The Past of Market Manipulation: The Love and Hate Between Market Makers, Project Teams, and Exchanges

TechFlow Selected TechFlow Selected

The Past of Market Manipulation: The Love and Hate Between Market Makers, Project Teams, and Exchanges

Users are not just users, they are also buyers.

Author: Guangwu, Founder of Canoe

The former FTX head of trade, @octopuuus, shared an interesting perspective on a podcast—the market maker’s point of view—jokingly referred to as “the old days of house操盘 lol.”

I’ll first summarize his description of Alameda's aggressive market-making style, then supplement it with other models I’m aware of from the last cycle, especially regarding the relationship between projects and market makers. The term "market maker" in this article specifically refers to entities involved in business related to exchanges and project tokens.

Institutional Trading Perspective

From an institutional standpoint, there are two main ways to manipulate token supply:

Strong Hand Control

When a project has solid fundamentals, select a target to operate on (whether or not the team is aware doesn’t matter much).

-

Phase One – Accumulation: A typical pattern involves continuous accumulation at low prices.

-

Phase Two – Consensus Among Market Makers: The key metric here is trading volume. First, push up the price slightly, then exchange holdings among other market makers during consolidation phases (recouping costs, improving capital efficiency, building risk management models).

-

Phase Three – Retail Investor Harvesting: Further pump the price while distributing tokens to recoup capital and fuel momentum. Some institutions may even proactively assist the project team in strengthening fundamentals at this stage.

Establishing Value Anchors for Tokens

This approach rapidly improves a project’s perceived fundamental quality through capital inflows and increased trading volume.

The best tools for this are lending and derivatives.

@octopus gave the example of lending: e.g., collateralizing FTT to borrow BTC/ETH. This effectively anchors FTT’s value to BTC and ETH. Through recursive borrowing with leverage, one could even use borrowed BTC/ETH to further boost FTT.

Another more sophisticated method involves futures (those eligible as margin, not perpetuals) and options. These instruments are relatively complex; during bull markets, market makers in crypto often don’t even need to deploy these tools to successfully run operations.

Relationship Between Projects and Market Makers

From the project side, relationships with market makers can generally be categorized as follows (ranging from top-tier to small studios):

-

If a project actively seeks listing, most CEXs will have requirements for market makers:

-

Some exchanges even designate preferred market makers. During listing stages, market makers can provide significant support—this is why many projects in the previous cycle were eager to secure investments from market makers.

-

Market making accounts usually require minimum collateral, such as holding at least $150K worth of token + USDT. This amount is often negotiable.

-

-

Terms offered by large market makers:

-

One type is passive market makers (more common in Europe), who offer strategy and technical support across hundreds of projects under a single model, charging around $3,000–$5,000 per month.

-

Another charges a tech fee (~$6,000/quarter) plus profit sharing (common in China). Profit sharing means splitting proceeds from selling tokens. For instance, if they sell $1M worth of tokens, profits might be split 70/30. These market makers share some interest alignment with the project team, but retain full control. A key negotiation point is reserve ratio: (market making funds / circulating market cap). To maintain influence over price action, this ratio should ideally be 30%–50%, preventing collapse post-listing (e.g., falling below private sale prices).

-

A third model, common among U.S.-based market makers, involves borrowing tokens—e.g., taking a 3% loan from the project team, returning principal plus interest at maturity. Such terms are illegal in the U.S., so contracts typically include disclaimers differentiating them from securities and waiving liability. Control remains with the market maker, who may choose to repay in tokens or USDT. Project teams have little say.

-

Repaying in tokens is straightforward—borrow X, return X. Repayment in USDT introduces nuance: top-tier market makers may repay based on their investment round price (slightly marked up). If the exchange price far exceeds the private round price, their profit becomes enormous. More ethical ones may use Binance’s daily volume-weighted average price on a specified date to determine USDT repayment.

-

Superpower from the last cycle: combining early-stage investment with borrowing large amounts of tokens from the project at private round pricing. As analyzed above, choosing to repay in USDT maximizes profit—for example, selling a token that appreciated 100x yields a 100x gain. In effect, this is akin to acquiring a low-cost (or zero-cost) American call option—the higher the price pumped, the greater the option value. In U.S. finance, such arrangements fall under Liquidity Service Level Agreements (SLAs), which strictly prohibit these clauses.

-

-

-

Smaller market makers are simpler (sometimes including incubators or projects with internal MM teams—the big whales in crypto often belong to this category): They primarily charge fees and follow project instructions. They typically send you a daily balance sheet and may offer suggestions. Unlike larger market makers, they communicate frequently since they manage fewer clients and aren't mostly passive.

-

The ideal scenario for a project is being forcibly listed by an exchange and intercepted (“截庄”) by a market maker. The team focuses solely on building while quietly offloading their position, profiting silently. When volumes are high, achieving $100M daily volume on Binance isn’t difficult; thus, selling $1M per day has negligible impact on price. This explains why mid-bull market projects care less about VC quality and prioritize rapid exchange listings. For example, during Vietnam’s GameFi wave, VCs recouped their entire investment—or multiplied it tenfold—during TGE, enabling extremely fast capital turnover. Funds could be recovered within a month, allowing reinvestment into quality projects during bear markets. However, this model carries high risks and often collapses.

-

A downside of being intercepted ("截庄"): The project team might end up losing money. Suppose the team collectively sells all VC-held tokens at a low price, only for a market maker to later intercept and pump the price. The team may then have to compensate disgruntled VCs out of pocket. Worse still, they might stay focused on development, see the token rise 100x without selling, and then watch everything go to zero due to product failure—a common fate. Meanwhile, the market maker profits handsomely. The backlash? Entirely directed at the project team. Even when market sentiment drives prices up 50x, retail buyers entering at those levels will blame the project for a year, though it was likely the doing of rogue ("wild") market makers. The project had no control. As mentioned earlier, reputable teams with strong fundamentals tend to play fairly—with transparent token distribution and clean conduct. Any foul play deters serious capital from touching their token.

Of course, market makers aren’t inherently evil—they’re simply running a capital business. What I’ve described mainly applies to active market makers. Those without primary market investment arms merely adjust strategies passively based on order books, rarely making dramatic moves. If the market is the riverbed, market makers are the source feeding water into it. It’s normal for projects to hold less power against them—in the secondary financial ecosystem, liquidity originates from these market makers. But ultimately, even they have their own dependencies, experiencing losses, gains, and sometimes bankruptcy.

Relationship Between Market Makers and Exchanges

Exchanges have been mentioned throughout; let me now elaborate on the shadow banking system formed between exchanges and market makers:

-

During current bear market liquidity droughts, top-tier exchanges frequently reach out to market makers, practically begging them to provide liquidity. After all, liquidity is the foundational infrastructure of any exchange.

-

Back in bull markets: Why would exchanges with massive profits resort to misusing customer assets and expanding their balance sheets? A large portion of an exchange’s liabilities consists of unsecured credit lines extended to market makers. These market makers use the funds to deepen liquidity, often adding leverage, thereby creating abundant market depth. Effectively, this grants market makers the right to misuse customer assets. When we marveled at the immense liquidity in 2021, we hailed these institutions as saviors of the secondary market—only to realize during blowups that the very liquidity providers were us, the retail users. 😭

-

Exchanges typically offer market makers numerous advantages: zero fees, unsecured loans, low interest rates. Why were market makers/hedge funds (like 3AC) willing to pay over 10% annual interest in 2021–2022? Because part of that interest was actually covered by the exchange, not borne entirely by the market maker. Some exchanges routinely issue unsecured loans to market makers as a substitute for formal liquidity management costs.

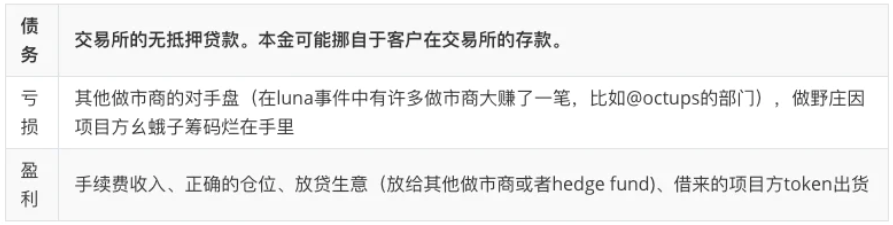

PS: This section is quite complex—here’s a table outlining how market makers interact with exchange businesses in terms of debt, loss, and profit.

- FTX & Alameda took this system to its extreme. When an exchange directly tops up a market maker’s account using customer funds, the resulting explosion affects every user. After FTX collapsed, market liquidity dropped by over 50%.

- Overall, exchange liquidity depends on market makers, who simultaneously print money (via unsecured loans) and leveraged bets, leading to frequent financial blowups and shadow banking debt crises—all funded by customer principal.

Future: Market Makers and AMMs

Of course, these are scripts from the last cycle. How things will unfold next time is unknown. For example, many new ventures in 2022 established hedge fund divisions to escape profit extraction by traditional market makers.

Regarding project-market maker dynamics, there were also notable examples last cycle. One I particularly admire is Merit Circle, which raised $105M via LBP, then opened LP mining on UNIV2/3. Its liquidity quickly ranked among the top, second only to ETH/USDC, demonstrating exceptional depth. Having already secured sufficient funding through LBP, they didn’t depend on exchange listings—but given the massive volume, Binance listed them anyway. Today, this gaming guild still holds $100M in treasury assets even during a deep bear market, with addresses publicly auditable and updated daily.

LBP was initially designed for fair launches, but during good market conditions evolved into a powerful monetization and exit tool: projects can profit without relying on market makers, breaking free from the exchange-market maker profit structure. Moreover, post-LBP liquidity pools serve as natural exits for VCs.

Following the recent wave of blowups and cleanouts involving aggressive market makers, the next cycle will likely bring major changes to exchange-based market making operations. An intriguing question will be how to decentralize these functions—partitioning permissions and assets on-chain. In the last cycle, centralized market makers became increasingly familiar with DEX systems, and mainstream aggregators began introducing RFQ features tailored for professional market makers. Recently, Binance listed Hashflow, a DEX centered around RFQ. Yet, the barrier for traditional market makers to enter DEX market making remains high, requiring 2–3 months of adaptation before deploying capital. Additionally, blockchain latency and performance issues still render many strategies ineffective. I anticipate that in the next cycle, high-performance chain-based trading engines and engineering implementations not constrained by Solidity/Vyper will further empower professional market makers to establish liquidity on DEXs, gradually shifting pricing power from CEXs to DEXs.

Another thought: the challenge of using AMMs for market making. For market makers, AMMs represent a passive convex curve—a passive convex function. Combined with impermanent loss, it's extremely difficult to pump or control prices. Uniswap v3 improved this slightly, but requires constant repositioning of price ranges, making operations cumbersome. izumi discretized v3’s function for better management, but even after discretization, each segment remains a passive convex curve—so discretization alone cannot enable active market making or control.

One of my future research directions relates to this: can we design a new functional form that shifts from passive to active? Start by defining mathematically what “passive” means around variable t, then explore transformations or eliminations of t—similar to how Fourier transforms convert time-domain functions into frequency domain. If we can achieve active management and leverage operations for market makers within DeFi, the risks associated with the old shadow banking system could be significantly reduced.

Afterword

Above are the insights I have on market makers. The only practical takeaway might be to choose transparent projects and focus on assets vetted by major platforms for use as collateral or margin.

Initially, I compiled this information inspired by @octupus. But as I wrote, I found myself reflecting on people online and around me. They might be young individuals carrying family burdens, husbands and fathers hoping to improve life for their wives and children. They might be cautious programmers working late occasionally, ordinary workers chasing modest dreams. They might be sons who told repeated lies to their families—regular people denied any chance of redemption. They pour their dreams, lives, and families into this ruleless game of price manipulation, only to face potential ruin.

To market makers, it’s just business;

To retail investors, it’s their entire life;

And truthfully, for projects that chose alignment with market makers from day one, isn’t it the same? “Users aren’t just users—they’re buying pressure.” But eventually, this too backfires.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News