Treasuries, which dominate current RWA offerings and belong to the category of security tokens. These assets cannot be issued directly unless sovereign entities (e.g., the U.S. government) issue them on-chain (e.g., CBDC). Therefore, another issuance model has emerged: acquiring corresponding assets in traditional capital markets and issuing a proportional number of tokens—an approach known as the asset-backed model.

This section discusses both models.

Classification of Asset Issuance Models

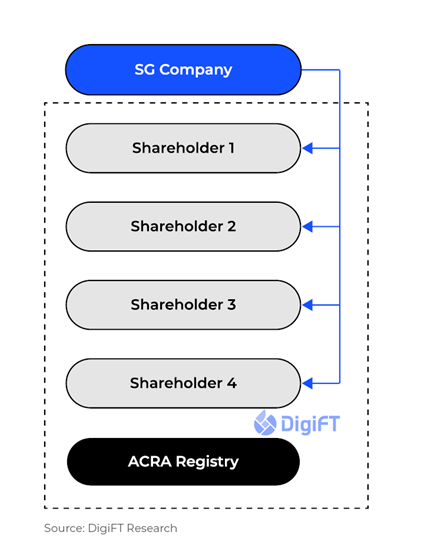

To understand RWA token issuance models, let’s first review traditional asset issuance—using equity as an example. The diagram below illustrates a typical equity issuance process for a Singapore company.

Figure 2: Traditional Stock Issuance Model

A company may have multiple shareholders, all of whom are registered with ACRA (Accounting and Corporate Regulatory Authority). Transfers and transactions must also be recorded with ACRA.

Here, ACRA acts as Singapore’s securities registrar. Other jurisdictions may have equivalent institutions—such as transfer agents in the U.S.—whose role is to register and maintain records of security holders.

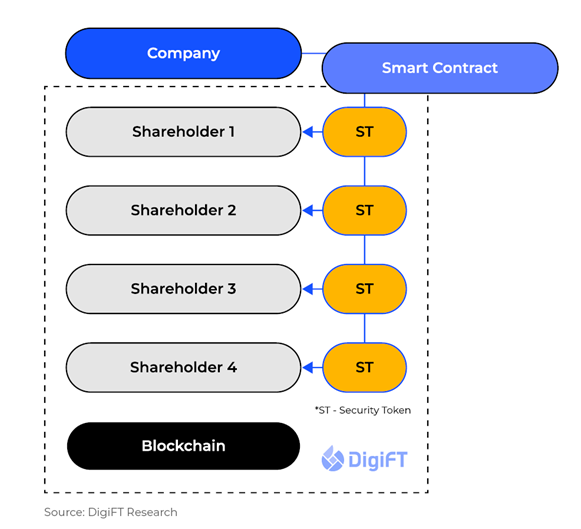

As shown below, issuing tokens on a blockchain means using the blockchain itself as a ledger for registering asset ownership and recording every transfer.

Figure 3: Direct Issuance Model

In a few leading jurisdictions with progressive financial innovation, such as Switzerland under its DLT Act, securities can be directly registered on blockchains. In these regions, authorized entities can issue securities directly on-chain, and the blockchain is legally recognized as a valid tool for rights registration. However, in most major financial markets—including the U.S., Singapore, and Hong Kong SAR—laws currently do not permit direct on-chain registration of securities. As a result, most projects take indirect approaches. For instance, Wall Street firms like Franklin Templeton issue funds on-chain but rely primarily on centralized accounting systems, using blockchain only as a secondary ledger.

Thus, the current market landscape includes two primary issuance models: direct issuance model and asset-backed model. Both involve issuing bonds on-chain, but differ fundamentally in structure and associated rights.

It should be noted that private securities may be issued compliantly if certain conditions are met—such as limited offering amounts, restricted investor types, and minimal impact on financial markets. Issuers may choose blockchain as the registration mechanism. This explains why most RWA projects currently target qualified investors only, a topic further explored in the “Challenges: Why Only Qualified Investors?” section.

Direct Issuance Model

In the direct issuance model, the asset issuer uses the blockchain as a ledger to register and issue tokens representing the asset. The token itself represents the underlying asset. Investors who purchase and hold such tokens directly acquire related rights—such as voting rights for stocks or repayment rights for bonds.

However, this model faces many limitations in the current environment. Tokenized securities are incompatible with mainstream exchanges (e.g., Nasdaq, SGX), creating friction costs. Legal frameworks are still incomplete, and there are insufficient judicial precedents to guide future rulings.

Asset-Backed Model

Due to incomplete regulations and limited on-chain assets, many projects opt for the asset-backed model. Essentially, the issued token is a new security representing the economic rights of the underlying asset. The asset issuer registers and manages the asset off-chain. A third party purchases the asset and issues tokens proportionally. Counterparty risk lies with both the asset issuer and the token issuer.

The asset-backed model is currently the most common RWA approach, enabling real-world yields to flow onto-chain. However, it introduces additional risks, and while the token captures the economic value of the underlying security, its rights may differ from those of the original instrument.

V. Current Landscape: Supply Dominated by Fixed-Income, Demand Driven by Institutions

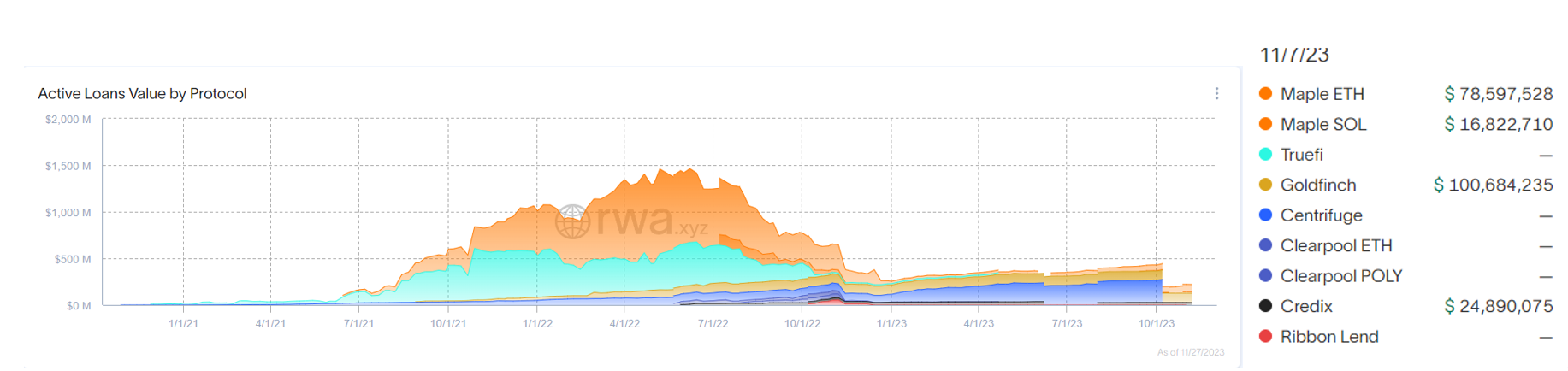

Currently, on-chain security-type RWAs are primarily private credit and tokenized U.S. Treasuries. The RWA space first gained traction in 2020 through private credit models, with unsecured lending being the dominant product—projects like Maple Finance, Clearpool, and Centrifuge leading the way.

Figure 4: RWA Private Credit Outstanding Loans by Protocol, Source: rwa.xyz, Data as of November 27, 2023

Private credit markets follow cycles. When trust prevails, borrowers are willing to pay reasonable interest rates, and lenders are ready to provide capital. After the collapses of Luna and FTX, multiple private credit pools suffered defaults, causing TVL to drop sharply and enter a relative trough.

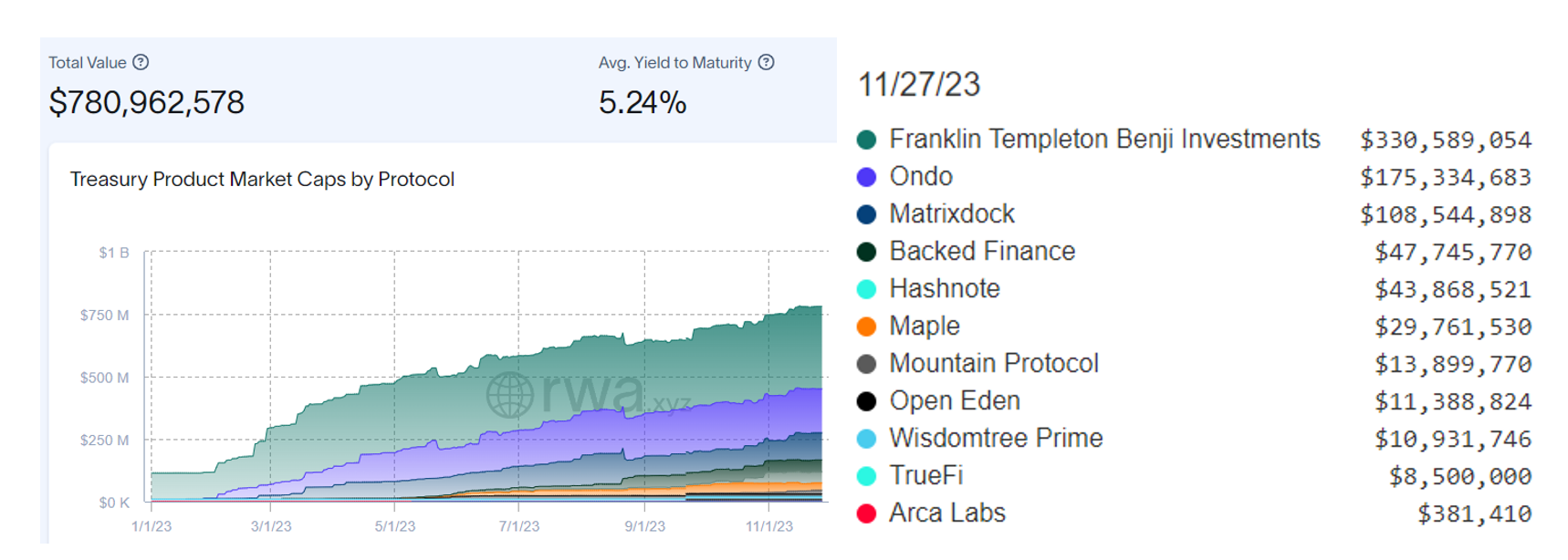

On the other hand, amid high external macro interest rates and the absence of yield in crypto markets, tokenized U.S. Treasury assets have surged. According to Defi Llama, TVL of Treasury-linked RWA projects continues to grow under clear market demand.

Figure 5: On-Chain Market Cap of U.S. Treasury-Related Tokens, Source: rwa.xyz, Data as of November 27, 2023

Two U.S. asset management giants—Franklin Templeton (green portion) and WisdomTree—have conducted Treasury tokenization experiments on the Stellar blockchain, each accumulating hundreds of millions in TVL. However, these projects rely on centralized ownership registries, using blockchain only as a secondary record of token ownership.

Holding Address Analysis

Compared to DeFi assets, RWA lacks excitement in terms of yield and gameplay. However, due to the safety of underlying assets, it attracts institutional investors seeking stable returns and high liquidity. Because they’re tied to real-world assets, most platforms require KYC and AML checks. For securities, regulations are stricter, often requiring investors to be accredited. These compliance barriers and yield considerations make RWA less accessible to retail users. Currently, most RWA TVL is concentrated in U.S. Treasury-related products. As the most consensus-driven, stable-yielding, and liquid asset class, U.S. Treasuries have been widely adopted by DeFi protocols and crypto investors amid macro bear markets.

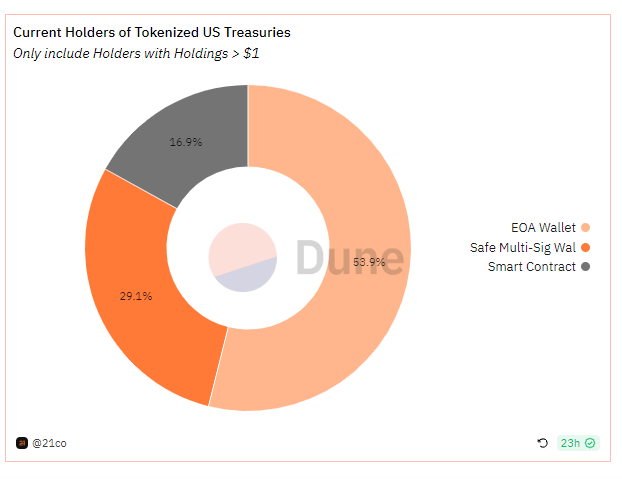

We observe that major RWA holdings are held by institutions, protocols, or used for short-term liquidity management or as underlying assets for structured products (discussed later in the “Innovation” section). By analyzing on-chain data, we examined key Treasury-related token holdings—data sourced from Ondo Finance OUSG, Maple Finance USDC Cash Management, Backed Finance bIB01/bIBTA, OpenEden Tbill, and MatrixDock STBT. We found that 29.1% (by USD value) of tokens are held in multi-sig addresses—indicating institutional/company ownership. Another 16.9% are held in smart contracts, representing DeFi applications such as Flux Finance, which uses Ondo’s OUSG tokens. These DeFi protocols transmit RWA yields permissionlessly into the DeFi ecosystem via lending mechanisms. The remaining 53.9% are held in EOA addresses. Considering that companies/institutions may use MPC wallets, third-party custodians, or hardware wallets—whose on-chain appearance remains as EOAs—the actual institutional share is likely even higher.

Figure 6: Distribution of U.S. Treasury-Related Token Holdings by Address Type, Source: Dune Analytics, 21co, Data as of November 27, 2023

RWA Status Summary: From B2B to B2B2C

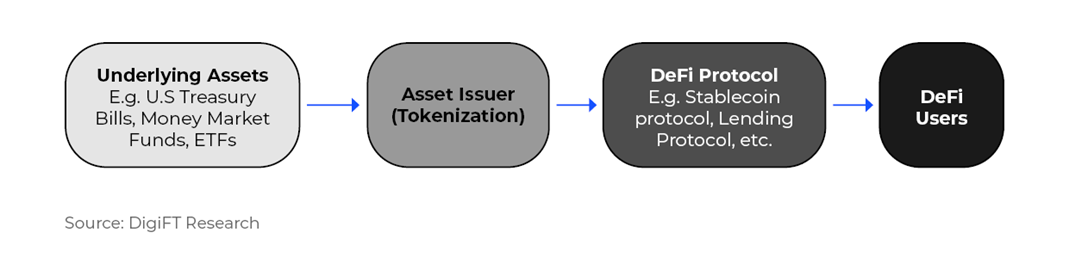

We believe that in the short term, direct RWA sales will remain B2B-focused. However, we also see RWA being integrated into DeFi as underlying assets for structured products. Examples include Angle Protocol (backed by Backed Finance bC3M), Spark Protocol (backed by MakerDAO’s trust-purchased Treasuries), USDV (backed by MatrixDock STBT), TProtocol (backed by MatrixDock STBT), Mantle mUSD (redeemable for Ondo Finance USDY), and Flux Finance (using Ondo Finance OUSG as collateral)—all forming B2B2C models. These integrations meet compliance needs while accelerating RWA adoption and real-world application.

Figure 7: RWA Asset Supply Chain

VI. Challenges: Why Limited to Accredited Investors?

Aside from a few projects that comply with local laws, special prospectuses, and specific securities registrations to offer RWA to retail investors under certain constraints (see the Innovation section), most current RWA offerings are limited to accredited investors. Depending on jurisdiction, investors must demonstrate a minimum level of financial assets—e.g., SGD 1 million (~USD 730,000) in Singapore—to qualify.

The reason most RWA products—including U.S. Treasury-linked ones—are limited to accredited or institutional investors is the high cost of compliant retail issuance.

This cost stems from the disconnect between the underlying asset and the final issued token. Securities laws impose strict requirements when offering securities to retail investors—including preparing and registering a prospectus. Moreover, most jurisdictions mandate that ownership of stocks and bonds be recorded in specific ways (e.g., in a register maintained by the issuer). Current authorities generally do not accept tokens or blockchains as valid ownership registries, meaning token ownership does not automatically confer legal title under these laws.

For asset-backed RWA—such as Treasury-linked tokens—there must be a “bridge” between the underlying asset and the intended RWA token. This bridge can be established by treating the RWA token as a standalone security, but this means the token must independently comply with all applicable securities laws—requiring the issuer to prepare and register a separate prospectus for the RWA token.

To understand this, consider the traditional process for retail securities issuance—whether stocks or bonds—which typically involves:

-

Internal preparation phase: determining the characteristics of the securities, selecting and hiring investment banks (underwriters) and other financial professionals (lawyers, accountants) to assist with the IPO process.

-

Selection of underwriter: who assists the company in preparing and executing the bond issuance.

-

Due diligence, audit, and rating (for bonds): reviewing internal controls and governance to ensure compliance; for bonds, ratings affect credit quality.

-

Prospectus: if targeting retail investors, it must be approved by regulators to ensure adequate disclosure.

-

Pricing: determining valuation and issuance price jointly with underwriters.

-

Marketing: roadshows, investor engagement, explaining the business.

-

Issuance and listing: meeting exchange listing requirements.

-

Post-trade management: financial disclosures, announcements, etc.

As seen, compliant retail securities issuance involves a complex process, hindered by two key factors:

-

High cost, low return. Full compliance can cost millions in fees and require regulatory approval. Given the relatively small scale of the crypto market compared to traditional finance, such issuance is too costly and offers insufficient returns.

-

Inadequate infrastructure. There are no compliant securities exchanges providing trading services for tokens, and securities registrars do not yet recognize tokens as valid ownership records.

To avoid these high costs and frictions, issuers limit offerings to accredited and institutional investors. Most current crypto-market RWA assets are issued by SPVs set up by startups. If using traditional assets like U.S. Treasuries as backing under the asset-backed model, investors buying these bonds are not purchasing Treasuries directly—but corporate bonds issued by the SPV backed by Treasuries—introducing significant counterparty risk. This downgrades the original AA+ rated U.S. Treasury to a BBB-rated corporate bond. Similarly, other directly issued corporate bonds are typically from smaller companies that skip full retail issuance procedures to save costs, resulting in eligibility being limited to accredited investors only.

VII. Drivers: A Two-Way Convergence Between Real World and Crypto

RWA connects both the real world (i.e., traditional finance for securities) and the crypto world. Current market participants show strong motivation from both sides.

Traditional World Drivers:

-

Adopting new financial infrastructure to reduce cost and improve efficiency. Blockchain consensus enables synchronized ledgers with enhanced security, drastically reducing settlement time and cost.

-

Self-custody. After multiple bank/financial institution failures, trust in traditional finance’s opacity has eroded. The self-custody feature of crypto assets is now gaining favor among mainstream capital.

-

Asset flexibility. Tokenized assets are transparent and seamlessly integrable with on-chain applications, enhancing user experience—lending, trading, staking—and even programmability via smart contracts.

-

Real-time settlement. Transactions and loans executed via on-chain smart contracts eliminate intermediaries, enabling direct clearing and settlement—reducing time and complexity.

-

Transparency and traceability. Records are real-time, public, transparent, and auditable—enabling instant monitoring and analysis.

-

Global access. Through DeFi infrastructure, investors can easily access global assets.

Crypto World Drivers:

-

Demand for on-chain asset management. On-chain asset managers seek stable yields and good liquidity—U.S. Treasuries and similar instruments are widely accepted.

-

Seeking alternative yield sources. Native on-chain yields come from staking, trading fees, and lending interest. During bear markets, activity declines, reducing these yields. To find uncorrelated income streams, RWA becomes essential.

-

Portfolio diversification. Sole reliance on on-chain assets leads to high correlation and volatility. Introducing stable, uncorrelated RWA enables hedging and richer investment strategies.

-

Introducing diversified collateral. High correlation among on-chain assets makes lending protocols prone to bank runs and mass liquidations—amplifying volatility. Adding low-correlation RWA helps mitigate this.

Amid the broader macro backdrop of yield-starved DeFi assets—with volatile and uncertain returns—traditional financial products offer richer, more robust hedging tools and steadier yields. Hence, DeFi protocols and Web3 institutions are turning to RWA.

Given the maturity of existing legal frameworks and product workflows, RWA will remain bond-centric in the near to medium term—until new market demands trigger the next cycle. We expect sustained demand for RWA, particularly bond-type assets, ahead of the next crypto risk-asset bull run. Primary demand comes from short-term cash management and from DeFi protocols transmitting yields to retail users to meet their liquidity needs. During risk-asset bull markets, RWA demand may wane, but new, higher-risk/higher-return RWA assets may emerge to compete with native crypto assets.

Building a new capital market on blockchain and smart contracts is a trend that, once established, will not reverse.

VIII. Global Regulation: U.S., Europe, and Asia

Since most RWA assets are tokenized securities, they fall under securities regulations in each jurisdiction. The U.S. is one of the few jurisdictions whose securities laws apply extraterritorially—making them particularly relevant and concerning to the crypto industry. U.S. securities laws apply to any securities offered to or by U.S. residents. To address the former, most RWA tokens explicitly exclude U.S. residents. For the latter, any RWA token launched by a U.S.-based company must either register with the SEC or (more likely) utilize a registration exemption. Examples include Regulation A/D (small offerings) and Regulation S (offerings outside the U.S.).

Regulation A (Reg A): Often called the “mini-IPO.”

-

Reg A Tier 1: Allows up to $20 million raised in 12 months, with lower ongoing reporting requirements, open to both accredited and non-accredited investors.

-

Reg A Tier 2: Allows up to $75 million raised in 12 months, with stricter reporting, open to both accredited and non-accredited investors.

Regulation D (Reg D): Provides exemptions from full SEC registration for certain private placements.

-

Rule 504: Allows up to $5 million raised in 12 months. Available to both accredited and non-accredited investors.

-

Rule 505: Allows up to $5 million raised in 12 months, limited to accredited investors and up to 35 non-accredited investors. Non-accredited investors must provide financial disclosures.

-

Rule 506(b): Allows unlimited fundraising from accredited investors and up to 35 non-accredited investors. General solicitation prohibited.

-

Rule 506(c): Permits general solicitation but restricts sales to accredited investors only.

Regulation S (Reg S): Exempts U.S. securities registration requirements for offerings made solely to non-U.S. persons and compliant with foreign jurisdiction rules. While Reg S offerings mainly target non-U.S. retail investors, U.S. issuers may participate as long as they follow applicable rules.

Unlike the U.S., the EU and Asia lack a unified securities framework—laws vary by jurisdiction. Within the EU, Switzerland notably supports tokenized securities and is among the few countries to legally recognize tokens as valid proof of ownership under its Digital Ledger Technology (DLT) Act.

In Asia, Singapore and Hong Kong SAR—longstanding traditional financial hubs—are also leading the way. Singapore’s government has repeatedly expressed support for asset tokenization. Reports indicate Hong Kong plans to release guidelines on security token offerings soon.

IX. Key Players: Participation Paths, Models, and Status

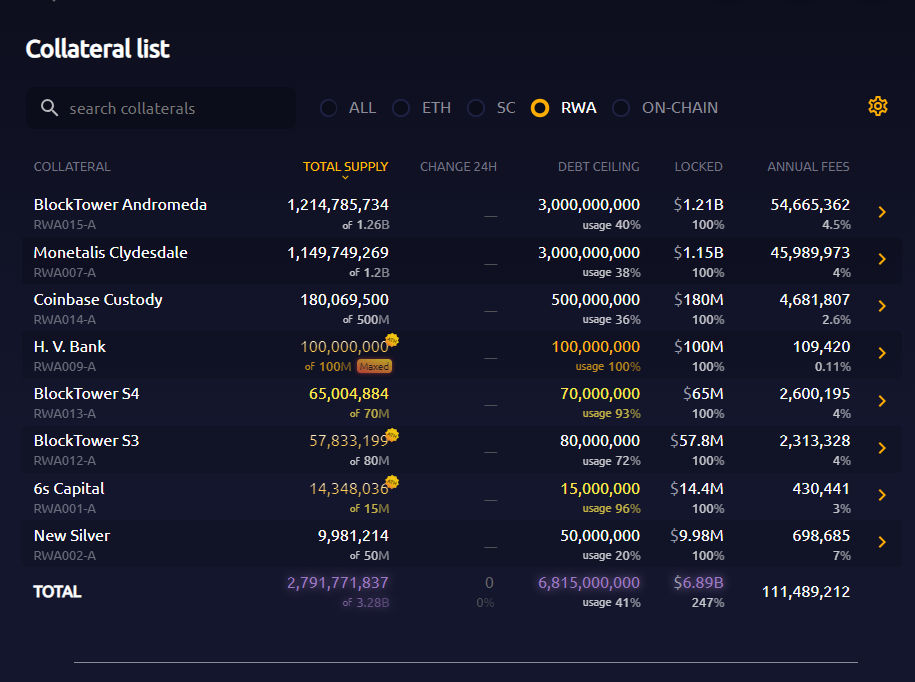

MakerDAO

MakerDAO is a stablecoin protocol that generates Dai by accepting collateral. As the largest DeFi protocol holding RWA on-chain, MakerDAO uses RWA as collateral to mint new Dai. Although most of MakerDAO’s RWA holdings are currently acquired off-chain, it remains central to any discussion of RWA.

MakerDAO began exploring RWA as collateral as early as 2021—one of the first projects to integrate RWA with DeFi. Initially partnering with lending protocol Centrifuge, MakerDAO brought off-chain assets on-chain as collateral to generate Dai.

Since Centrifuge’s issued assets were private credit—typically bonds from small companies (larger firms use traditional financing)—they carried higher default risks. For example, the ConsolFreight pool (linked to freight agent invoices) defaulted, exposing MakerDAO to $1.84 million in risk.

Figure 8: MakerDAO’s Current RWA Collateral Breakdown, Source: Makerburn.com, Data as of November 27, 2023

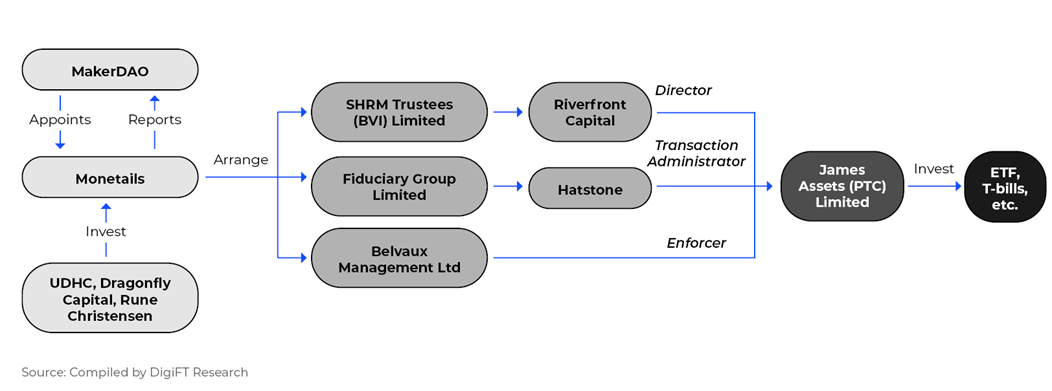

In early 2022, MakerDAO proposed using U.S. Treasuries as Dai collateral—initially aiming to generate yield from USDC held in its Peg Stability Module (PSM). This led to two initiatives: Monetalis Clydesdale (launched in 2022) and BlockTower Andromeda (launched in 2023). Both use off-chain trust structures benefiting MKR and DAI holders to purchase money market funds, U.S. Treasuries, or ETFs. Together, these projects have acquired over $2 billion in assets, used as collateral to mint Dai. For details on Monetalis Clydesdale’s structure, refer to DigiFT’s earlier MakerDAO RWA report.

Figure 9: MakerDAO Monetalis Clydesdale Trust Structure

MakerDAO is currently evaluating the possibility of tokenizing Treasury products, with proposals received from multiple platforms following a suggestion by strategic advisor Steakhouse.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News